AI Agents for Portfolio Monitoring in Private CRE

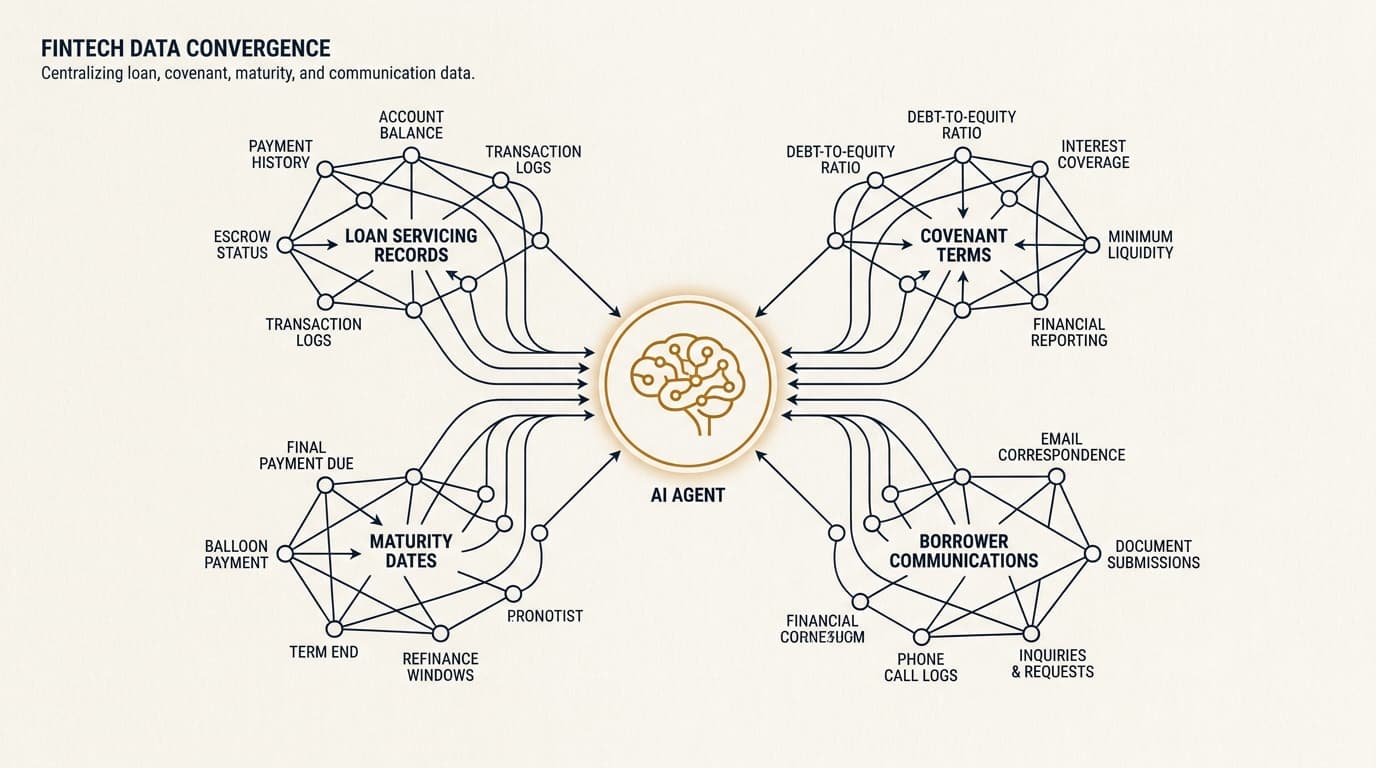

Private CRE lenders usually spot post-close risk after the fact because servicing data, covenant terms, maturity dates, and borrower communications live in different systems. AI agents for portfolio monitoring pull those records into one ongoing review process that flags covenant slippage, refinance risk, missing reporting, and escalation triggers before a loan ends up in special servicing.

Private CRE lenders usually run into the same problem after closing: payment status sits in the servicing system, covenant packages show up by email, maturity dates live in spreadsheets, and rising risk often becomes obvious only after someone misses a deadline. AI agents for portfolio monitoring are built to close that gap. They keep reading servicing activity, reporting calendars, borrower communications, and collateral updates so exposure shows up earlier, while there is still time to act.

