AI Agents for Borrower Intake in CRE: What to Automate

Borrower intake is usually the first place CRE lending teams lose time: rent rolls are missing, sponsor data comes in uneven, and staff chase the same follow-up questions before underwriting starts. AI tools for borrower intake can make pre-screening more consistent, ask for the right documents, and check basic eligibility before a file lands with a human underwriter.

Incomplete intake packages slow down private CRE lending every day. AI agents for borrower intake help by collecting standardized deal facts, chasing missing documents, and running basic eligibility checks before a file reaches credit review. The payoff is simple: less back-and-forth, fewer half-built files, and cleaner handoffs to underwriting.

For private lenders, this is an operations play, not a thought experiment. Done well, intake automation cuts incomplete submissions, speeds up triage, and keeps messy files out of the credit queue until they are actually ready. This article looks at intake design for inbound borrowers and brokers, with specific guidance on pre-screening questions, document request logic, eligibility rules, controls, and implementation details that broader overviews, including this guide to ai agents for private commercial real estate lending, usually gloss over.

Key Takeaways

- Borrower intake automation works best when the AI agent gathers structured facts first, then requests documents based on asset type, loan purpose, and sponsor profile.

- McKinsey’s work on banking operations and risk workflows points to document-heavy processes as a major source of manual rework in lending.

- Consumer Financial Protection Bureau guidance on the Equal Credit Opportunity Act makes the standard clear: intake practices need to be consistent, non-discriminatory, and tied to a defined adverse action process when eligibility decisions affect applicants.

- The NIST AI Risk Management Framework calls for logging, human oversight, and controls around accuracy, validity, and traceability in automated systems.

- Private lenders should automate completeness checks and basic program-fit rules first. Exceptions, judgment calls, and policy overrides still belong with credit or origination staff.

