Yield Maintenance Prepayment Penalty Explained

A yield maintenance prepayment penalty is the lender’s make-whole fee for paying off a commercial mortgage before it matures. In practice, the payoff statement includes unpaid principal, accrued interest, servicing fees, and a penalty that usually increases when Treasury yields fall and shrinks as the loan approaches maturity.

Most borrowers don’t really feel yield maintenance until the payoff statement shows up. The note says 6.25%, but the wire required to retire the loan early can be hundreds of thousands of dollars higher once unpaid principal, accrued interest, and the make-whole charge are added. This article breaks down how a yield maintenance prepayment penalty works in an actual payoff, when it gets triggered, how payoff statements are built, and which variables tend to push the cost up or down in 2026.

Key Takeaways

- Yield maintenance usually applies when a fixed-rate commercial loan is paid off before scheduled maturity, subject to any lockout, open period, or defeasance terms in the loan documents.

- A payoff statement typically includes unpaid principal, accrued interest, default interest if applicable, servicing or statement fees, and the yield maintenance prepayment penalty.

- The penalty usually gets larger when the loan coupon is high, the remaining term is long, and the lender’s reinvestment benchmark — often a U.S. Treasury rate — is low.

- The penalty usually shrinks as the loan gets closer to maturity and may drop to zero during a contractual open window, but the result depends on the note and rider language.

- Before wiring funds, borrowers should verify the calculation date, remittance date, benchmark rate, spread, and per diem interest.

What is a yield maintenance prepayment penalty?

A yield maintenance prepayment penalty is a contractual make-whole payment. It compensates the lender for losing an above-market loan before maturity. In most commercial real estate loans, the charge estimates the present value of the lender’s lost interest stream against a reinvestment benchmark, often based on a U.S. Treasury yield plus a spread set in the loan documents.

According to the Freddie Mac Multifamily Seller/Servicer Guide section on yield maintenance, yield maintenance is meant to preserve the lender’s expected yield when a mortgage is prepaid before maturity. The Fannie Mae Multifamily loan document resources make the practical point: the note and rider decide whether prepayment is prohibited, allowed only with a premium, or allowed during a specified period. That language controls whether a payoff can happen at all and what extra amount has to be wired.

For a broader overview of commercial real estate yield maintenance, including how it compares with other exit structures, the pillar page covers the bigger picture. This article stays focused on the part borrowers actually have to fund: what the penalty means once a real payoff statement is in play.

Featured snippet answer: A yield maintenance prepayment penalty is the make-whole amount a commercial borrower pays to retire a loan before maturity. The payoff statement usually includes principal, accrued interest, fees, and a penalty tied to the remaining scheduled interest stream, discounted using a Treasury-based benchmark specified in the loan documents.

When is a yield maintenance prepayment penalty triggered?

The penalty is triggered when the borrower pays the loan off before the documents allow a no-premium payoff. The exact trigger comes from the note, deed of trust or mortgage, prepayment rider, and any servicing instructions.

The Freddie Mac Multifamily Seller/Servicer Guide provisions on prepayment tie the ability to prepay, and the applicable premium, to the mortgage terms and the point in the loan term. Fannie Mae Multifamily guidance on mortgage loan maturity and prepayment administration makes the servicing side clear: payoff requests are administered under the governing loan documents and servicing rules.

Common triggers include:

- Refinancing before maturity. A new lender pays off the old fixed-rate loan, which triggers the premium unless the loan is already in an open period.

- Sale with debt repayment. If the buyer does not assume the existing debt and the sale closes before maturity, the seller usually owes the premium at payoff.

- Voluntary early retirement. A sponsor may use cash, recap proceeds, or a portfolio restructuring to retire the debt.

- Casualty or condemnation scenarios. Some documents treat prepayment differently after a taking or major casualty. Others waive it. You have to read the documents.

Lockout, open period, and default status matter

The same loan can produce very different payoff numbers depending on timing and status. A loan may ban prepayment during a lockout, allow it with yield maintenance for several years, and then become open during the final 90 days or six months before maturity.

