Auditable AI for CRE lending.

Where AI agents fit across the commercial real estate lending lifecycle — what to automate, what to leave to humans, and how to deploy systems your auditors will sign off on.

TOPICS

AI agents in real estate

Where AI agents fit across the CRE lending lifecycle — what to automate, what to leave to humans, and how to deploy auditable systems.

AI Agents for Private CRE Lending in 2026

Private CRE lenders are starting with AI agents in document-heavy work: intake, document review, servicing requests, and portfolio surveillance. This guide lays out where those agents fit across the lending lifecycle, what they should and should not automate, how to measure ROI, and which controls matter if you want an auditable system in 2026.

Read the guide →

AI Agents for CRE Loan Origination: What to Automate

Commercial real estate loan origination still bogs down at the front end: inquiry triage, borrower follow-up, application intake, and broker updates often get split across inboxes, spreadsheets, and loose handoffs. This article looks at where AI agents can handle CRE origination work reliably, where credit teams still need to stay involved, and how lenders can build audit-ready controls around both.

CRE Loan Origination Workflow AI Agent Guide

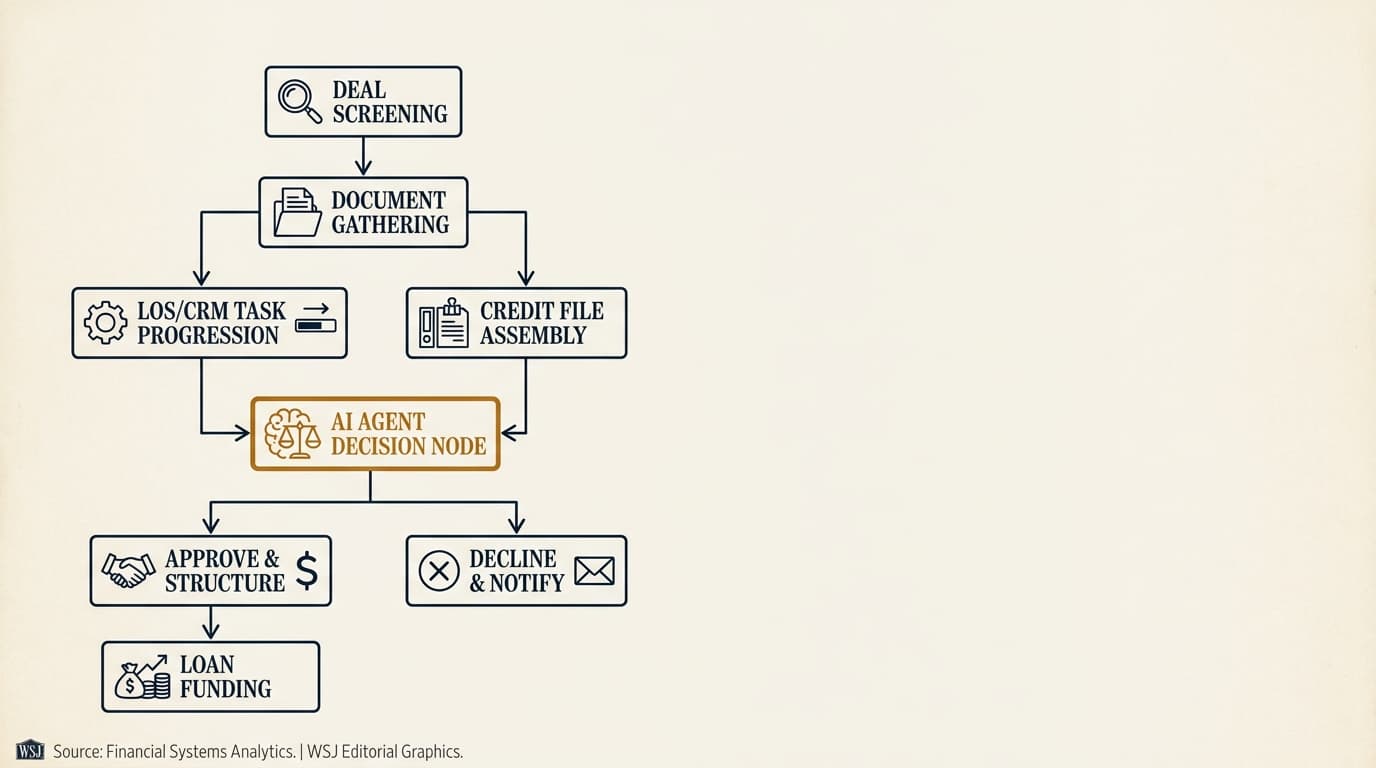

A CRE loan origination workflow AI agent can screen inbound deals, gather the required documents, move tasks through the LOS or CRM, and assemble a credit-ready file for human review. The real value isn’t full automation; it’s shorter cycle times, fewer handoff mistakes, and a clear record of what the system did at each step.

AI Agents for Borrower Intake in CRE: What to Automate

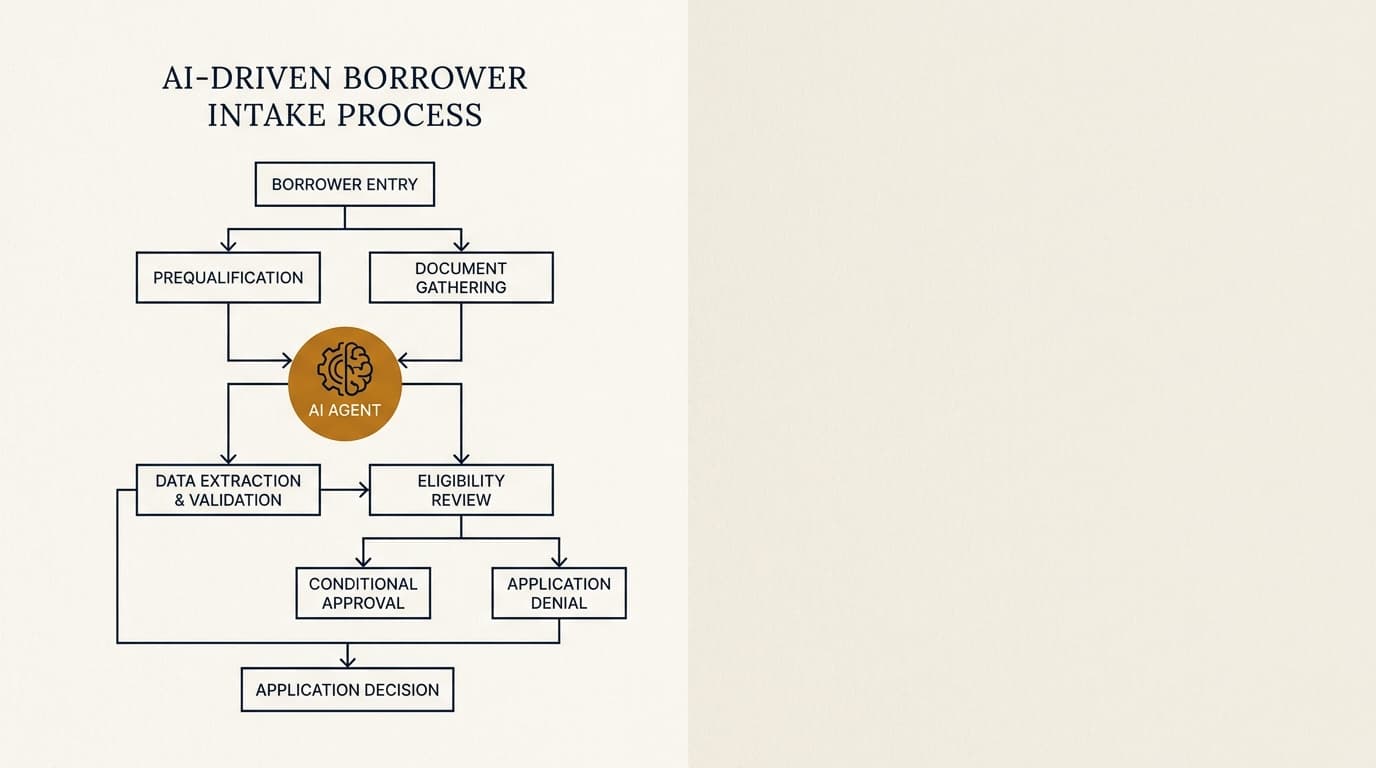

Borrower intake is usually the first place CRE lending teams lose time: rent rolls are missing, sponsor data comes in uneven, and staff chase the same follow-up questions before underwriting starts. AI tools for borrower intake can make pre-screening more consistent, ask for the right documents, and check basic eligibility before a file lands with a human underwriter.

AI Agents for CRE Underwriting: Controls and Risks

AI tools for CRE underwriting can pull together borrower, property, and market data much faster than a manual process, but they should support analyst judgment, not make credit decisions on their own. For private lenders, they’re usually most useful for triage, data reconciliation, flagging exceptions, and producing audit-ready handoffs.

AI Underwriting for Private Lenders: What to Automate

Private CRE lenders can automate document intake, data standardization, covenant testing, and exception routing with relatively low risk. Credit judgment, sponsor assessment, market interpretation, and structuring decisions still need analyst review because they rely on incomplete information, context, and policy tradeoffs.

AI Agents for DSCR and LTV Analysis Explained

Debt service coverage ratio and loan-to-value calculations are only as good as the assumptions behind them. AI agents can pull together borrower, property, and market data, run DSCR and LTV the same way every time, and catch mismatches before an analyst treats the numbers as reliable.

