CRE Loan Origination Workflow AI Agent Guide

A CRE loan origination workflow AI agent can screen inbound deals, gather the required documents, move tasks through the LOS or CRM, and assemble a credit-ready file for human review. The real value isn’t full automation; it’s shorter cycle times, fewer handoff mistakes, and a clear record of what the system did at each step.

Private CRE lenders usually do not lose time on one big underwriting call. The drag comes from dozens of small handoffs during origination: intake, document chasing, data entry, task routing, and file prep. A CRE loan origination workflow AI agent is basically an orchestration layer for those repeatable steps inside an existing loan origination system or customer relationship management platform. It moves the file forward, keeps a record of what happened, and hands a clean package to a human reviewer. This article lays out the exact workflow, where the agent belongs, what it should and should not automate, and how private lenders are putting these controls into production in 2026.

Key Takeaways

- A CRE loan origination workflow AI agent is most useful before formal underwriting starts: lead qualification, document collection, task routing, and file packaging.

- The highest-value setup usually connects email, borrower portal, LOS, CRM, and document storage instead of trying to replace them.

- Human review should stay in place for credit judgment, policy exceptions, pricing decisions, and adverse-action or declination communications.

- The strongest model is event-driven: each borrower action, missing document, or status change triggers a logged next step.

- Private lenders should measure results with pull-through, time-to-complete intake, document defect rates, and touches per file, not generic AI metrics.

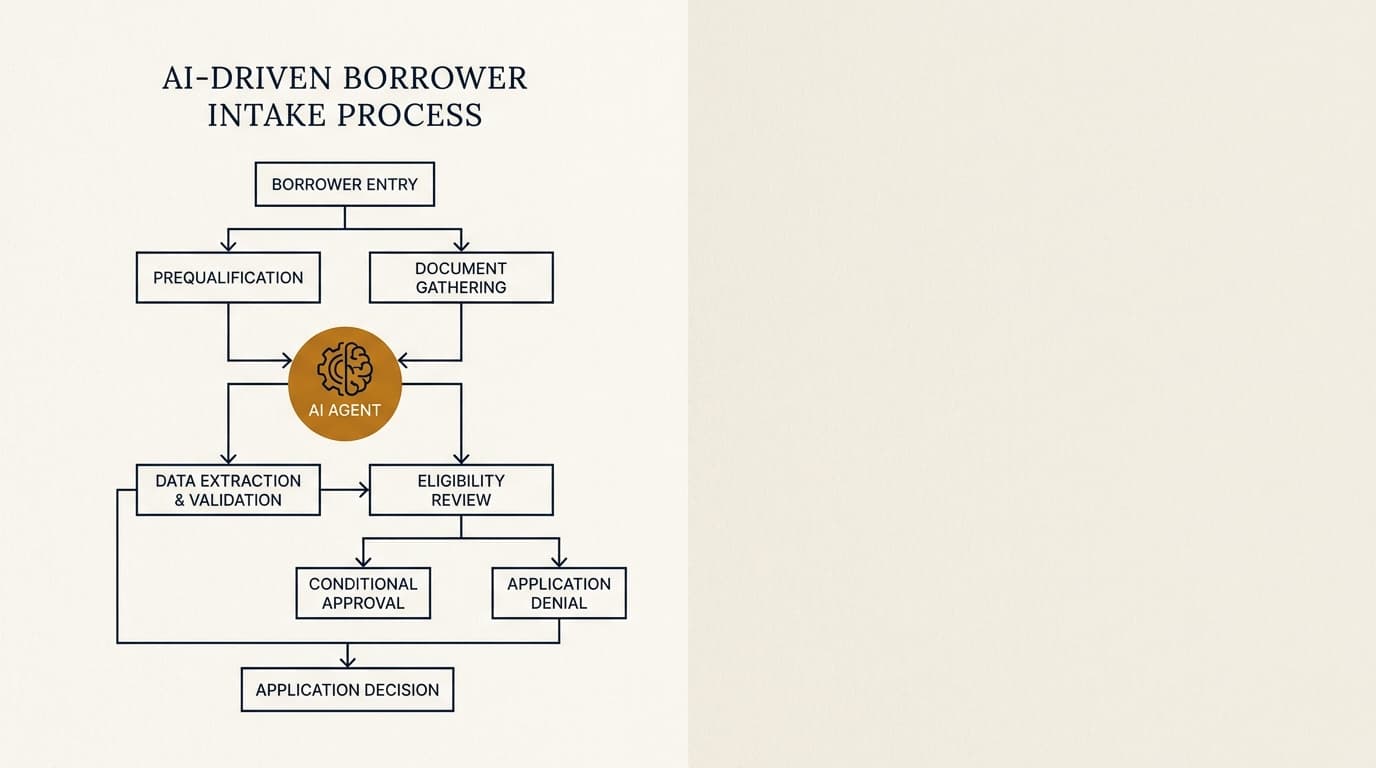

What a CRE loan origination workflow AI agent does

A CRE loan origination workflow AI agent does not replace a credit team. It watches intake events, applies lender-specific rules, requests missing information, updates records, and assembles a standardized package for the next human decision.