The Consumer Financial Protection Bureau discussion of prepayment penalties in Regulation Z commentary explains the basic principle: whether a charge counts as a prepayment penalty depends on the contractual charge imposed on early payment. Commercial mortgage servicing is not governed the same way as consumer mortgage disclosures, but the core idea is the same. The obligation comes from the contract. If the loan is in default, the payoff may also include default interest, legal fees, or protective advances. Those are separate from yield maintenance, and they can move the total wire by a lot.

If the broader question is whether the charge applies at a particular point in the term, the related page on yield maintenance before maturity goes deeper on timing.

How payoff statements are prepared for a yield maintenance loan

A payoff statement is an itemized demand showing the exact amount required to retire the debt on a stated date. For a yield maintenance loan, the servicer or lender usually calculates principal, interest, fees, and the prepayment premium as of a specific remittance date, then adds a daily interest amount if funding happens later.

Uniform Commercial Code section 9-210 gives a debtor the right to request an accounting or payoff amount in secured transactions, although commercial mortgage practice is ultimately governed by the loan documents and servicing standards. The Freddie Mac Multifamily servicing guide on mortgage payoff statements also makes clear that payoff figures are issued subject to stated assumptions, timing, and remittance instructions. In institutional CRE lending, the statement usually comes from the master servicer, special servicer, portfolio lender, or loan administrator — not just closing counsel.

Typical components of the payoff statement

Most yield maintenance payoff statements include the same core line items. The labels may change. The economics usually do not.

| Line item | What it covers | Why it matters |

|---|---|---|

| Unpaid principal balance | Outstanding loan amount | This is the base amount that has to be retired in any payoff. |

| Accrued interest | Interest from the last payment date through the payoff date | Per diem accrual can add several days of cost if funding slips. |

| Yield maintenance premium | Make-whole charge under the note or rider | This is often the largest variable cost in an early payoff. |

| Servicing or payoff statement fee | Administrative fee for preparing the demand | Usually small relative to the premium, but still part of the wire. |

| Default interest | Extra interest if the loan is in default | Can increase the payoff materially, separate from the prepayment premium. |

| Protective advances or legal fees | Taxes, insurance, legal expenses, or advances made by lender/servicer | Often missed until the final statement is issued. |

Step-by-step payoff process

The payoff process follows a pretty standard sequence, and date mistakes often change the final number as much as calculation mistakes do. Most disputes are not about whether the clause exists. They are about dates, benchmark selection, or charges that were not accounted for early enough.

- Review the note, prepayment rider, and servicing notices to confirm whether prepayment is permitted on the target date.

- Request a formal payoff statement from the lender or servicer with the intended funding date and any backup calculation required under the documents.

- Verify the unpaid principal balance, accrued interest period, per diem amount, and all administrative fees.

- Check the yield maintenance benchmark, spread, remaining term, and discounting assumptions against the contract language.

- Confirm whether any defeasance, assumption, lockout, open-period, or default provisions change the payoff structure.

- Coordinate closing funds so the wire lands on the exact payoff date stated in the demand.

- Obtain a revised statement if the closing date changes, because per diem interest and the premium may both move.