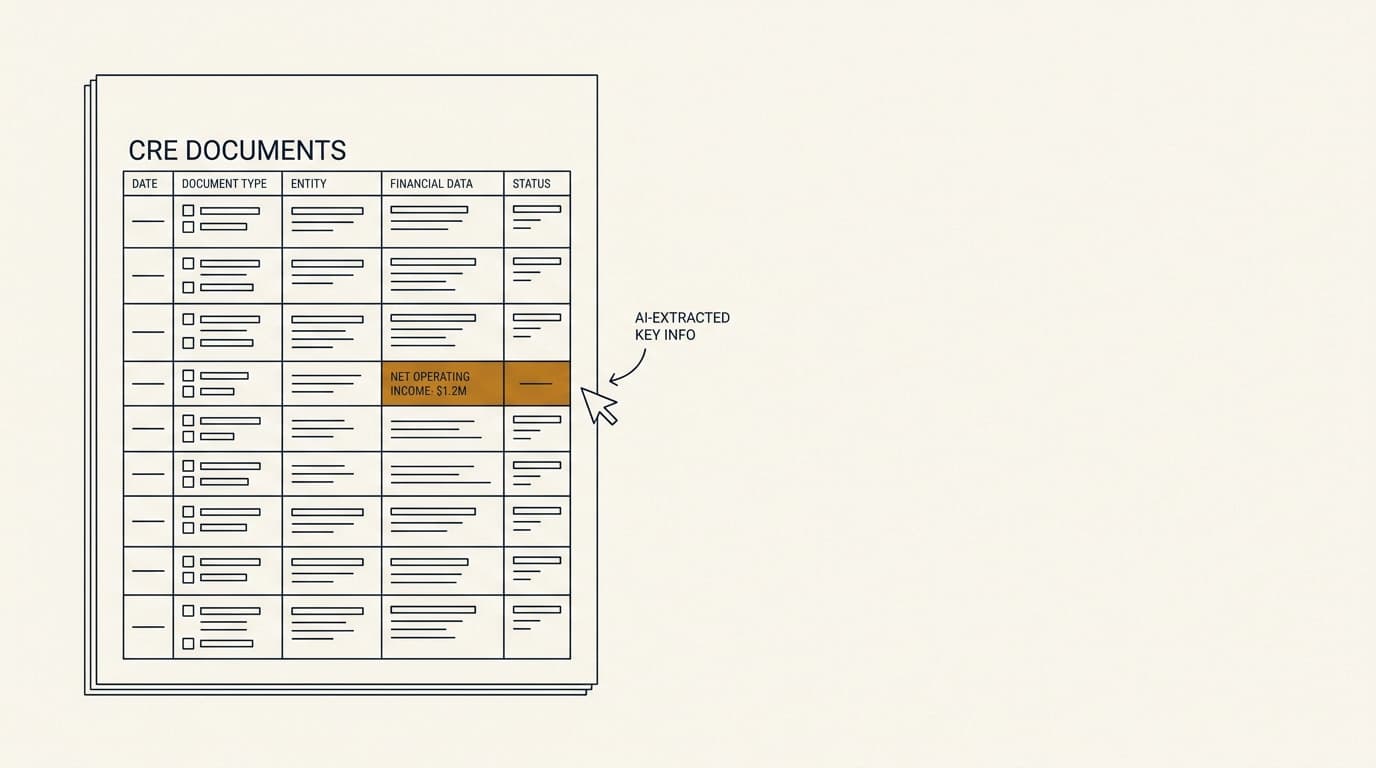

AI Agents for CRE Document Analysis: Controls That Matter

Rent rolls, trailing-12s, lease abstracts, and borrower financial packages almost never show up in a consistent format. This article shows how AI tools for CRE document analysis pull key fields, standardize property-level data, flag exceptions for review, and send verified outputs into underwriting models with a clear audit trail.

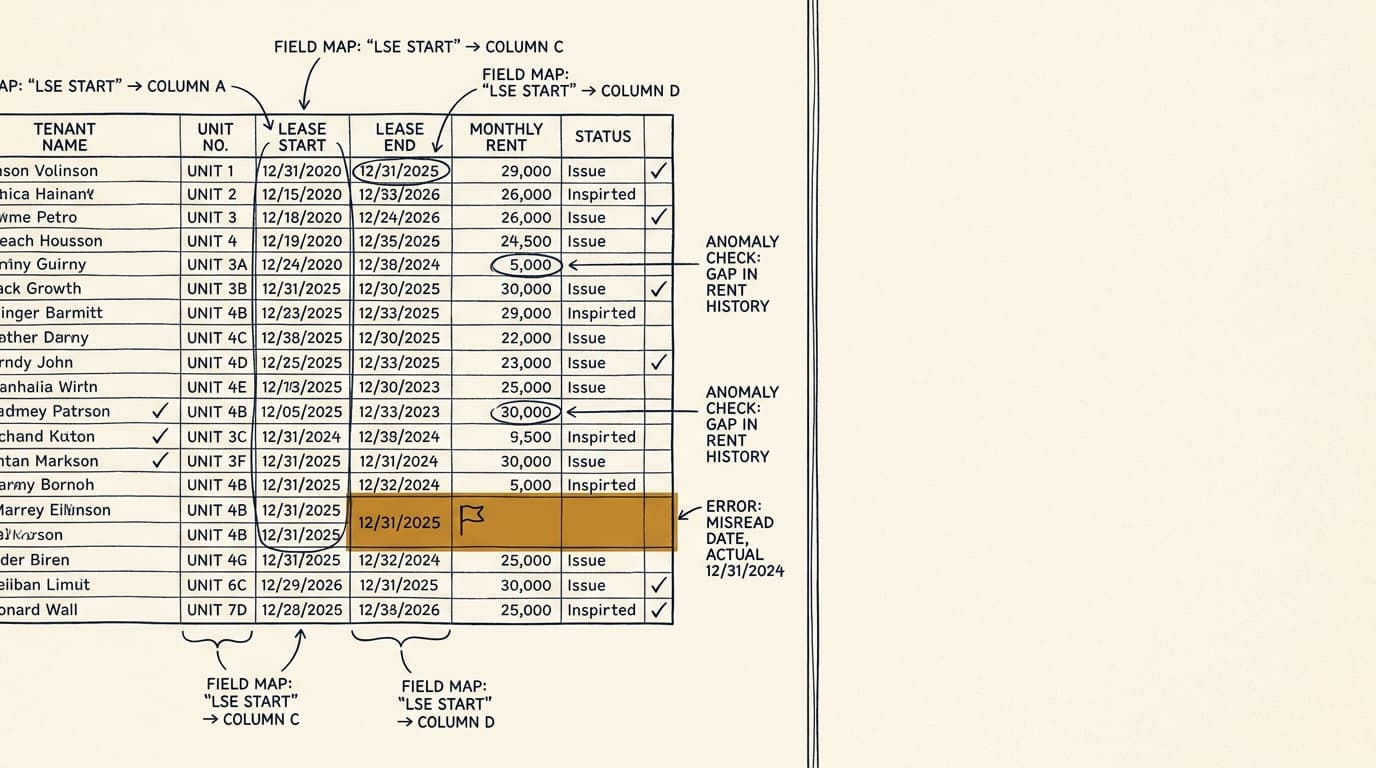

AI Document Extraction for Rent Rolls: QC Guide

Rent roll extraction usually breaks at the field level: unit IDs change format, lease dates get misread, concessions end up counted as base rent, and vacant units are labeled inconsistently. This article lays out how AI rent roll extraction needs to handle mapping, anomaly detection, and quality checks before lenders use the output to size or price a deal.