This article breaks down how AI agents for portfolio monitoring work across a private commercial real estate loan book, with a close look at covenant compliance, maturity risk, borrower outreach, and problem-loan escalation. It also explains the operating model behind the software — how portfolio surveillance ties into servicing and asset management without dumping every exception into a manual review queue.

Key Takeaways

Private CRE portfolio monitoring usually fails at the handoff points between servicing, asset management, and borrower communication. AI agents help by watching deadlines, exceptions, and trend changes continuously instead of waiting for month-end or quarter-end.

- AI agents for portfolio monitoring work best when they pull from at least four inputs: servicing status, covenant calendars, borrower documents, and property-level performance data.

- Maturity surveillance should start 9 to 12 months before loan maturity, with separate triggers for refinance risk, extension conditions, and missing borrower response.

- Covenant monitoring is more than document intake; the system has to compare reported figures against loan agreement thresholds, prior periods, and cure windows.

- Problem-loan escalation needs an auditable rule set: who gets notified, what evidence triggered the alert, and when the case moved to watchlist or special servicing.

- The best implementations do not replace servicers or asset managers. They cut the manual tracking work so staff can spend time on judgment and borrower decisions.

AI agents for portfolio monitoring: what they do after closing

AI agents for portfolio monitoring are post-close software agents that watch a loan book for reporting deadlines, covenant breaches, maturity exposure, payment anomalies, borrower communication gaps, and asset-level deterioration. In practice, they sit between the servicing system, document repositories, email workflows, and portfolio reporting tools.

The important distinction is that portfolio monitoring is broader than servicing. A servicing team may track payments, notices, reserves, and routine requests. A portfolio monitoring agent adds surveillance logic across the whole book: Which loans are drifting toward covenant default? Which maturities are unlikely to refinance in the current market? Which borrowers have gone quiet? Which exceptions have sat unresolved for 30 days?

That is why this workflow belongs alongside basic servicing automation, not buried inside it. For broader context on the operating model across the lending lifecycle, see ai agents for private commercial real estate lending. For the post-close operational layer, the adjacent workflow is ai agents for loan servicing.

A direct answer suitable for search extraction: AI agents for portfolio monitoring are systems that continuously review post-close loan data — including covenants, maturity dates, borrower reporting, payment behavior, and collateral performance — to identify exceptions, trigger outreach, and route higher-risk loans to watchlist or asset management teams.

Why portfolio monitoring breaks down in private CRE loan books

Portfolio monitoring breaks down because private lenders usually inherit fragmented workflows, not a single surveillance system. The problem is rarely a lack of data. It is that each team sees only one slice of the file.

According to the Federal Reserve supervision and regulation framework for credit risk management, effective loan risk management depends on timely identification, measurement, monitoring, and control of credit exposure. According to the Office of the Comptroller of the Currency Comptroller's Handbook on commercial real estate lending, banks should maintain systems that track borrower performance, collateral trends, and policy exceptions over the life of the credit. Private lenders face the same operating requirement even if they are not examined the same way.

In a typical private CRE shop, four failure points come up again and again:

- Calendar risk. Reporting deadlines, insurance renewals, reserve tests, and maturities are managed in spreadsheets that are not tied to live loan status.

- Document lag. Borrowers send rent rolls, operating statements, and compliance certificates in inconsistent formats, usually by email. Review gets stuck with one analyst.

- No trend analysis. Teams check whether a package arrived, but not whether DSCR, occupancy, delinquency, or liquidity is weakening versus prior quarters.

- Weak escalation rules. An exception may get noted, but there is no standard trigger for outreach, watchlist placement, reserve action, or transfer to special servicing.

This is one reason document extraction and structured data matter upstream. If post-close packages are still trapped in PDFs, the monitoring layer does not have much to work with. That dependency is covered in more detail in ai agents for cre document analysis.

What AI agents monitor across a private CRE portfolio

A good portfolio monitoring agent does not stare at one metric. It watches a stack of operational, financial, and documentary signals that together show whether a loan is stable, deteriorating, or simply offside from an administrative standpoint.