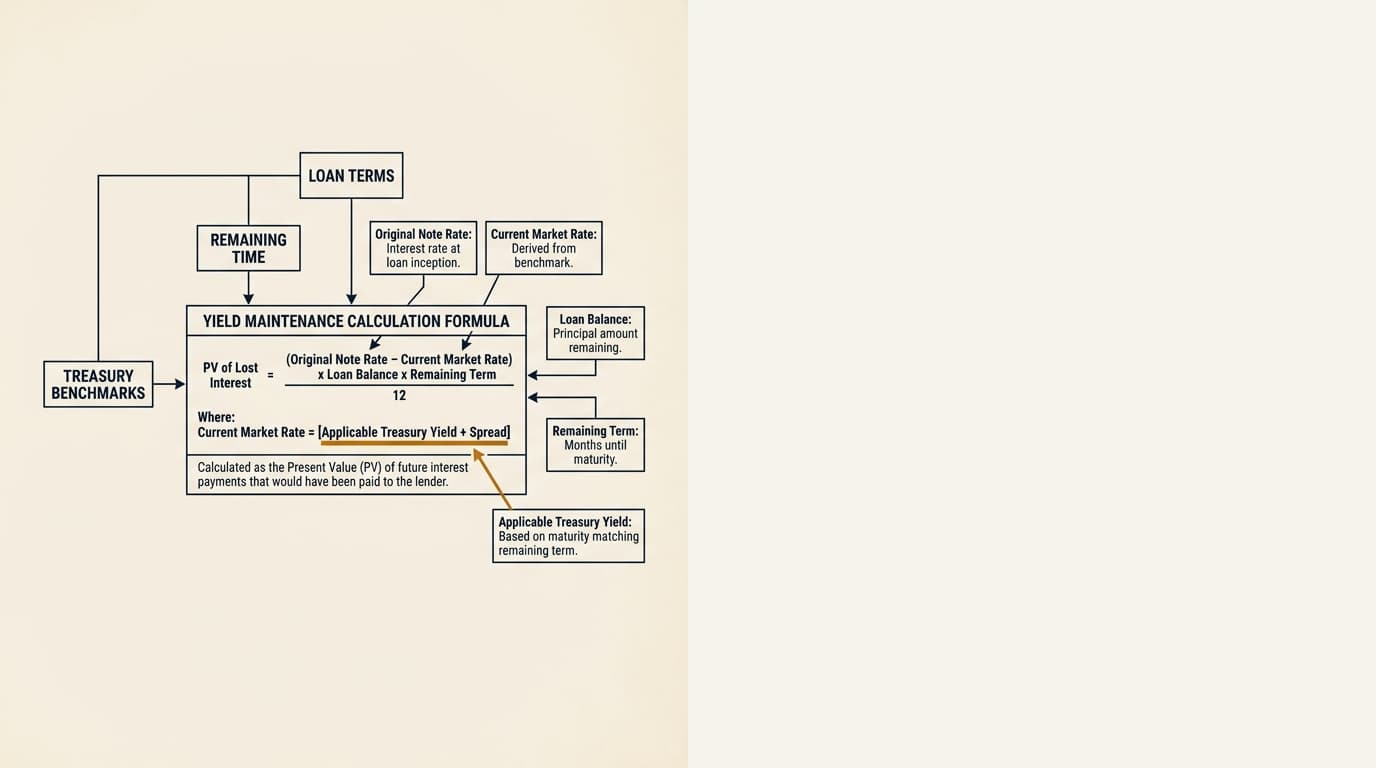

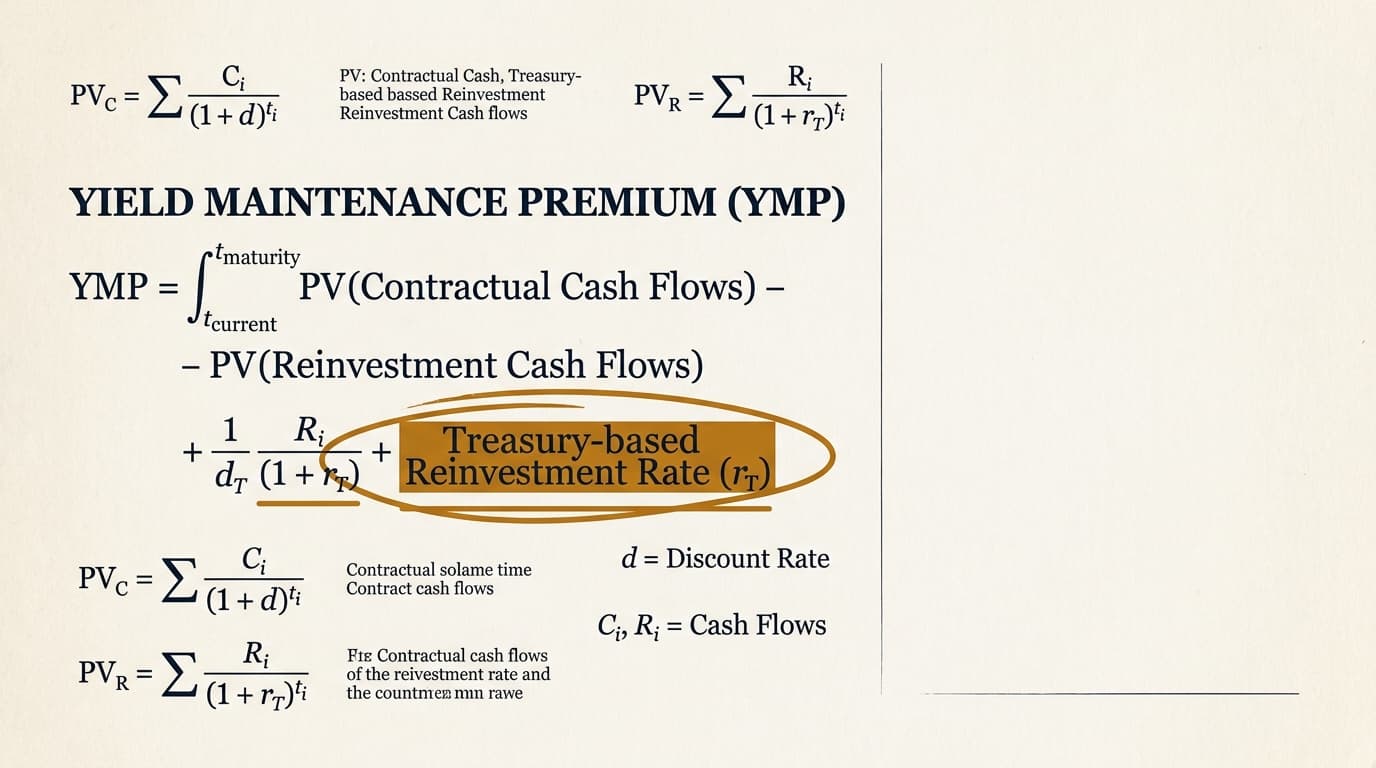

Readers who need the math itself can use the separate explainer on the yield maintenance formula. This page stays with the practical question: how that math shows up in a live statement and settlement.

What increases or reduces a yield maintenance prepayment penalty?

The biggest drivers are the interest-rate gap, the time left on the loan, and the benchmark method required by the contract. In plain English, the penalty gets bigger when the lender is losing a high coupon for a long remaining term and can reinvest only at a lower market rate.

The U.S. Department of the Treasury daily Treasury par yield curve rates change every day. Because many yield maintenance clauses point to Treasury securities or interpolated Treasury yields, the penalty can move meaningfully from one quote date to the next when rates move. The Federal Reserve H.15 selected interest rates release is also useful for validating the rate environment tied to a payoff quote.

Variables that usually increase cost

These conditions usually make the premium larger:

- Lower Treasury rates. A lower reinvestment rate increases the present value of the lender’s forgone interest stream.

- Longer remaining term. More months left until maturity means more scheduled interest to replace.

- Higher note coupon. The larger the gap between the loan rate and the benchmark, the larger the make-whole amount tends to be.

- Monthly payment structure with substantial remaining amortization tail. If many payments remain, the discounted lost-yield amount is usually larger.

- No open window. If the document stays premium-bearing until very close to maturity, there is less room for a cheaper exit.

Variables that usually reduce cost

These conditions usually make the premium smaller:

- Higher Treasury rates. If reinvestment rates rise closer to the note rate, the lost-yield amount narrows.

- Short time to maturity. Fewer remaining scheduled payments usually mean a smaller premium.