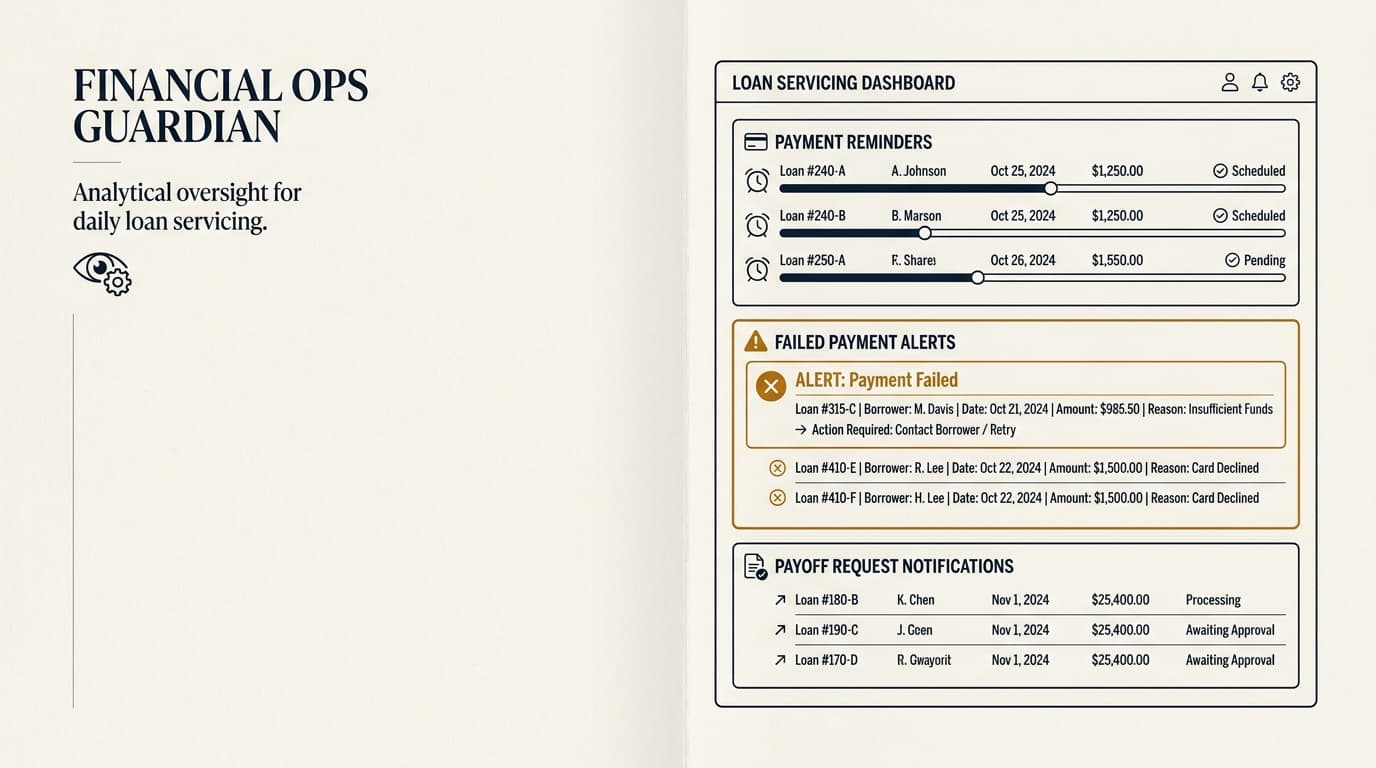

AI Agents for Loan Servicing in CRE: Uses and Controls

For many private CRE lenders, post-close servicing eats up more staff time than the payoff itself. AI tools for loan servicing can handle payment reminders, borrower requests, covenant tracking, escrow notices, and delinquency workflows without losing audit trails, approval controls, or servicing records.

AI for Loan Servicing Payment Management Guide

Servicing teams spend too much post-close time chasing routine payment follow-up, answering borrower emails, and checking status updates. This article looks at where AI actually fits in CRE loan servicing workflows, with specific examples for reminders, failed-payment triage, payoff requests, and borrower service tickets.

AI Agents for Portfolio Monitoring in Private CRE

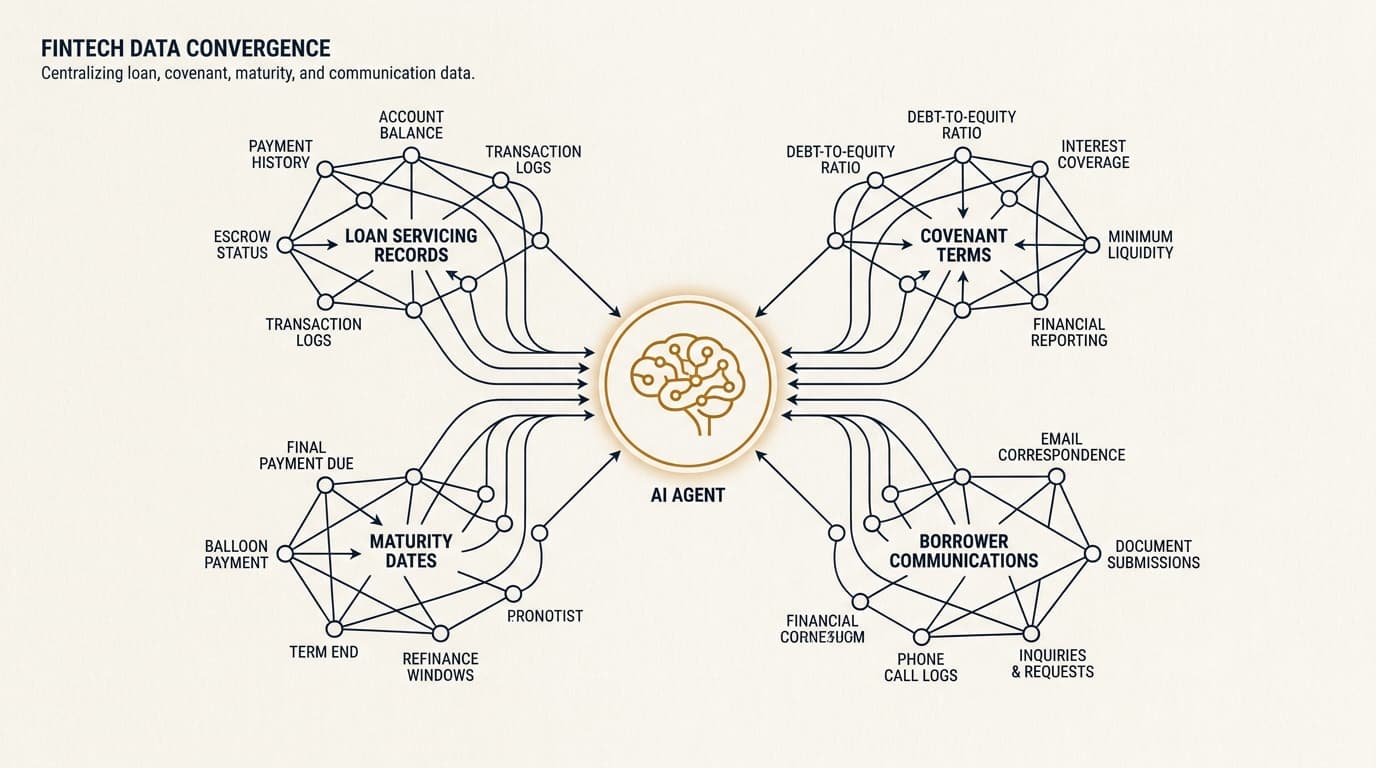

Private CRE lenders usually spot post-close risk after the fact because servicing data, covenant terms, maturity dates, and borrower communications live in different systems. AI agents for portfolio monitoring pull those records into one ongoing review process that flags covenant slippage, refinance risk, missing reporting, and escalation triggers before a loan ends up in special servicing.

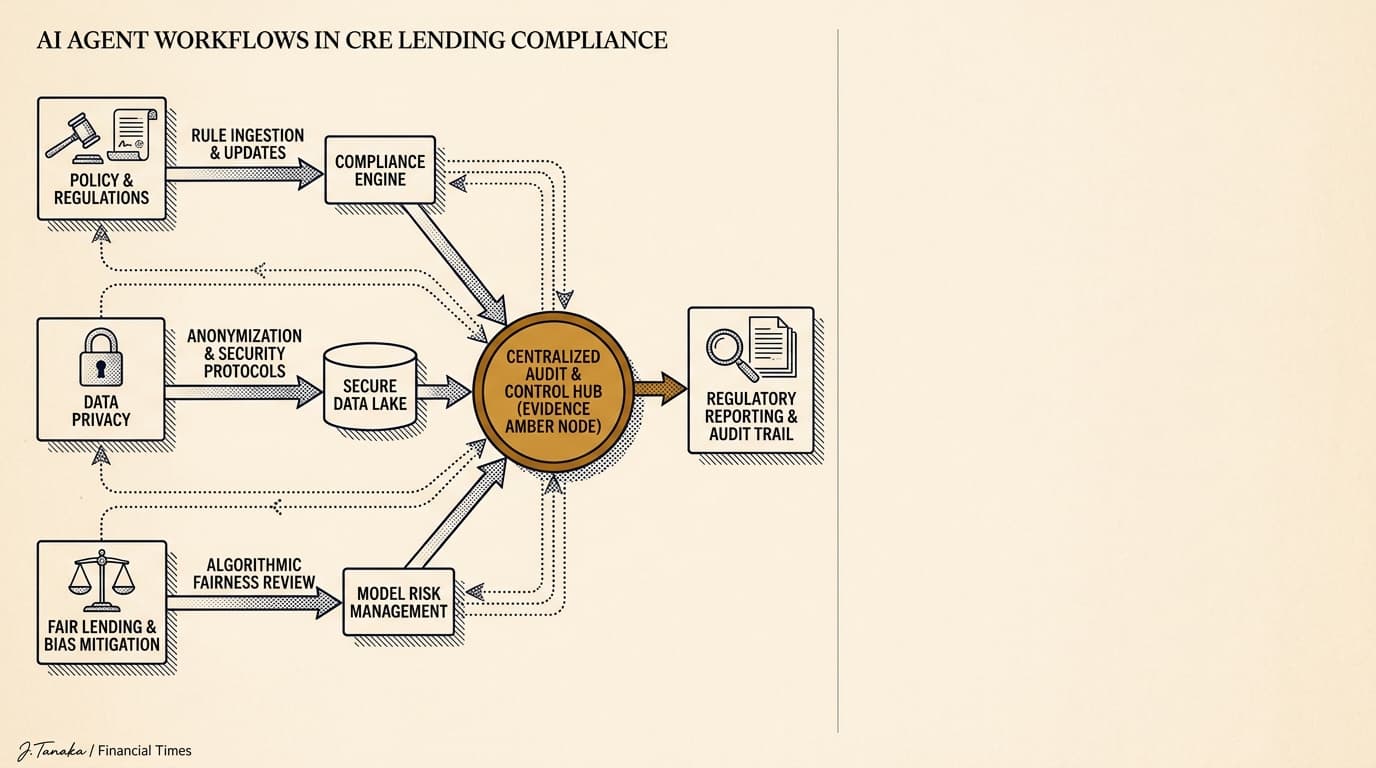

AI Agents for CRE Lending Compliance: Controls That Hold

AI agents in credit workflows need to stay within documented control boundaries, not outside them. For private CRE lenders, that means tying each agent action to lending policy, privacy requirements, fair lending rules, recordkeeping obligations, and human review standards before rollout.