At minimum, the monitoring stack should include the following data classes:

| Monitoring area | Typical inputs | Common trigger | Operational response |

|---|---|---|---|

| Payment and servicing status | Payment posting, delinquency aging, reserve balances, fees | Late payment, repeated short pay, reserve deficiency | Servicer review, borrower notice, asset manager alert |

| Covenant reporting | Compliance certificates, financial statements, rent rolls, T-12s | Missing package, incomplete package, threshold breach | Follow-up request, cure tracking, exception memo |

| Maturity surveillance | Maturity date, extension options, current rate environment, occupancy, sponsor response | Loan within 12 months of maturity with unresolved exit path | Refinance outreach, extension review, watchlist discussion |

| Collateral performance | NOI trend, occupancy, major tenant rollover, deferred maintenance indicators | Sharp NOI drop, occupancy decline, tenant concentration increase | Asset review, updated valuation request, site inspection |

| Borrower responsiveness | Email logs, portal activity, document submissions, call notes | No response after defined contact sequence | Escalation to relationship manager or legal notice |

According to the Federal Deposit Insurance Corporation real estate lending standards materials, prudent monitoring includes ongoing review of collateral and repayment capacity, not just payment status. In private lending, that means a performing loan can still carry real risk if reporting is stale, rollover is concentrated, or extension conditions are unlikely to be met.

AI agents for covenant compliance monitoring

Covenant compliance is where many private lenders first see the value of AI agents because the work is repetitive, date-driven, and document-heavy. The agent's job is not just to collect files. It has to determine whether the borrower met the reporting obligation and whether the reported numbers still fall within the loan agreement.

According to sample commercial mortgage credit agreement covenant structures filed with the U.S. Securities and Exchange Commission, CRE loan agreements commonly require periodic delivery of property operating statements, rent rolls, borrower financials, insurance evidence, and compliance certificates, often with event-based notices for defaults or material adverse changes. The exact thresholds vary, but the operating pattern is pretty consistent across private loan books.

How covenant monitoring actually works

A covenant monitoring agent compares three things: what the loan documents require, what the borrower submitted, and what the submission says. Those are separate checks, and each one can fail on its own.

- Obligation check. Read the loan agreement or covenant matrix and create a calendar of reporting dates, thresholds, and cure periods.

- Receipt check. Detect whether a package arrived on time, whether all required components are present, and whether the correct period is covered.

- Compliance check. Extract values such as DSCR, debt yield, occupancy, net worth, liquidity, or reserve balances and compare them with required minimums.

- Variance check. Compare current results with prior periods to spot deterioration that may not yet rise to a formal breach.

- Escalation check. Route the issue based on severity: reminder, exception log, formal default review, or sponsor call.

This process depends heavily on upstream extraction quality. Lenders building this workflow often start with post-close reporting packages after using similar extraction methods earlier in ai agents for cre loan origination and ai agents for cre underwriting.

Where manual covenant reviews miss risk

Manual covenant review often catches binary breaches and misses the trend underneath. A property that stays above a 1.15x DSCR threshold, for example, may still deserve attention if DSCR fell from 1.42x to 1.19x across two reporting periods while occupancy dropped and tenant rollover increased.

This is where AI agents do more than save labor. They can score exception severity using combined evidence instead of one breached threshold. A practical rubric might assign higher watchlist priority when three conditions show up together: declining NOI, delayed reporting, and limited borrower responsiveness. That kind of synthesis usually is not visible on the covenant certificate itself.

AI agents for maturity risk and refinance tracking

Maturity risk shows up well before the stated loan maturity date. In a higher-rate market, or just a tighter credit market, a loan can move into refinance risk 9 to 12 months before payoff if debt yield, occupancy, cash flow, sponsor support, or extension conditions are weak.

According to Mortgage Bankers Association commercial and multifamily mortgage debt resources, commercial mortgage maturities remain a major portfolio management issue as large volumes of loans come due in a market with refinancing constraints. According to Trepp market commentary on commercial real estate loan maturities and refinance conditions, refinance proceeds can be constrained by valuation pressure, lower NOI, and higher debt service assumptions. Private lenders managing bridge, transitional, or short-duration paper usually feel this first.

What a maturity agent should flag

A maturity monitoring agent should not rely on date alone. It should score exit risk using loan structure, current property performance, and sponsor engagement.

| Signal | Why it matters | Example trigger |

|---|---|---|

| Months to maturity | Starts outreach and refinance planning | 12, 9, 6, and 3-month milestones |

| Extension conditions | Determines whether borrower has a realistic contractual path | Minimum DSCR not met or extension fee unpaid |

| Updated property cash flow | Affects refinance sizing | NOI down 15% from underwritten level |

| Leasing rollover | Affects lender confidence and valuation | 30% of NRA rolls within 12 months |

| Sponsor responsiveness | Shows whether payoff planning is actually active | No response after two outreach cycles |

For lenders with concentrated bridge exposure, this analysis often belongs with dedicated ai agents for watchlist and maturity management logic rather than generic servicing reminders.