- An expired premium floor or a no-premium open period. Some loans become freely prepayable near maturity.

- An assumption rather than a payoff. If the buyer assumes the debt and the lender approves, the seller may avoid a prepayment event altogether, subject to fees and underwriting.

For rate-driven behavior in lower-rate cycles, the dedicated article on yield maintenance in a falling rate environment goes deeper on why the same loan can get materially more expensive to exit after a Treasury rally.

Decision framework: pay now or wait?

The right answer depends on whether the penalty savings from waiting are bigger than the cost of waiting. That sounds obvious, but borrowers regularly focus on the premium by itself and miss the transaction math around it. If you are comparing an immediate refinance with a delayed one, test three numbers together: the current premium, the expected premium on a later date, and the carry cost of waiting.

| Scenario | What usually matters most | Practical implication |

|---|---|---|

| Sale closing in 30 days | Firm contract date and buyer certainty | A smaller future premium may not matter if delaying puts the sale at risk. |

| Refinance with lower permanent rate | Rate savings versus premium | The refinance works only if present-value interest savings exceed the all-in payoff cost. |

| Loan near open period | Months until no-premium payoff | Waiting can make economic sense if carry costs are lower than the premium avoided. |

| Potential assumption by buyer | Lender approval and assumption fees | Assumption may preserve value if the existing loan terms are attractive enough to the buyer. |

This is the part people often get wrong. The question is not whether the yield maintenance prepayment penalty feels high. It usually does. The question is whether paying it now leads to a better net result than refinancing later, waiting for an open window, or taking another exit route. For a side-by-side comparison of structures, see yield maintenance vs step-down and yield maintenance vs defeasance.