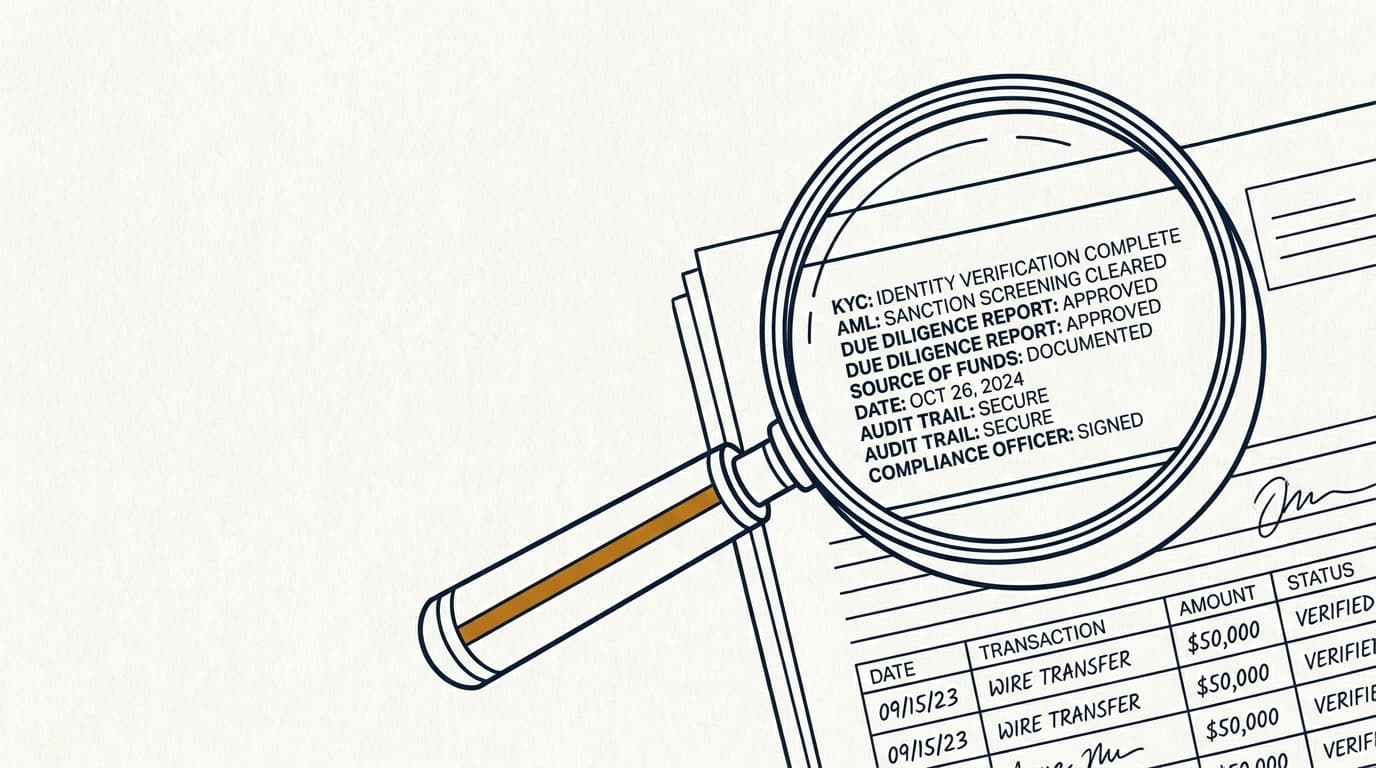

AI Agents for KYC and AML in Lending in 2026

Private lenders can use AI agents to gather identity documents, check names against sanctions lists, trace beneficial ownership, and send exceptions to human reviewers. The payoff is faster, more consistent processing, but the control framework still rests on documented policies, vendor oversight, and regulated staff making the final calls.

Yield maintenance

Yield maintenance from first principles — formula, Treasury inputs, prepayment timing, and how it compares to defeasance and step-down across CMBS, multifamily, office, and retail loans.

Commercial Real Estate Yield Maintenance Guide 2026

Yield maintenance is a commercial real estate prepayment clause that compensates the lender if a loan is paid off before maturity. In practice, the cost turns on the loan rate, time remaining, the Treasury benchmark in the formula, and the exact wording of the note and rider.