In practice, the agent sits between inbound opportunity creation and full underwriter review. A borrower or broker submits a scenario by email, form, or portal. The agent reads the submission, identifies the property type, loan purpose, location, sponsor profile, and stated leverage, then checks those facts against lender rules. According to the Consumer Financial Protection Bureau's Equal Credit Opportunity Act resources, creditors need controlled, consistent processes around application handling and decisioning. For private CRE lenders, a documented workflow beats a loosely supervised inbox every time.

The workflow usually has four layers:

- Qualification against basic box rules.

- Document collection and deficiency management.

- Task routing into the LOS or CRM.

- Preparation of a credit-ready file with a traceable activity log.

For a broader market view, see Graphline's pillar on ai agents for private commercial real estate lending.

Where the agent fits in a private lender's origination stack

The agent works best as a middleware layer tied to the systems of record. Most private lenders already run origination through some mix of CRM, shared inboxes, document storage, and a loan origination system, not a single end-to-end platform.

That matters because workflow failures are usually integration failures. The agent should not turn into a shadow LOS. It should write back only approved fields, preserve source documents, and keep a timestamped record of every action taken. According to the Federal Financial Institutions Examination Council guidance on architecture, infrastructure, and operations, data flows, change management, and logging still need governance in technology-enabled processes. Even if a private debt fund is not examined like a bank, that is still a sensible baseline.

A common stack looks like this:

| Layer | Typical system | Agent function | Output |

|---|---|---|---|

| Lead capture | CRM, web form, email inbox | Parse inquiry, create opportunity, assign owner | Structured lead record |

| Intake | Portal, email, shared drive | Request checklist, track missing items, validate uploads | Complete intake package |

| Data standardization | LOS, spreadsheet, document repository | Normalize fields and map documents to required categories | Clean file for review |

| Triage | CRM or LOS queue | Route to analyst, originator, counsel, or exception queue | Task assignment and SLA clock |

| Pre-underwriting prep | Credit memo template, LOS | Assemble summary and evidence links | Human-ready package |

That is narrower than a full ai agents for cre loan origination strategy. This page stays focused on the workflow layer inside that broader function.

CRE loan origination workflow: exact step-by-step sequence

The best workflow is event-driven and sequential. Each step should produce a clear output, and no step should silently overwrite source data.

- Capture the incoming scenario from email, form, broker package, or borrower portal.

- Extract core fields such as property address, property type, requested loan amount, purpose, occupancy, sponsor, and timeline.

- Check those fields against lender rules for geography, product, leverage, asset type, and minimum data sufficiency.

- Create or update the opportunity in the CRM and LOS using approved field mappings.

- Request the required documents based on the scenario, such as rent roll, trailing-12 financials, operating statement, purchase contract, existing debt details, borrower organizational documents, and property photos.

- Validate incoming files for completeness, recency, legibility, and document type.

- Route exceptions, missing items, or policy mismatches to the right owner.

- Prepare a standardized file summary with source links, open issues, and confidence flags.

- Escalate the file for human review once the required threshold is met.

This sequence looks simple on paper. The real gain comes from cutting rework. According to the Mortgage Bankers Association's performance reporting resources, lender production costs are heavily shaped by manual process inefficiency and fallout. Private CRE lenders deal with the same friction, even if the product mix differs from agency or consumer lending.

Example: bridge loan intake

A light-transitional multifamily bridge request is a good example of where the workflow agent helps. A broker sends a five-page teaser, twelve trailing months, a current rent roll, and a target closing date in 21 days.

The agent can spot that the package is missing ownership structure documents and a borrowing entity chart, classify the request as bridge rather than stabilized term debt, and send it to the correct product queue. It can also flag timing risk because a 21-day target close leaves little room for diligence and legal work. That kind of triage belongs in workflow. It does not require the system to make a final credit decision. For a product-specific discussion, see the related page on ai agents for borrower intake.