Decision framework for maturity triage

Maturity triage should separate loans into operational categories, not one generic “upcoming maturity” list. That gives asset management something they can actually use.

- Category 1 — expected payoff. Stable property, responsive sponsor, refinance or sale process already underway.

- Category 2 — likely extension request. Sponsor engaged, asset improving, but extension conditions need review.

- Category 3 — refinance gap risk. Performance or leverage suggests conventional takeout may come up short.

- Category 4 — workout candidate. Deteriorating operations, weak response, unresolved defaults, or no clear exit.

These categories matter because they map to different staffing actions. Category 1 may stay with servicing. Category 2 usually needs asset management review. Category 3 often needs valuation and sponsor liquidity analysis. Category 4 may require legal, reserves, and transfer planning. A maturity agent earns its keep by routing loans into those lanes early instead of producing a static date-based report.

Borrower outreach and follow-up workflows

Borrower outreach is part of portfolio monitoring because missing reporting and unresolved maturities usually start as communication failures before they become credit failures. The system should log contact attempts, deadlines, borrower responses, and unresolved items in a form that both servicing and asset management can use.

According to the Consumer Financial Protection Bureau mortgage servicing compliance resources, servicing communications and loss mitigation workflows require reliable records of notices and borrower interactions. Private commercial lending works differently, but the basic discipline — keeping a complete communication trail — applies just as much to workout and maturity management.

A practical outreach ladder usually includes:

- Initial reminder with the specific missing item and due date.

- Second notice that references the governing covenant or extension requirement.

- Relationship-manager escalation if there is no response after the defined interval.

- Formal notice or default review if the cure period expires.

The AI agent's role is to trigger, personalize, and log these steps using current loan facts. Staff may still approve the actual communications, especially once legal language or default remedies enter the picture. Lenders that want this workflow as its own operating layer should pair monitoring with ai agents for loan servicing, while borrower-facing messaging logic can sit separately from this page's topic.

Problem-loan escalation and watchlist management

Problem-loan escalation should start with defined triggers, not analyst intuition alone. The goal is consistency. Two loans with the same risk pattern should reach the same review path, with a clear record of why the system flagged them.

According to the Office of the Comptroller of the Currency Comptroller's Handbook on problem assets, institutions should identify problem credits early, maintain watchlists, document action plans, and monitor progress against those plans. That translates directly to private CRE lending operations.

Common escalation triggers in private CRE

Most lenders have some version of a watchlist, but the trigger logic is often inconsistent across teams. A portfolio monitoring agent can standardize the handoff with a rule stack.

- Administrative triggers: repeated late reporting, expired insurance evidence, missing tax confirmation, unresolved reserve shortfall.

- Credit triggers: DSCR breach, occupancy decline, large tenant rollover, declining collections, repeated delinquency.

- Behavioral triggers: borrower stops responding, disputes operating numbers, refuses inspection access, changes management without notice.

- Event triggers: maturity inside six months without an exit plan, unpaid maturity extension fee, casualty event, litigation, bankruptcy filing.

What good escalation looks like in practice

A useful escalation record should include the triggering data, source document, date detected, assigned owner, required next action, and review deadline. That sounds basic because it is basic, but many private lenders still manage special situations through email threads and ad hoc comments in the servicing system.

An auditable workflow matters for governance as much as operations. If a lender later needs to explain why one loan stayed in ordinary servicing while another moved to workout, the system should be able to show the exact evidence and rule path. Governance considerations overlap with ai agents for cre lending compliance, particularly where policy exceptions, borrower privacy, and model controls are involved.

How servicing data connects to asset management workflows

Portfolio monitoring only creates value if servicing data and asset management action are connected. A sharp alert that does not change who works the file, what documents get requested, or whether a strategy memo gets prepared is just another dashboard notification.

The operating model usually looks like this:

- Servicing system supplies status data. Payments, delinquencies, reserves, fees, maturities, notices, and borrower contact records flow into the monitoring layer.

- Document system supplies evidence. Compliance certificates, rent rolls, operating statements, leases, and insurance files are extracted and structured.