Read the guide →

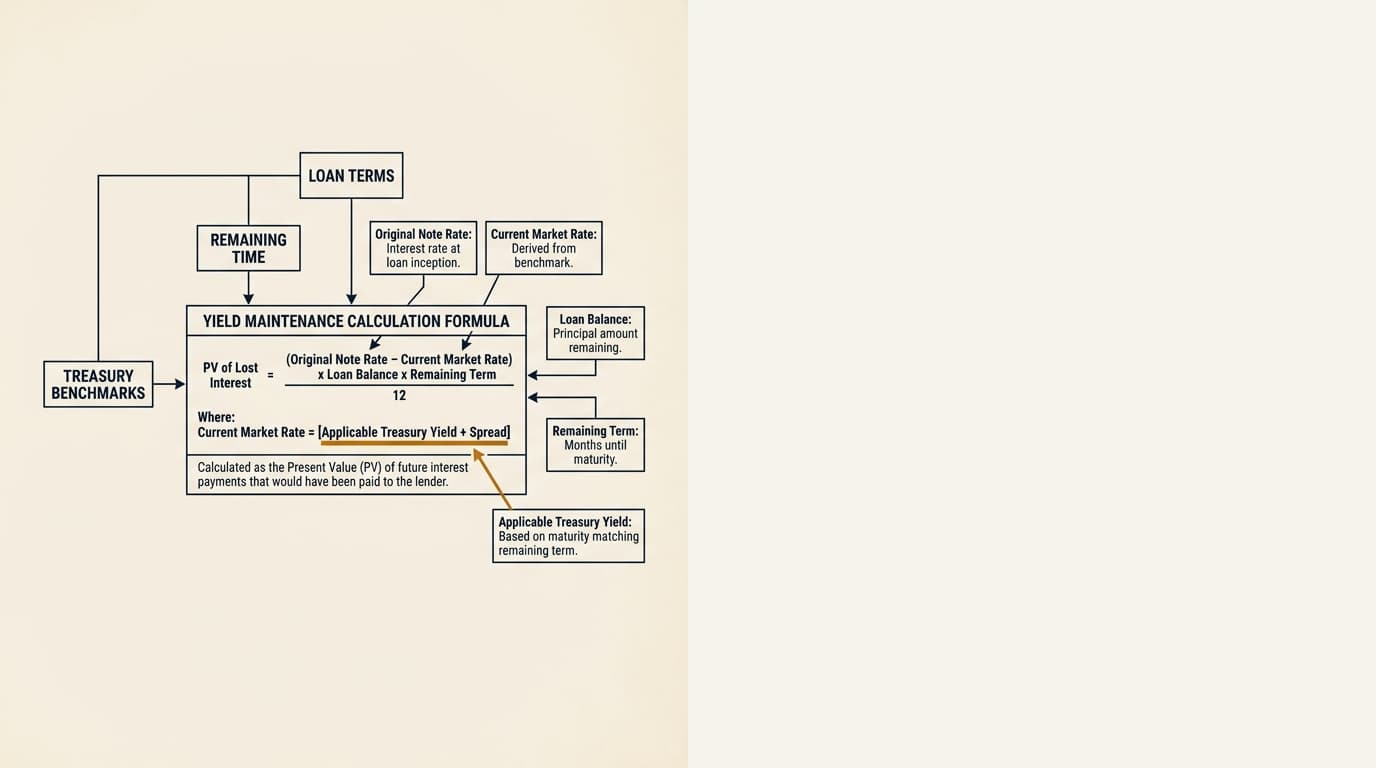

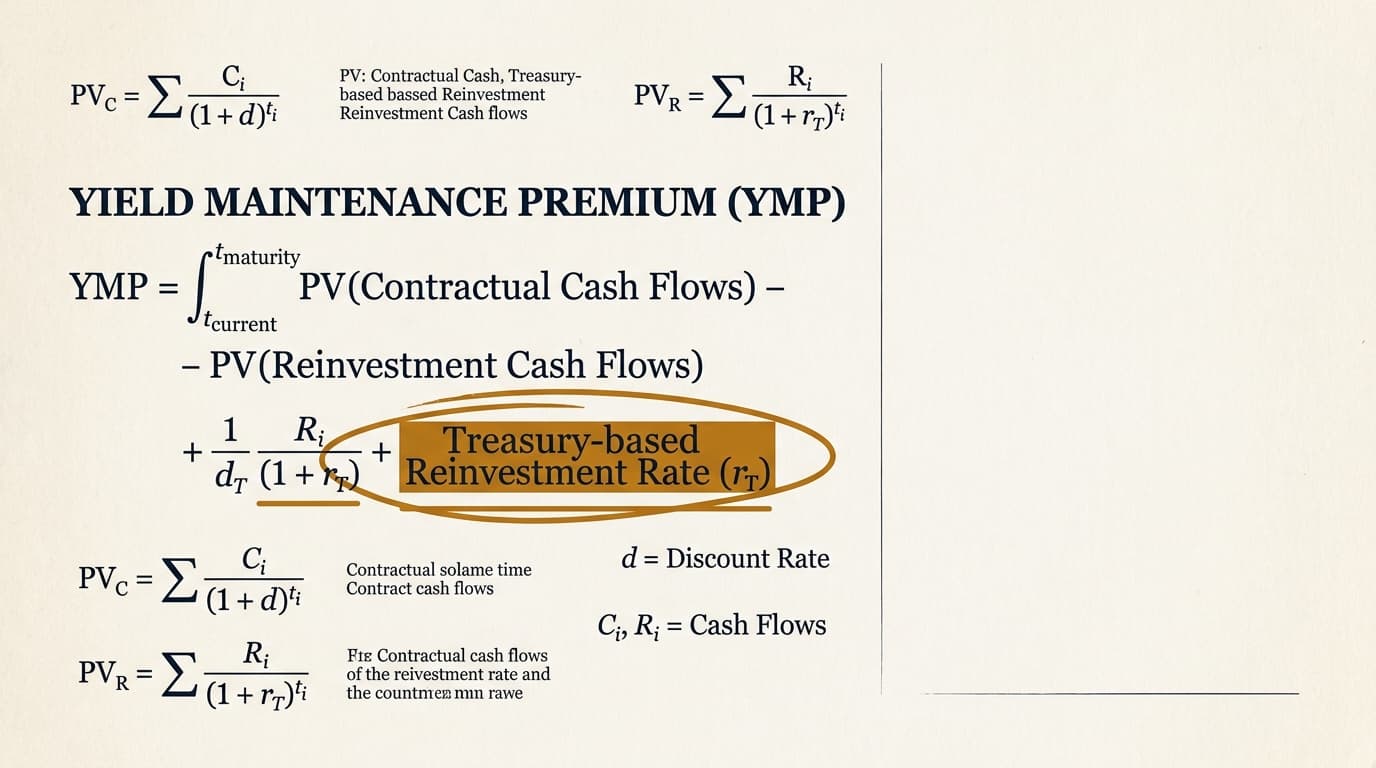

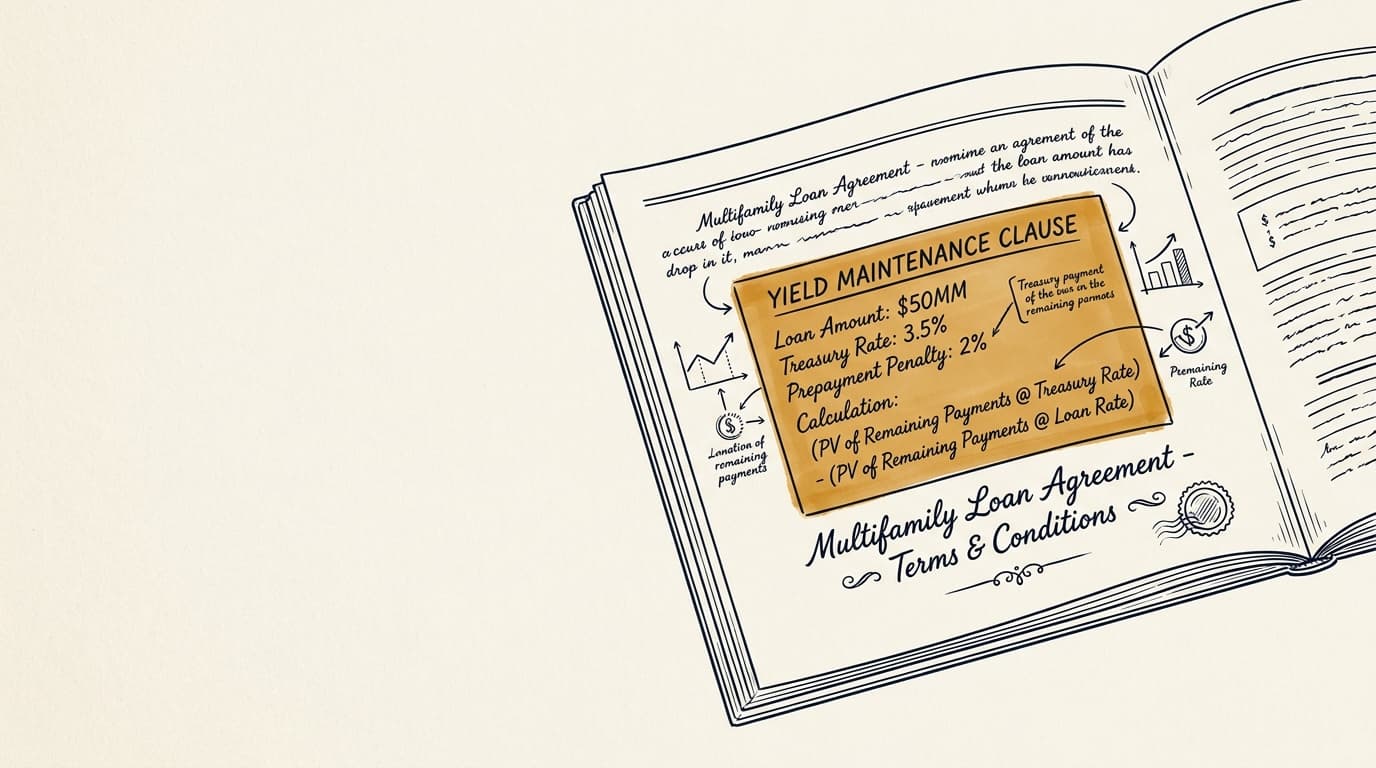

Yield Maintenance Formula: Audit the Calculation

Yield maintenance usually equals the present value of the lender’s lost interest, using the scheduled loan payments discounted at a Treasury-based reinvestment rate, with any contractual spread added or subtracted. In practice, the outcome depends less on what the note calls it than on three things: the remaining amortization schedule, the Treasury benchmark the loan points to, and the discount rate set in the loan documents.

Yield Maintenance Treasury Rate: Which Rate Is Used?

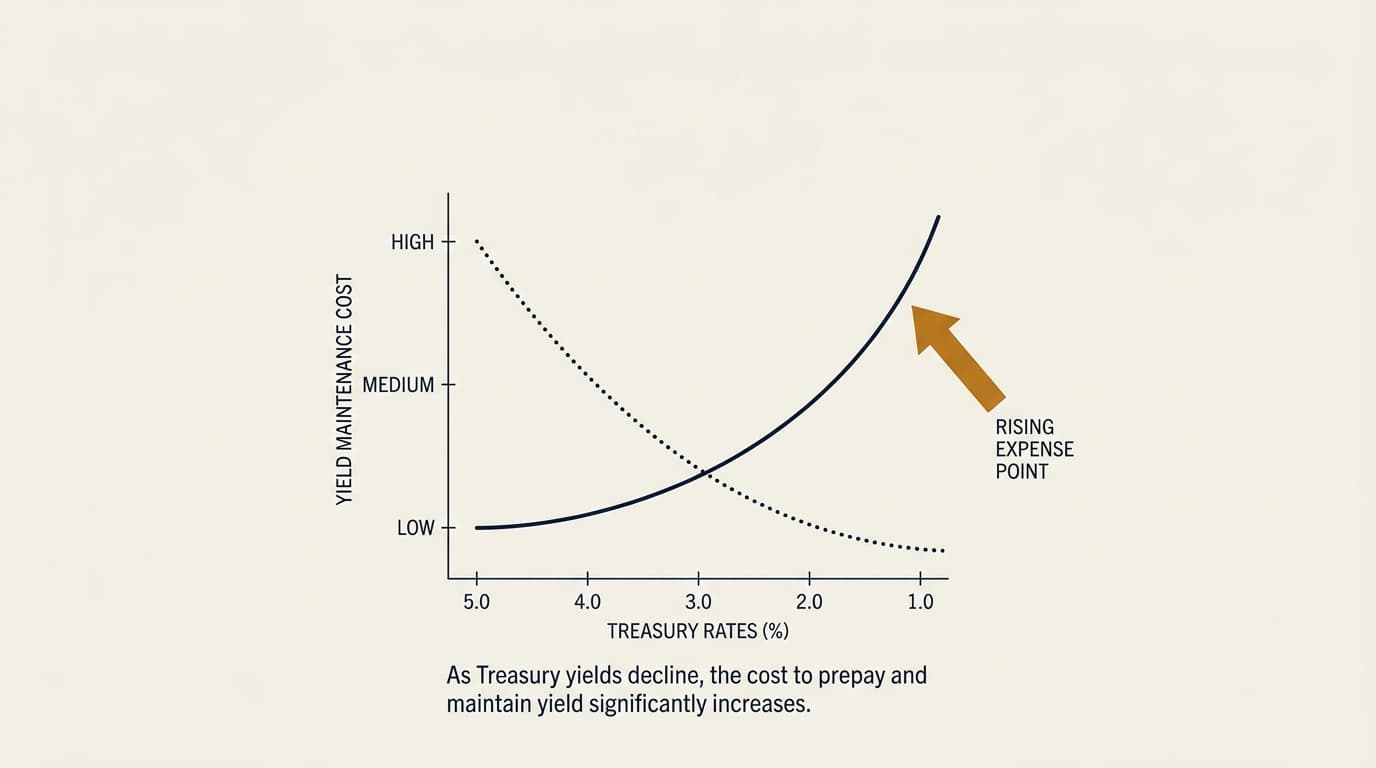

Most yield maintenance disputes start with a single input: the Treasury rate. Loan documents usually tie the calculation to a specific Treasury security or an interpolated Treasury yield matched to the remaining term, and even a 10- to 25-basis-point move can materially change the prepayment charge.