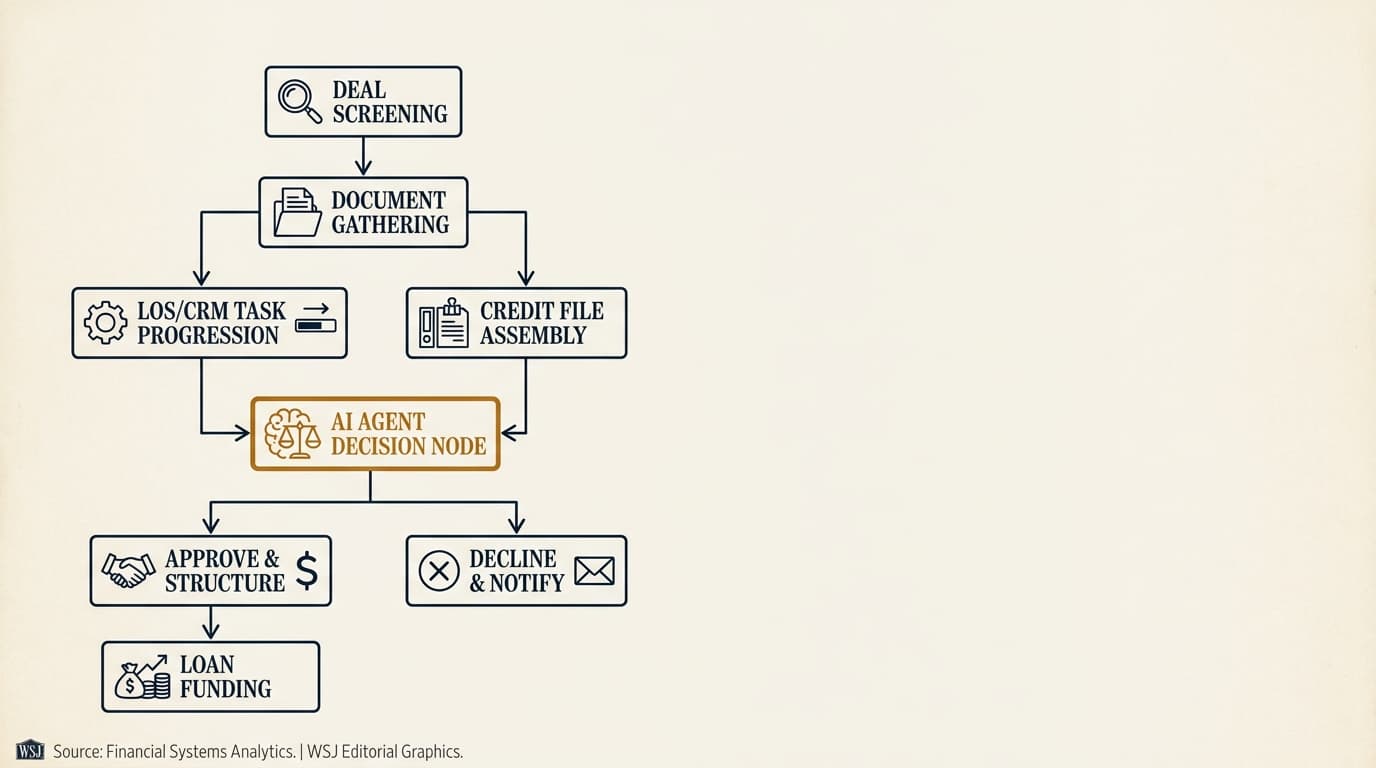

What AI agents for borrower intake do

AI agents for borrower intake are workflow systems that interact with inbound borrowers or brokers, capture required facts in a structured format, request supporting documents, and test submissions against initial policy rules. They do not replace underwriting. They sit in front of it as an intake control layer and answer a narrower question: is this file complete enough and close enough to program fit to move forward?

In practice, intake agents handle four core jobs:

- Collect a minimum viable credit package through web forms, email, portal messages, or chat interfaces.

- Normalize incoming information into standard fields such as loan amount, property type, occupancy, sponsorship, entity structure, and requested timeline.

- Trigger document requests based on the submission details.

- Apply threshold checks such as geography, asset class, requested leverage, and business-purpose fit before routing the file.

This is different from ai agents for cre loan origination, which manage broader workflow orchestration across the pipeline, and from ai agents for cre underwriting, which deal with risk, cash flow, and exceptions after intake is done.

Federal Reserve research on digital financial interactions found that users increasingly expect online information capture and status visibility. In commercial lending, borrowers and brokers expect the same thing, even if the deals themselves are still bespoke and a little messy.