- Monitoring agent scores the loan. Rules and models classify issues by type, severity, and urgency.

- Work queue routes the case. Administrative exceptions stay with servicing; credit deterioration goes to asset management; legal defaults move to counsel or workout.

- Resolution outcome writes back. The decision, action plan, and next review date update the system of record.

This architecture is one reason lenders should be precise about workflow boundaries. The agent that supports post-close monitoring is not the same system that handles intake or underwriting, even if they share extracted data. Readers comparing lifecycle handoffs may want the separate views on ai agents for borrower intake and cre loan origination workflow ai agent.

A practical rollout framework for private lenders

Private lenders usually get better results by implementing portfolio monitoring in stages instead of trying to automate the entire book at once. The first phase should focus on the highest-friction post-close tasks with clear data sources and obvious escalation paths.

- Inventory the data sources. Map servicing fields, document repositories, covenant matrices, outreach logs, and watchlist reports.

- Define the trigger library. List the exact conditions for late reporting, covenant breach, maturity review, watchlist transfer, and reserve issues.

- Normalize the evidence. Standardize how the system stores submission dates, reporting periods, covenant values, borrower responses, and exception notes.

- Set ownership rules. Decide which triggers stay with servicing and which move to asset management, credit, or legal.

- Run parallel review. Compare agent-generated alerts against analyst review for a limited portfolio segment before broader rollout.

- Audit the outputs. Test false positives, missed alerts, timing lags, and documentation quality.

The point is not to automate every judgment call. It is to make sure no deadline, package, or deterioration signal disappears between teams.

What to measure: KPIs and control points

Portfolio monitoring programs should be measured by detection speed, exception resolution, and transfer quality, not just task volume. A lender can send thousands of reminders and still miss the loans that actually need intervention.

Useful KPIs include:

- Reporting timeliness rate: percent of required packages received by due date.

- Covenant review cycle time: average days from package receipt to pass, exception, or escalation.

- Exception aging: number of unresolved exceptions over 15, 30, and 60 days.

- Maturity readiness rate: percent of loans with documented payoff or extension strategy 6 months before maturity.

- Watchlist precision: share of escalated loans that required asset management action, a useful proxy for alert quality.

The most overlooked control point is evidence traceability. For each alert, staff should be able to answer five questions quickly: What triggered it? Which document or field supported it? When was it detected? Who reviewed it? What action was taken? If the system cannot answer those questions, the portfolio monitoring layer is not ready for audit or exam-style review.

Frequently Asked Questions

What are AI agents for portfolio monitoring in private CRE lending?

AI agents for portfolio monitoring are post-close systems that continuously review loan data, borrower reporting, maturity dates, servicing activity, and collateral performance to identify exceptions and route them to servicing, asset management, or workout teams. In private CRE lending, they are most often used for covenant compliance, maturity surveillance, outreach tracking, and watchlist escalation.

How early should a private lender start maturity monitoring?

Most lenders should begin formal maturity monitoring 9 to 12 months before the stated maturity date, with stronger review at 6 months and 3 months. Short-duration bridge loans may need earlier review if extension conditions are tight or the business plan has slipped. The right timing depends on asset type, sponsor quality, lease rollover, and current refinance conditions.

How does portfolio monitoring differ from loan servicing?

Loan servicing focuses on routine post-close administration such as payments, notices, reserves, and borrower requests. Portfolio monitoring uses that servicing data, plus financial reporting and collateral information, to assess broader credit exposure across the loan book. A loan can be current from a servicing perspective and still carry elevated portfolio risk if cash flow is weakening or maturity refinance prospects are poor.

Which loans usually need the most intensive monitoring?

Transitional assets, bridge loans, construction-to-stabilization exposures, loans with near-term maturities, and credits with reporting gaps usually need the closest monitoring. Properties with tenant concentration, rollover exposure, or declining occupancy also deserve tighter review because the refinance outlook can change quickly even without a payment default.

Does portfolio monitoring vary by market or region?

Yes. Regional market conditions affect refinance availability, property valuations, leasing trends, insurance costs, and borrower exit options. Office exposure in gateway markets, for example, may need different maturity assumptions than multifamily loans in supply-constrained Sun Belt markets. Lenders should calibrate watchlist thresholds and maturity outreach based on local market liquidity, asset type performance, and state-specific legal timelines for default remedies.