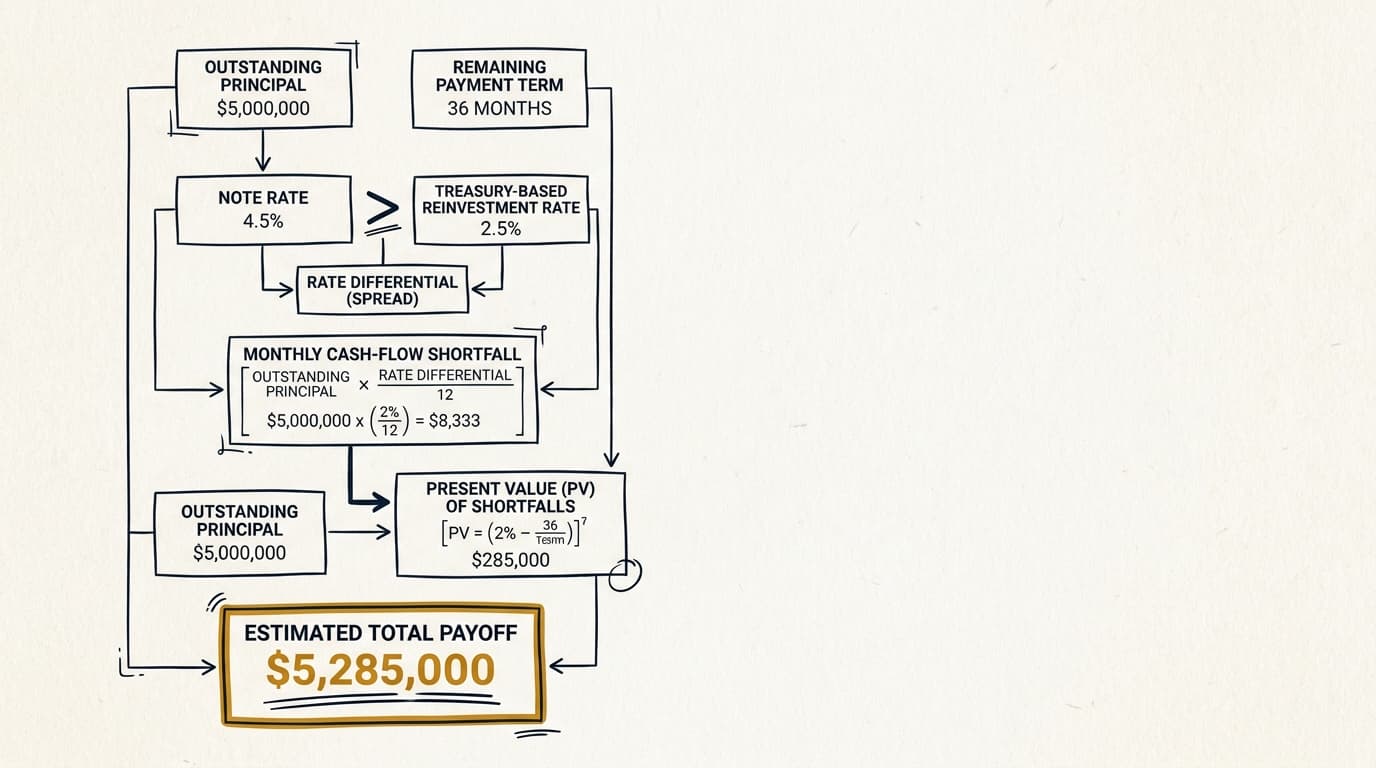

Yield Maintenance Calculation Example for CRE Payoffs

A yield maintenance example uses four inputs: outstanding principal, note rate, the Treasury-based reinvestment rate, and the remaining payment term. It walks through the math step by step, including the monthly cash-flow shortfall, the present value calculation, and the estimated total payoff.

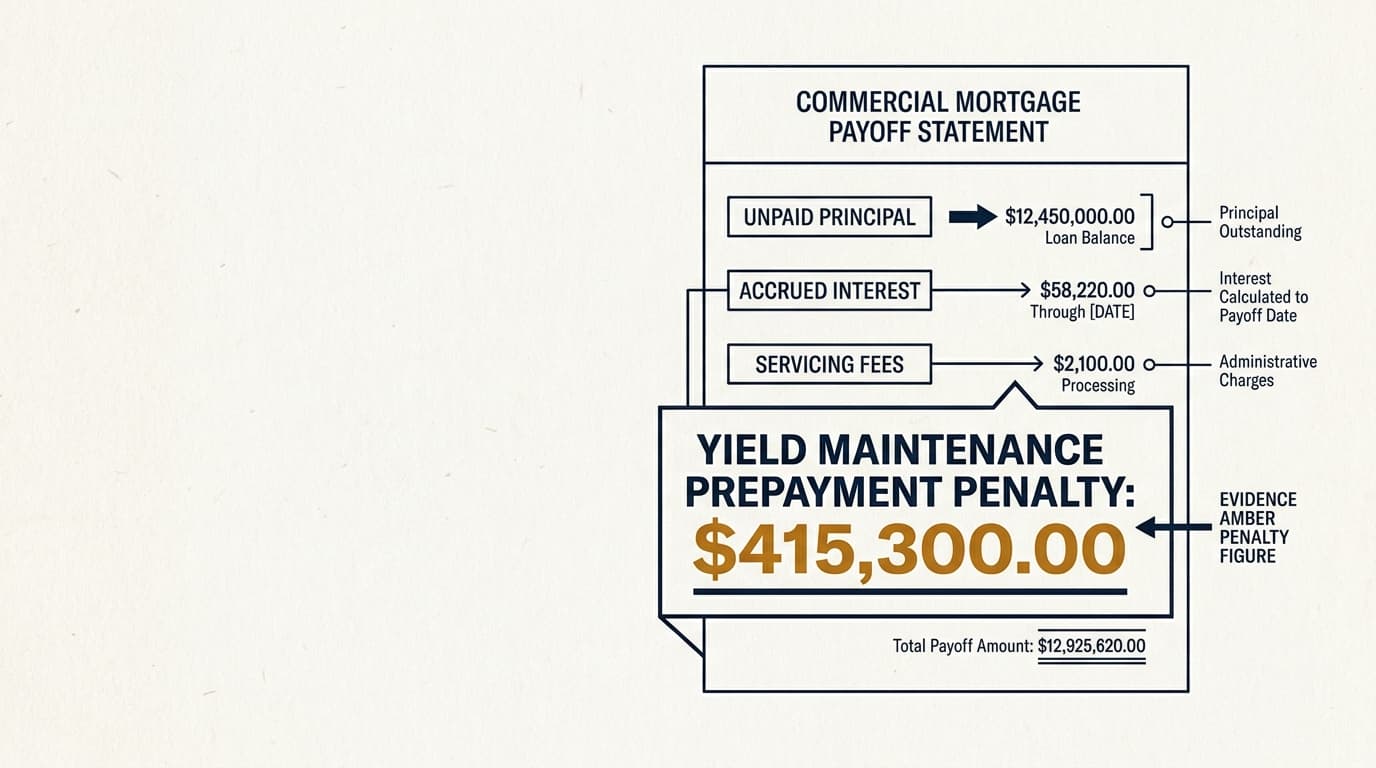

Yield Maintenance Prepayment Penalty Explained

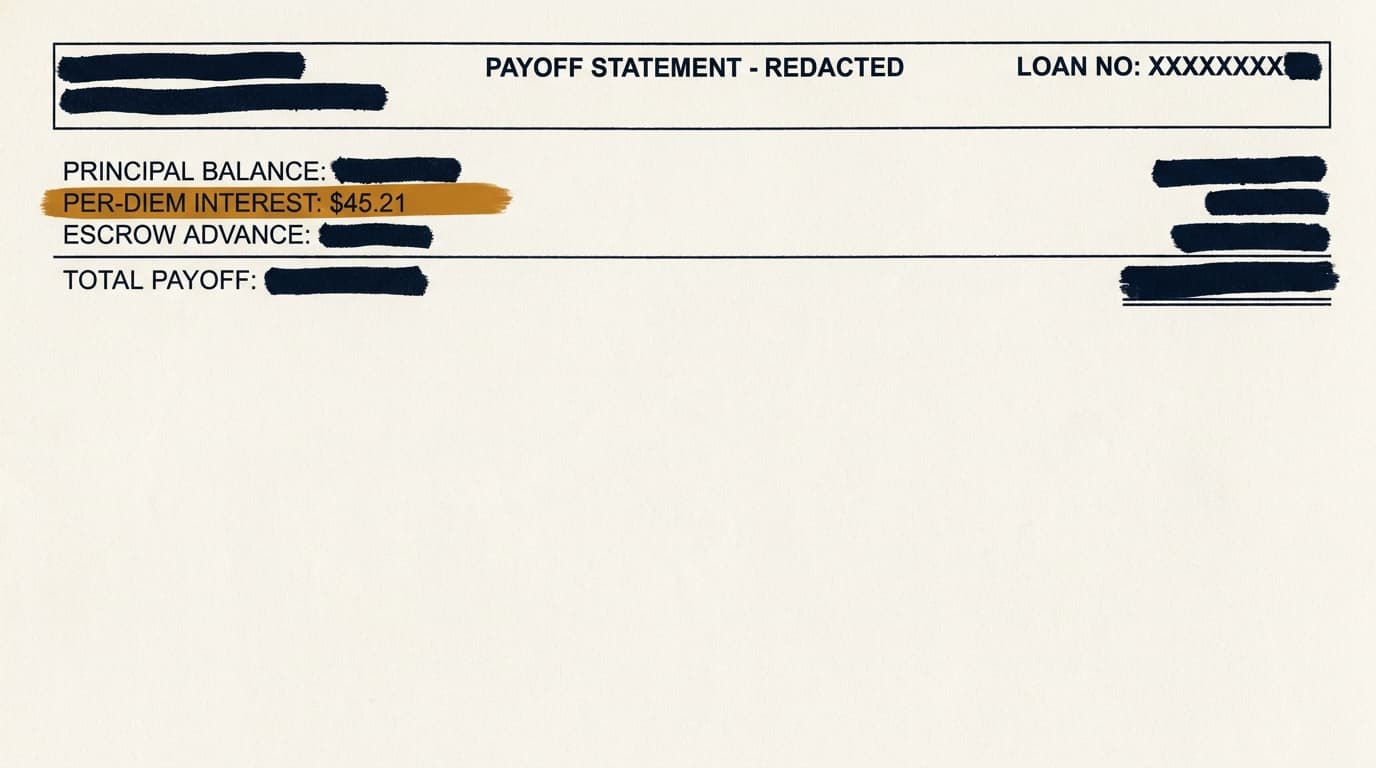

A yield maintenance prepayment penalty is the lender’s make-whole fee for paying off a commercial mortgage before it matures. In practice, the payoff statement includes unpaid principal, accrued interest, servicing fees, and a penalty that usually increases when Treasury yields fall and shrinks as the loan approaches maturity.