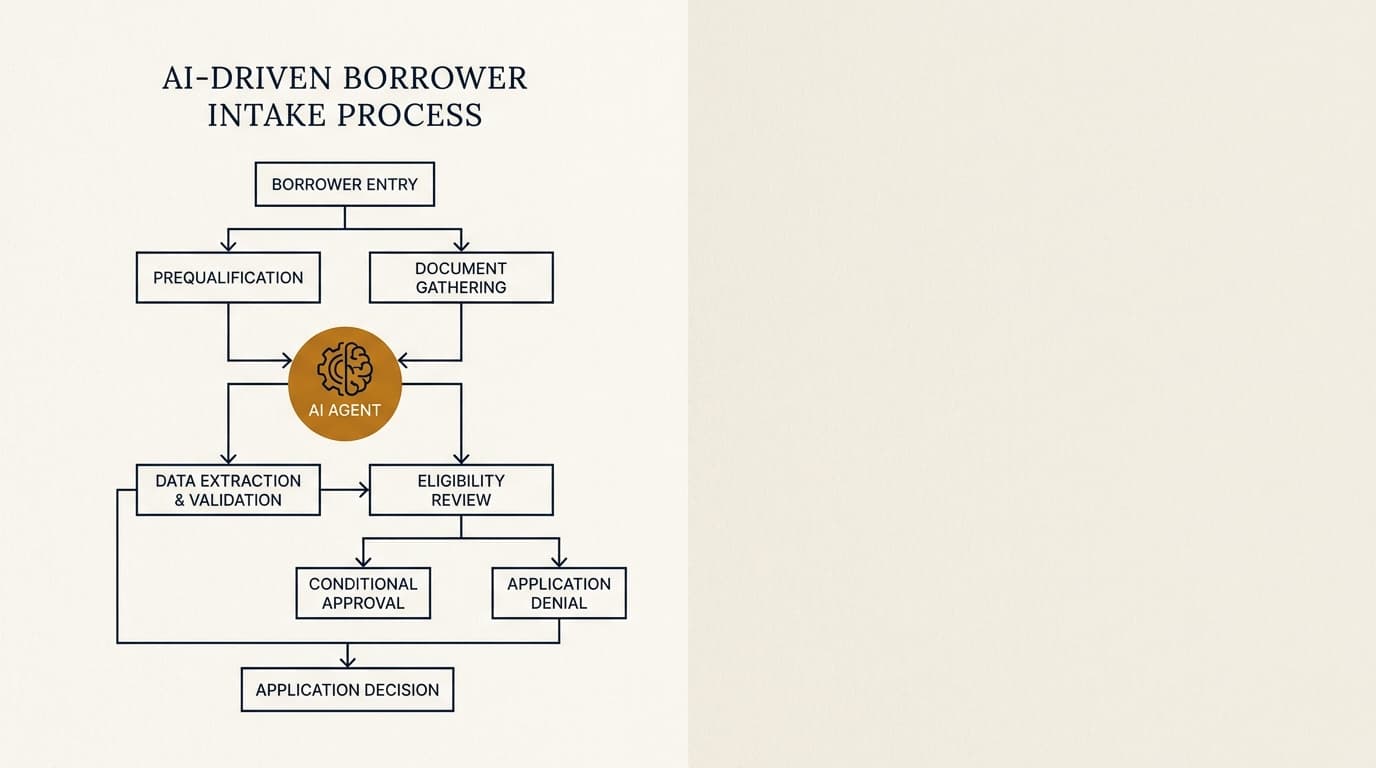

Borrower intake workflow: where AI agents fit

Borrower intake sits between lead capture and underwriting package assembly. A well-configured intake agent cuts down on files that reach underwriting with missing financials, unclear guarantor support, or unresolved program-fit issues.

A typical inbound workflow looks like this:

| Stage | Primary task | AI agent role | Human role |

|---|---|---|---|

| Initial inquiry | Capture basic deal facts | Ask standardized pre-screen questions | Review strategic fit for high-priority relationships |

| Pre-screen | Test minimum program criteria | Check asset type, location, size, loan purpose, leverage request | Approve exceptions or reject out-of-box scenarios |

| Document collection | Assemble initial credit package | Send dynamic request list, reminders, completeness checks | Clarify unusual structures or custom items |

| Data validation | Compare borrower responses to documents | Flag mismatches, missing dates, stale statements | Resolve discrepancies |

| Routing | Move file to origination or underwriting | Assign stage and next action | Confirm queue priority and ownership |

The handoff threshold needs to be explicit. A lot of lenders move files too early and quietly dump intake work onto underwriters. A better model is to require a defined set of structured fields and a minimum document package before a file can enter underwriting review.

Pre-screening questions AI agents should ask

Pre-screening works best when the questions are ordered to rule out obvious non-fit deals early. The first pass should establish program fit in under five minutes. Only after that should the workflow branch into asset-specific and sponsor-specific questions.

The initial question set should capture the following:

Loan request basics

Loan amount, purpose, and timeline tell you quickly whether the deal belongs in the pipeline at all. These fields should be mandatory and standardized, with controlled answer choices whenever possible.

- Requested loan amount

- Purchase, refinance, cash-out refinance, bridge, construction takeout, or recapitalization

- Requested close date

- Interest-only expectation

- Desired term and extension structure

Property and collateral data

Property details should be collected in a structured format because they drive both policy checks and downstream document requests. Free-text property descriptions create cleanup work nobody wants later.

- Property type and subtype

- Address, state, and market

- Number of units or square footage

- Current occupancy

- Stabilized or transitional status

- Year built and major renovation date

Sponsor and borrower information

Sponsorship data is often the biggest hole in brokered submissions. Intake agents should collect entity and guarantor information separately so the borrowing entity, property manager, and sponsor group do not get mashed together.

- Borrowing entity legal name

- Sponsor experience with similar asset types

- Net worth and liquidity ranges

- Guarantor availability

- Recourse expectations

- Bankruptcy, foreclosure, or litigation disclosures where policy and law allow them

Economics and performance

Income and leverage questions should support later validation. If the borrower states in-place NOI or DSCR assumptions at intake, the system should keep that original response and compare it with uploaded operating statements later on.

- Purchase price or current valuation estimate

- Requested leverage

- Trailing twelve-month net operating income

- Recent capex completed or planned

- Major tenant concentrations for commercial assets

Federal Financial Institutions Examination Council guidance on standardized data collection makes a point that applies directly here: consistent field definitions improve data quality and downstream reporting. In CRE intake, if occupancy, NOI, and borrower liquidity are defined three different ways, every later stage inherits that confusion.

Document request automation for borrower intake

Document request automation is where intake agents usually earn their keep fastest. The agent should generate a checklist from the facts already collected, then update that list as the borrower provides more information.