Workflow map: tasks, systems, outputs, and human checkpoints

An auditable workflow needs explicit checkpoints. The handoff to humans should happen where judgment, policy interpretation, or legal significance starts.

| Stage | AI agent task | Human checkpoint | Why the checkpoint matters |

|---|---|---|---|

| Initial triage | Read scenario and classify product fit | Originator reviews edge cases | Mixed-use, transitional, or cross-collateral deals are often misclassified by simple rules |

| Document collection | Request and track missing items | Analyst confirms sufficiency | A file can look complete and still be unusable for underwriting |

| Data entry | Map extracted data into LOS fields | Operations reviews high-impact fields | Loan amount, entity names, and collateral address drive downstream documents |

| Exception handling | Flag out-of-box LTV, DSCR, or geography | Credit officer decides treatment | Policy exceptions need a documented owner |

| File packaging | Build summary and evidence index | Underwriter accepts into queue | Prevents incomplete files from distorting underwriting cycle times |

This is also where workflow touches adjacent functions such as ai agents for cre underwriting and later-stage ai agents for loan servicing. The boundary should be clear: origination workflow prepares the file, underwriting evaluates risk, and servicing handles post-close administration.

What should stay with humans vs the AI agent

Credit judgment should stay with humans. Workflow AI is strongest at orchestration, completeness checks, standardized communications, and queue management.

Private lenders usually get better results when they separate three functions:

- Agent-owned tasks: checklist generation, follow-up reminders, file naming, metadata tagging, status updates, and routing.

- Shared tasks: issue spotting, preliminary rule checks, document anomaly flags, and memo drafting.

- Human-only tasks: pricing, structure selection, waiver decisions, policy exceptions, legal interpretations, and final go/no-go calls.

According to the National Institute of Standards and Technology AI Risk Management Framework, high-impact uses of AI need governance, oversight, and accountability that match the consequences of errors. In lending operations, the practical takeaway is straightforward: use the agent to cut clerical delay, not to bury consequential judgment inside a black box.

How to implement without disrupting your LOS or CRM

The safest rollout starts with one origination lane, one checklist standard, and one approval path for write-backs. Most failed deployments try to automate every product and every exception at the same time.

A workable rollout sequence is:

- Select one high-volume product lane, such as stabilized multifamily or bridge refinances.

- Define the minimum data set required before a file moves from intake to analyst review.

- Map every inbound document type to a system field, storage location, owner, and exception rule.

- Limit write access so the agent can update only approved fields and task statuses.

- Log every extraction, request, reminder, and field change with a timestamp and source reference.

- Review 50 to 100 files manually to establish baseline defect rates and cycle times.

- Expand only after the workflow produces stable completeness rates and clean audit logs.

The important point here is sequencing. A lot of lenders evaluate AI on model accuracy alone. In origination, throughput usually depends more on queue design and exception ownership than on extraction performance. A system with 95% extraction accuracy still fails if unresolved exceptions sit in the wrong queue for two days. That is not an AI problem. It is an operating model problem.

Common failure points in origination workflow automation

Most origination workflow failures come from weak data governance, not poor prompting. The recurring issues are duplicate records, unclear document standards, silent field overwrites, and no owner for exceptions.

Three edge cases deserve extra attention:

- Broker-submitted packages with inconsistent naming. The agent may identify every file correctly and still attach them to the wrong deal if duplicate borrower names already exist in the CRM.

- Entity-heavy sponsorship structures. A single loan may involve guarantors, borrowing entities, SPEs, and property managers. The workflow needs relationship logic, not just field extraction.

- Fast-close requests. Compressed timelines may justify a different checklist and escalation path. Otherwise, the standard chase cadence slows the file down.

According to the U.S. Government Accountability Office reporting on AI governance and risk management, organizations adopting AI systems still run into data quality, transparency, and oversight problems. In CRE origination, those issues usually show up first as operational mistakes, long before anyone argues about model performance.

Frequently Asked Questions

What is a CRE loan origination workflow AI agent?

A CRE loan origination workflow AI agent is a software layer that handles repeatable origination tasks such as intake triage, document requests, status tracking, task routing, and file preparation before human underwriting review. It usually works inside or alongside a lender's CRM, LOS, email, and document systems rather than replacing them.

Can a workflow AI agent make credit decisions for private CRE loans?

It can apply preliminary rules and flag out-of-box scenarios, but final credit decisions, pricing, and exceptions should stay with human reviewers. That split supports auditability and lowers the risk of making a high-impact lending judgment through an opaque automated process.

How does this workflow differ from AI underwriting?

Workflow AI prepares and routes the file. Underwriting AI analyzes risk once the file is ready. In practice, workflow covers lead qualification, document collection, deficiency tracking, and system updates, while underwriting covers cash flow review, leverage analysis, policy exceptions, and recommendation support.

What systems should a private lender connect first?

Most lenders start with the systems that create intake friction: shared inboxes, the borrower portal, CRM, document storage, and the LOS. Those connections usually produce faster gains than more advanced model features because they cut duplicate data entry and shorten document chase cycles.

Does workflow design vary by market or loan type?

Yes. A bridge lender in New York or California may need faster exception routing for entity structures, legal review, and closing timelines than a lender focused on stabilized multifamily in secondary markets. Geography, counsel requirements, title practices, and product type all affect the checklist, escalation path, and turnaround expectations.