Yield Maintenance vs Defeasance: Cost and Timing

Yield maintenance and defeasance can lead to meaningfully different payoff costs on the same commercial real estate loan. The less expensive option depends on interest rates, time remaining on the loan, servicing requirements, securities costs, and how quickly the deal has to close.

Yield Maintenance vs Step-Down: Key Cost Differences

Yield maintenance and step-down prepayment terms can lead to very different exit costs on the same commercial mortgage. That difference shapes refinance timing, sale negotiations, and whether paying off the loan early is just a hassle or too expensive to make sense.

CMBS Yield Maintenance: Rules, Lockouts, Defeasance

CMBS yield maintenance follows pooling and servicing agreements, loan documents, and securitization timelines that work differently from portfolio loans. This guide covers how master servicers handle payoff requests, when special servicing changes the process, how lockout periods apply, and why many CMBS loans move from yield maintenance to defeasance before maturity.

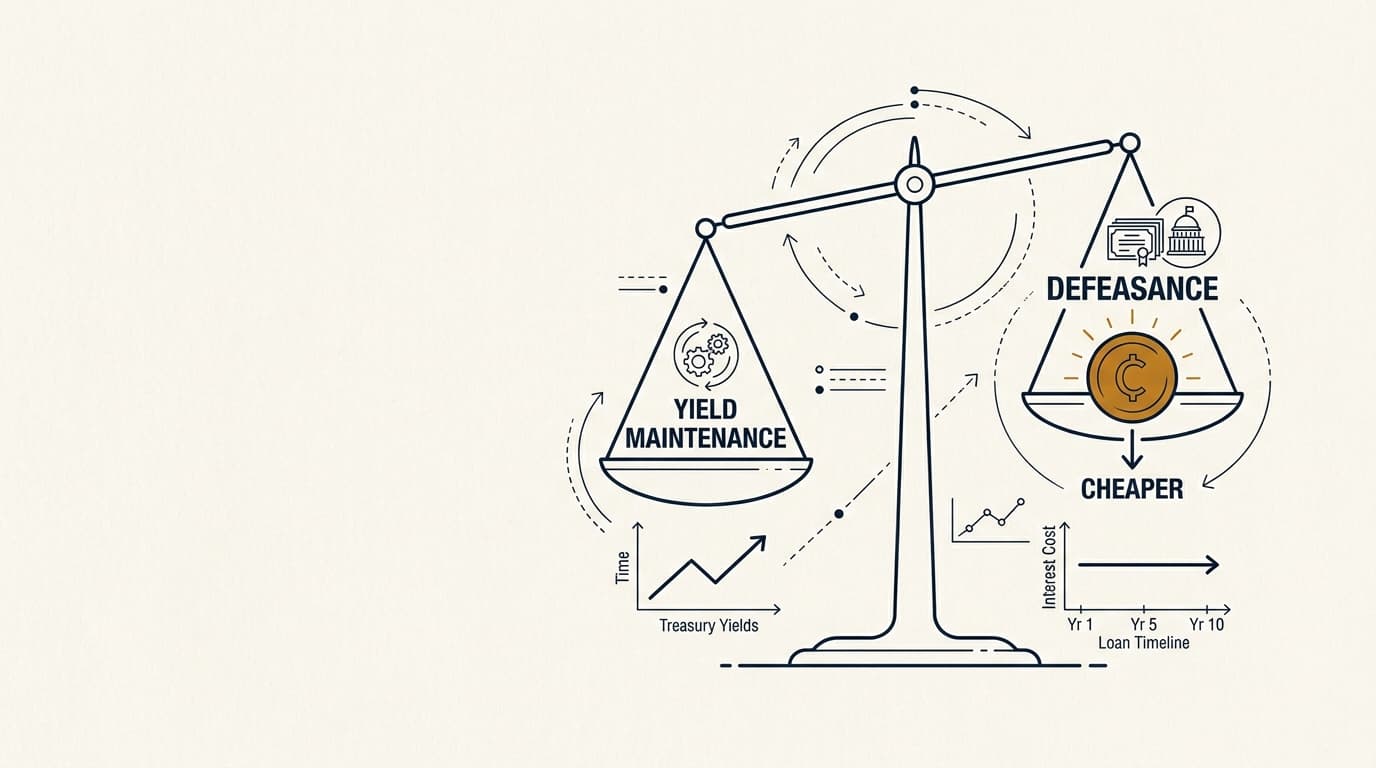

CMBS Yield Maintenance vs Defeasance: Cost Guide

For CMBS loans, the cheaper way out usually depends less on what the clause is called than on Treasury yields, time left on the loan, and transaction costs. This comparison shows when yield maintenance leads to a lower total payoff, when defeasance costs less, and which loan terms usually tip the outcome.

Yield Maintenance Before Maturity: When It Applies

Yield maintenance before maturity usually applies when a commercial borrower prepays during the protected period set out in the note, but the answer turns on the loan’s lockout language, any open-period provisions, defeasance terms, and any negotiated exceptions.

Yield Maintenance Refinance or Sale: Decide With Net Proceeds

A yield maintenance charge can swing a refinance or sale decision by hundreds of thousands of dollars. The real question is straightforward: take the higher net proceeds available today, or wait and see whether a lower penalty or a better rate environment produces stronger property-level returns.

Yield Maintenance Assumption Sale: Can It Avoid the Penalty?

A sale can avoid yield maintenance through loan assumption only if the loan documents allow it and the lender approves the buyer, the transfer structure, and the credit profile after closing. In practice, assumption usually turns a prepayment issue into an underwriting and consent issue.

Yield Maintenance in a Falling Rate Environment

Yield maintenance usually gets more expensive when Treasury rates fall: the lender has to reinvest at a lower rate, so the present value of the interest it loses goes up. This article breaks down the rate mechanics, walks through a simple model, and shows what borrowers should test before they refinance.

Yield Maintenance Borrower Negotiation: Key Clauses

Yield maintenance costs are usually locked in by the loan documents before closing. Borrowers, brokers, and counsel should pay close attention to spread floors, open-period language, Treasury selection, and assumption rights, because those terms often decide whether a future sale or refinance comes with a manageable prepayment cost or a seven-figure bill.