A baseline request package for income-producing CRE commonly includes:

- Borrower or broker deal summary

- Current rent roll

- Trailing 12-month operating statement

- Last 2 years of property operating statements or tax returns, if available

- Sponsor schedule of real estate owned

- Organizational chart and borrowing entity documents

- Bank statements or liquidity evidence for guarantors, if required by policy

- Purchase contract or payoff statement for refinances, depending on purpose

The checklist should change with the deal. For example:

| If intake data shows | Then request | Why it matters |

|---|---|---|

| Hospitality asset | STR reports, franchise agreement summary, seasonal performance detail | Cash flow volatility and brand obligations differ from multifamily |

| Retail center with concentration risk | Top tenant leases and rent commencement dates | Tenant rollover and credit quality affect durability of NOI |

| Bridge execution with capex plan | Scope of work, budget, sources and uses, contractor detail | Lender needs to assess business plan feasibility |

| Cash-out refinance | Use-of-proceeds explanation and recent capital events | Policy may restrict distributions or repayment uses |

| Foreign ownership or layered entities | Enhanced entity documentation and beneficial ownership details | KYC and legal review requirements increase |

FinCEN’s Customer Due Diligence Rule requires covered institutions to identify and verify beneficial ownership information in applicable cases. Even where a private lender is not mirroring bank procedures in every detail, intake design still has to account for ownership transparency and the documentation standards legal and compliance teams will ask for later.

One practical rule helps a lot: every requested document should carry a machine-readable status such as requested, received, incomplete, stale, mismatch, or waived. That status history becomes the operating record, and it is much more useful than a vague note saying “waiting on docs.”

Eligibility checks before underwriting begins

Eligibility checks should answer a narrow question: does the file meet basic program criteria, and does it contain the minimum information needed for credit review? They should not try to perform full risk assessment. That is where intake systems start pretending to know more than they do.

Common intake-stage eligibility checks include:

- Geography fit, including state, market, and excluded jurisdictions.

- Asset type fit, including multifamily, mixed-use, industrial, retail, office, hospitality, self-storage, or other categories allowed by policy.

- Loan size fit, with minimum and maximum principal amounts.

- Purpose fit, limited to purchase, refinance, bridge, or other product categories the lender actually offers.

- Leverage fit, based on requested loan-to-value within program tolerance.

- Stabilization fit, such as occupancy or debt service thresholds for permanent-style executions.

- Sponsorship fit, including experience, liquidity, and guarantor support requirements.

A useful design principle is to separate hard stops from soft flags. A hard stop might be a property type the lender does not finance at all. A soft flag might be leverage above standard policy but still within an exception range. That distinction matters. Without it, the system rejects files that should really go to a human for review.

Regulation B under the Equal Credit Opportunity Act requires careful governance of application handling and adverse action processes. If an intake agent is used to decline or screen out applicants, the lender needs documented rules, consistent application, and legal review of how those outcomes are communicated.

A decision framework: what to automate, what to escalate

The best intake programs automate determinable facts and escalate judgment calls. The dividing line is straightforward: can the answer be supported by a documented rule, a reliable data source, and a reviewable audit trail?

The table below is the framework most lenders actually need:

| Task | Automate | Escalate | Reason |

|---|---|---|---|

| Collect borrower contact and deal facts | Yes | No | Structured data capture is repeatable |

| Generate document checklist | Yes | No | Rules can be mapped to product, asset, and entity type |

| Check whether required files were uploaded | Yes | No | Completeness is measurable |

| Compare stated occupancy to rent roll occupancy | Yes | Sometimes | Mismatch can be flagged automatically, interpretation may require review |

| Decline unsupported asset class | Yes, with policy approval | Sometimes | Only if the exclusion is explicit and current |

| Assess sponsor quality | No | Yes | Experience, reputation, and execution capability are contextual |

| Evaluate business plan credibility | No | Yes | Requires judgment, market context, and often discussion |

| Approve policy exceptions | No | Yes | Governance and pricing authority sit with humans |

This is where a lot of automation projects go sideways. They try to force nuanced credit reasoning into the intake layer, then run into the basic reality of private lending: edge cases are not edge cases for long. A transitional retail property at 68% occupancy may be outside one permanent program and perfectly reasonable for a bridge execution if sponsorship, basis, and the lease-up plan hold up. Intake should identify that condition, not pretend to settle the credit decision.

Data model and systems design for intake automation

Borrower intake automation lives or dies on the data model. If the system stores nothing but uploaded PDFs and loose email threads, it will not produce reliable routing, reporting, or audit history.

At minimum, the intake record should include:

- Submission source: borrower direct, broker, referral partner, website, email

- Timestamped intake responses with version history

- Document inventory with status and receipt dates

- Rule evaluation results with pass, fail, flag, or waived outcomes

- Assignee and escalation history

- Communication log across portal, email, and messaging

- Reason codes for declines, withdrawals, and missing information closures

The NIST AI Risk Management Framework says organizations using AI systems should build governance for traceability, monitoring, and human oversight. In lending operations, that means reproducible rule sets, visible prompts or decision logic where relevant, and a clear record of who overrode what and why.

A second design issue is canonical fields. Take occupancy as an example. It should have one official calculation basis in the intake schema, with any alternate basis stored separately. Without that discipline, the CRM, loan origination system, and underwriting tools will all show different numbers for the same file, and then everyone wastes time arguing over which one is “right.”

Controls, audit trails, and exception handling

Controls are not a back-office add-on. If the intake agent asks questions, requests documents, or applies eligibility rules, the lender needs an auditable record of the exact inputs, the rule version, and the outcome.

Core controls should include:

- Versioned policy rules with effective dates

- Role-based permissions for rule changes and waivers

- Mandatory reason codes for manual overrides

- Retention of the original borrower-submitted response even after corrections

- Sampling and quality-control review of accepted and rejected files

- Periodic testing for disparate treatment and inconsistent application of screening logic

CFPB Equal Credit Opportunity Act compliance resources make the broader point clearly: application intake and evaluation practices require consistent treatment and documentation. Commercial real estate lending is not consumer mortgage lending, but the operational lesson is the same. Intake automation cannot be a black box.

Exception handling deserves its own attention. Files with missing T-12s, disputed ownership structures, stale bank statements, or contradictory occupancy figures should not just sit there. The system should assign an exception type, route it to the right owner, and set a deadline. Otherwise, the team recreates the same inbox chaos with nicer software.

Implementation steps for private CRE lenders

Private lenders should roll out intake automation in stages, starting with the narrowest use case that measurably reduces rework. The right first release usually is not a fully conversational agent. It is a structured intake workflow with dynamic checklists and rule-based triage.

- Define the minimum viable intake package for each product type.

- Map hard-stop rules and soft-flag rules from current credit policy.

- Standardize field definitions for loan request, collateral, sponsorship, and purpose.

- Build dynamic document checklists by asset type, loan purpose, and entity structure.

- Configure document statuses such as missing, received, incomplete, stale, mismatch, and waived.

- Route soft flags and policy exceptions to a named human owner with service-level targets.

- Log every intake response, rule result, document request, and manual override.

- Measure conversion, cycle time, completeness rate, and exception frequency before expanding scope.

For most private lenders, the first KPI set should stay operational: median time from initial inquiry to a complete intake package, percentage of files entering underwriting fully complete, touches per file, and fallout rate by reason code. Those measures tell you something real. Broad claims about “productivity gains” usually do not.

A useful benchmark is to compare broker-submitted files against direct borrower submissions. In many shops, brokered deals arrive faster but with more variation in document quality and field consistency. An intake agent can reduce that variance by enforcing the same checklist and field rules across both channels.

Teams planning broader workflow automation should keep intake as its own layer, then connect it to later processes. That sequencing avoids overlap with systems built for ai agents for cre loan origination and keeps early-stage data collection separate from the logic reserved for ai agents for cre underwriting.

Frequently Asked Questions

What are ai agents for borrower intake in commercial real estate lending?

AI agents for borrower intake are software systems that collect deal facts from inbound borrowers or brokers, request required documents, and apply basic eligibility and completeness checks before underwriting starts. In CRE lending, they are typically used to standardize intake for property details, sponsorship information, requested leverage, and the initial credit package.

Which intake tasks should private lenders automate first?

Most private lenders should start with structured pre-screen questions, dynamic document request lists, and completeness checks. Those tasks are rule-based, and they produce immediate operational gains by cutting manual email follow-up and keeping incomplete files out of underwriting. Judgment-heavy work such as sponsor assessment or business plan evaluation should stay with human staff.

Can an intake agent decline a loan request automatically?

An intake agent can screen out requests automatically only when the lender has explicit, documented hard-stop rules and has reviewed how those outcomes are communicated. Regulation B under the Equal Credit Opportunity Act requires controlled application handling and adverse action governance. In practice, many private lenders use automation to flag non-fit files for human confirmation instead of issuing immediate automated declines.

How does borrower intake automation differ by property type or market?

The core workflow is similar across markets, but the checklist and eligibility logic vary by asset type, state, and local legal requirements. A multifamily request in Texas may need a different property-level package than a hospitality asset in Florida or a mixed-use property in New York. Lenders also differ by geography in excluded states, minimum loan size, and entity documentation standards, so intake rules should be configurable by region and product.

What metrics show whether ai agents for borrower intake are working?

The most useful metrics are median time to complete intake, percentage of files entering underwriting with all required documents, touches per file, and fallout rate by reason code. Secondary measures include broker response time, stale-document frequency, and the share of files that need manual exception handling. Those numbers show whether intake automation is actually reducing rework instead of just moving it to another team.