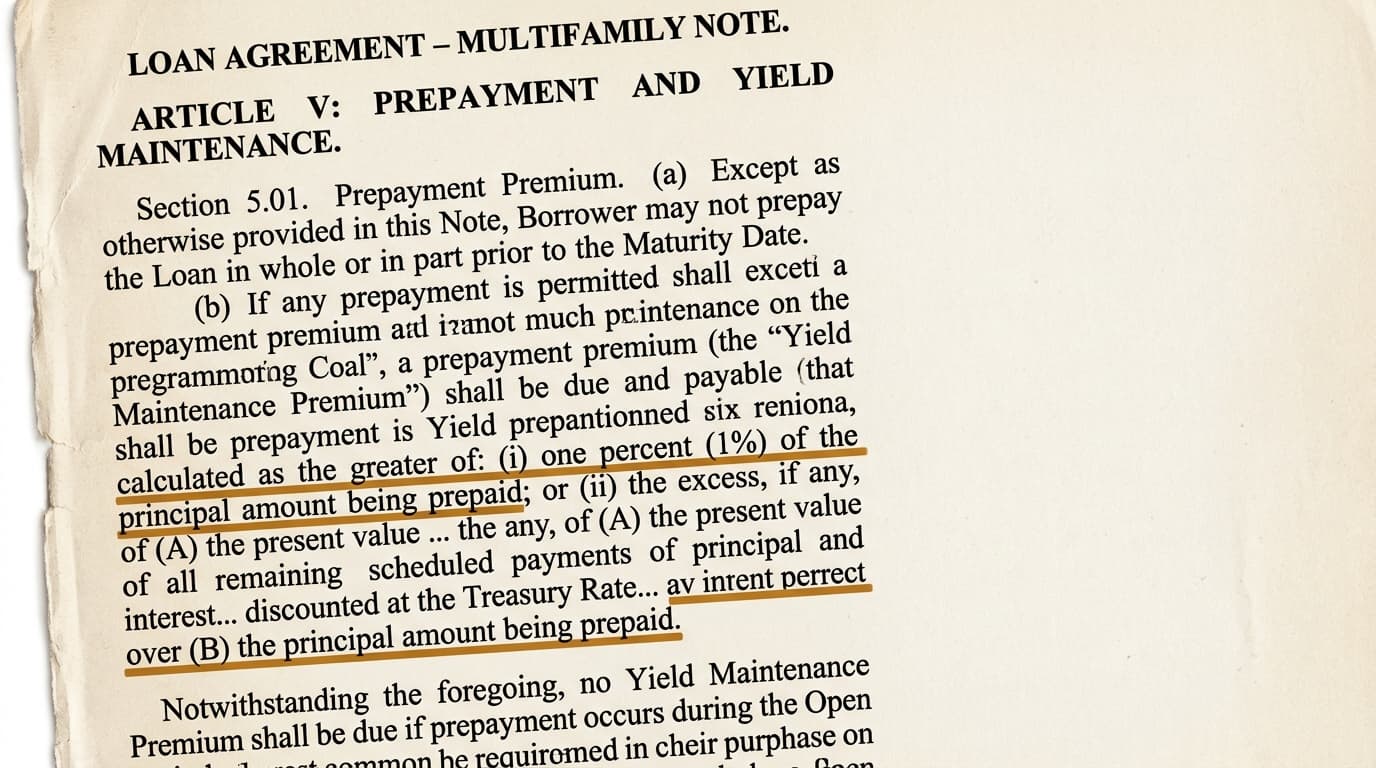

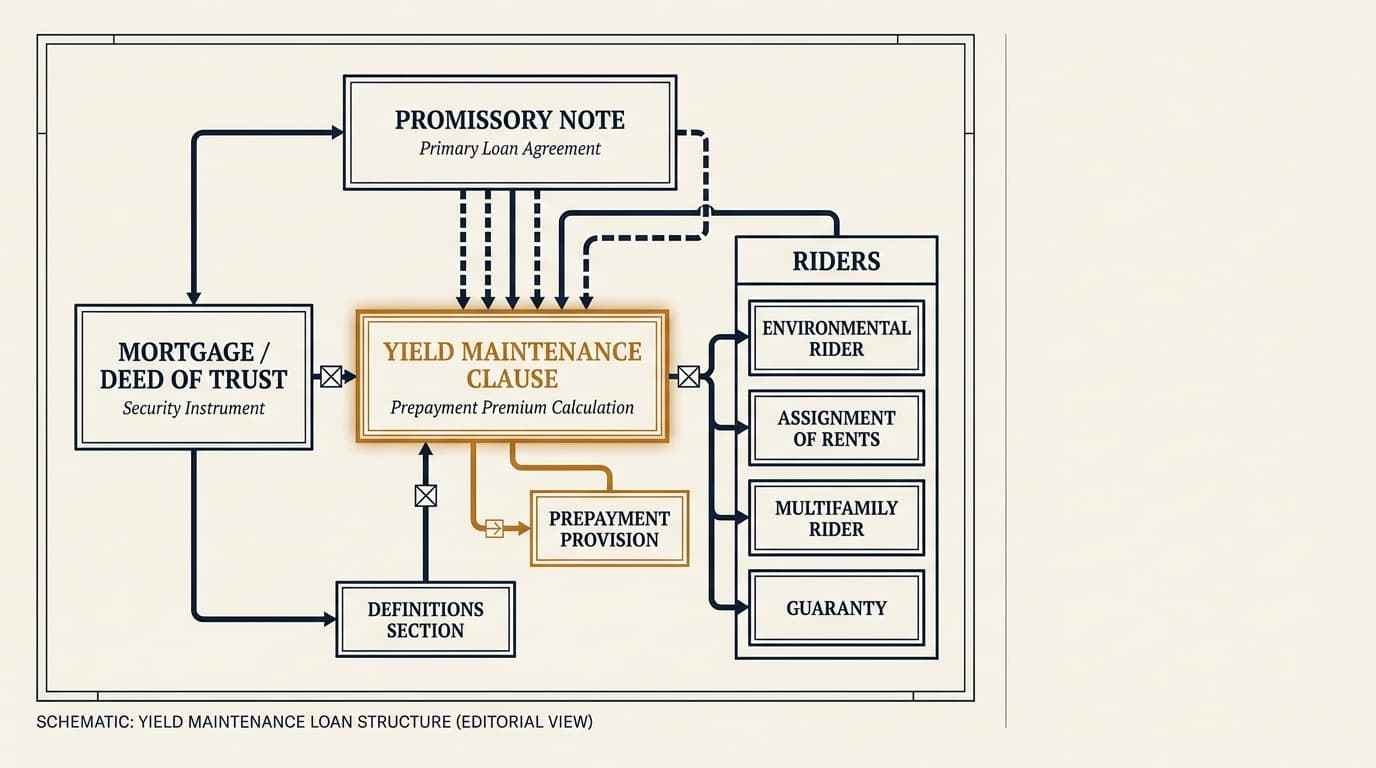

Yield Maintenance Loan Documents: What Controls Payoff

Yield maintenance usually isn’t controlled by a single clause. In most commercial real estate loans, the payoff terms are spread across the promissory note, mortgage or deed of trust, the definitions section, and any riders that change prepayment rights, Treasury selection, or notice requirements.

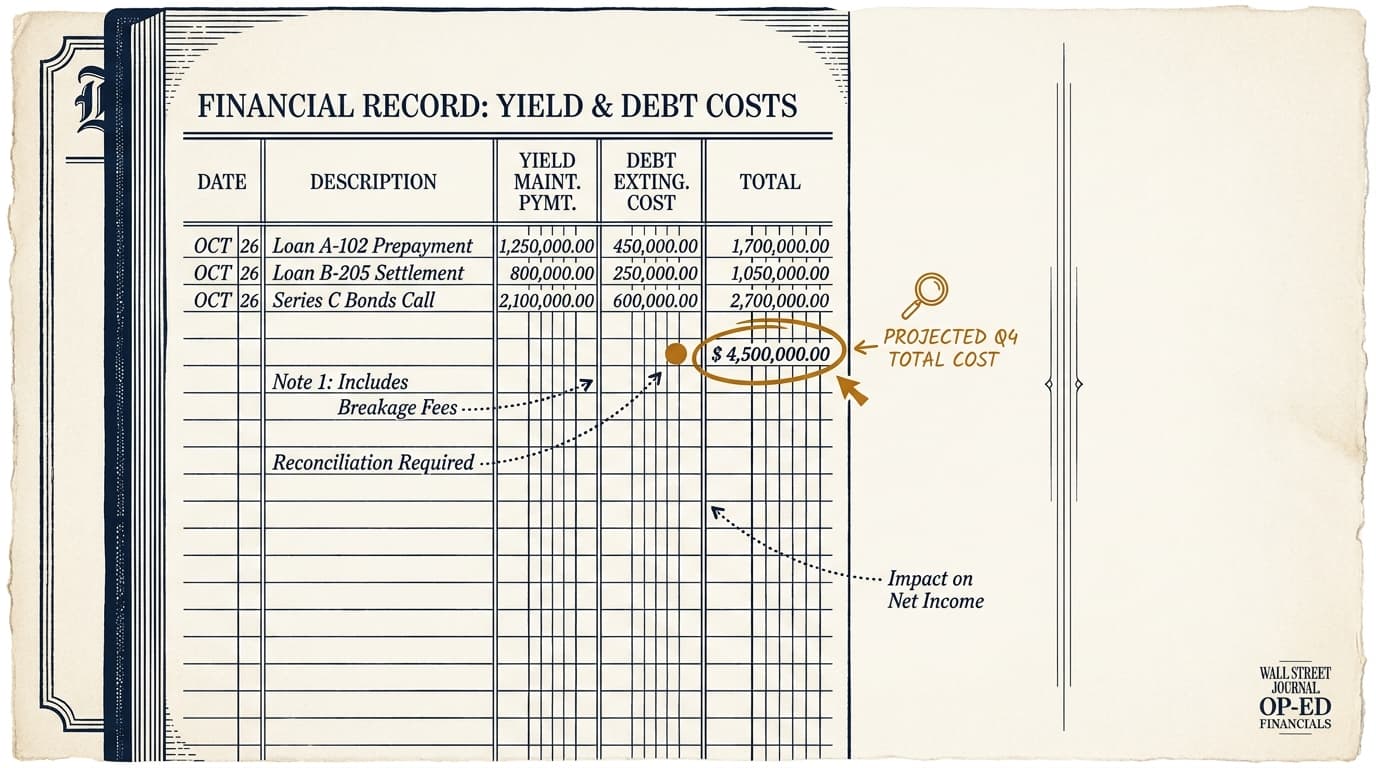

Yield Maintenance Accounting Tax Treatment Guide

Yield maintenance payments usually count as debt extinguishment costs for book purposes, but the tax treatment depends on the borrower’s facts, deal structure, and reason for paying off the loan early. This article explains how finance teams typically classify the charge, what U.S. GAAP says, and what CFOs should confirm with auditors and tax advisors before close.

Yield Maintenance Multifamily Loans: Lender Differences

Multifamily yield maintenance varies widely by lender. Agency loans, banks, and balance-sheet lenders often set different lockout periods, Treasury spreads, open windows, and defeasance options, and those differences can materially change the cost of a sale or refinance before maturity.

Yield Maintenance Office Retail: Sale Timing Guide

Office and retail owners usually run into yield maintenance at exactly the wrong time: during tenant rollover, a refinancing gap, or a sale that depends on a clean payoff. This is not just a loan-calculation issue; it can change hold strategy, leasing decisions, and whether a property can sell at all.

See the principles in production.

Graphline applies these patterns to private CRE lenders running real portfolios. Apply with one closed loan and we will show you what we see.

Apply for design partner access →