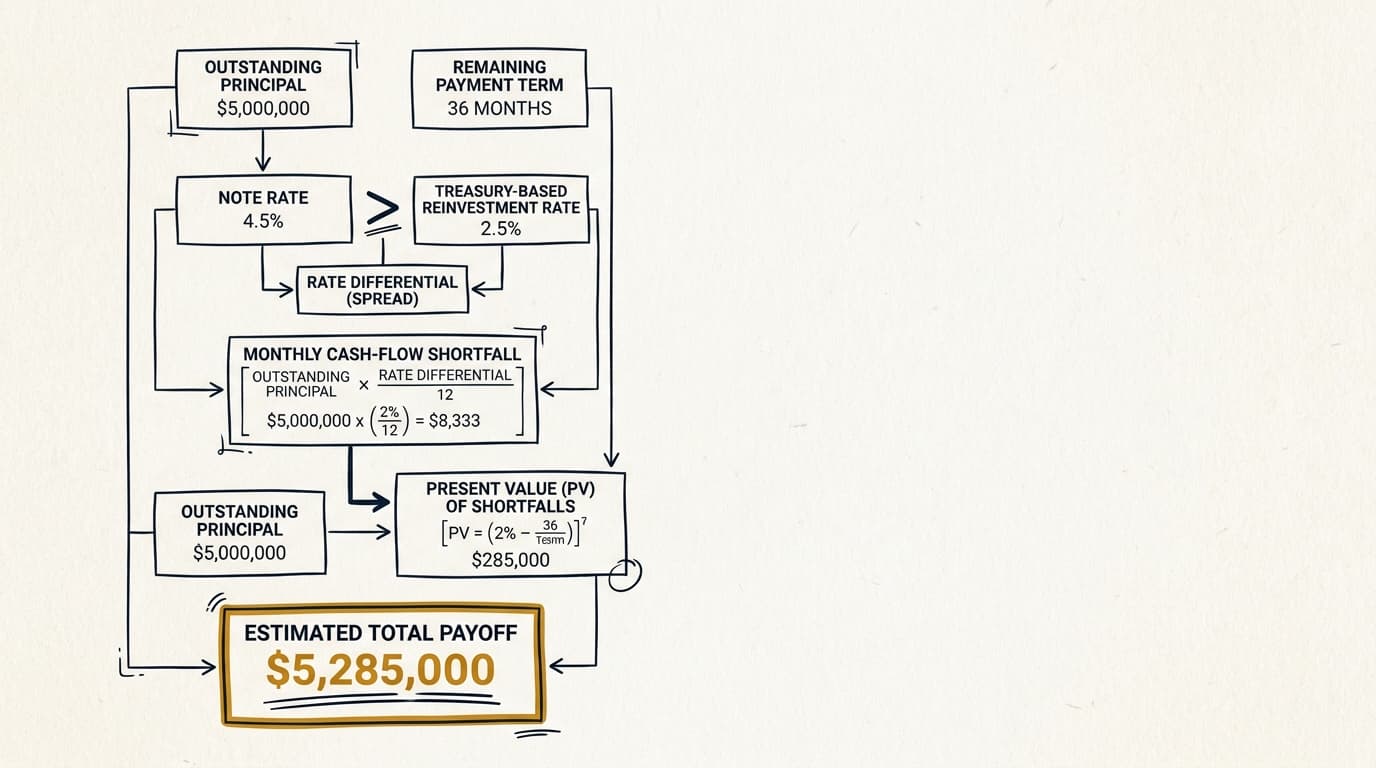

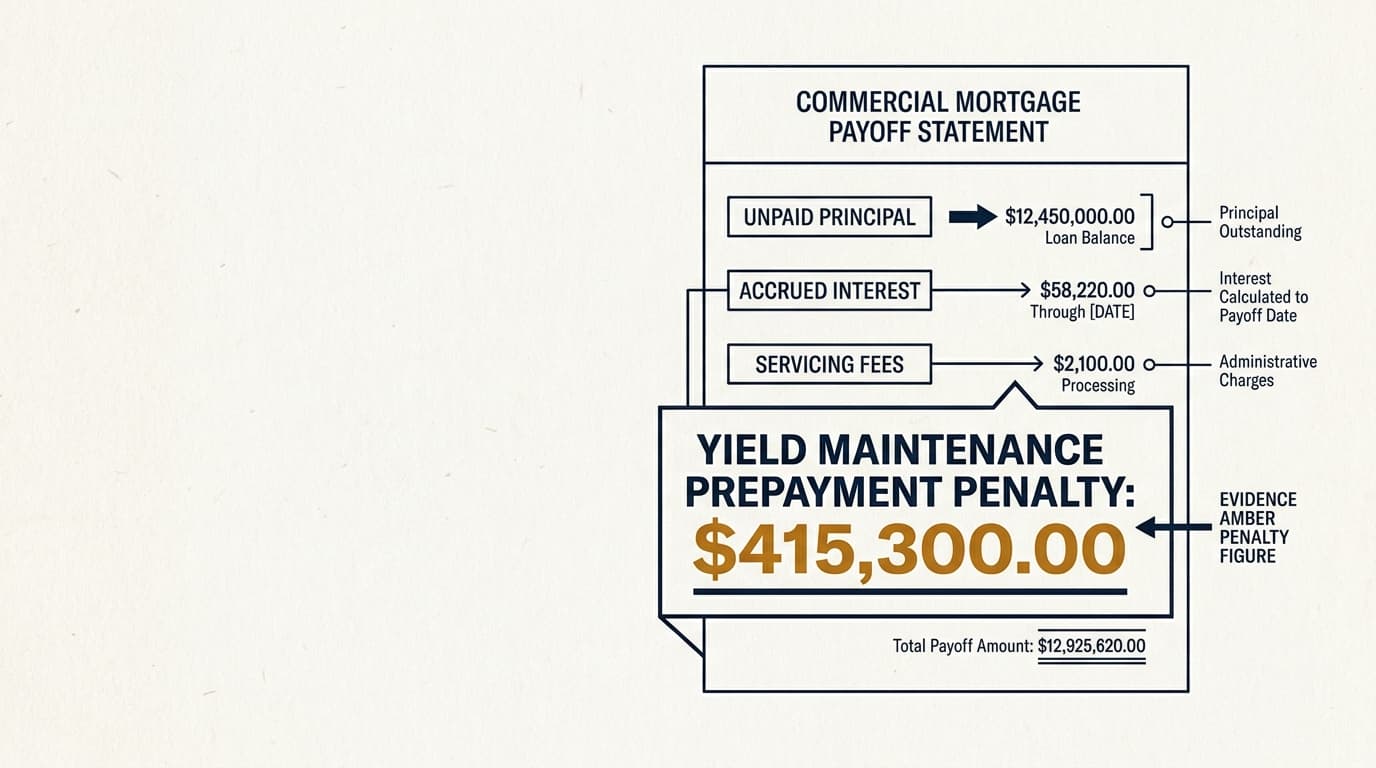

Real payoff example: how the penalty changes the wire amount

A payoff statement turns an abstract clause into a settlement number. Even a moderate premium can change sale proceeds, refinance proceeds, reserves, and lender-to-lender timing.

Consider a simplified office loan with these assumptions:

- Outstanding principal: $8,000,000

- Note rate: 6.20% fixed

- Remaining term: 48 months

- Accrued interest through payoff date: $41,333

- Servicing/payoff fee: $1,250

- Yield maintenance premium: $612,000

Under those facts, the wire amount is not $8 million. It is approximately $8,654,583 before any additional legal fees, escrow shortages, or date changes. If the closing slips five days and the per diem interest is about $1,378, the borrower adds another $6,890. That is not a rounding issue. A one-week delay can move the settlement by nearly $7,000 even before any rate-driven recalculation of the premium.

That is why payoff administration matters. In a refinance, the incoming lender may size proceeds around principal and ordinary closing costs, while the actual payoff demand includes a large premium that has to be covered with cash-in or a larger loan request. In a sale, the penalty comes straight out of the seller’s net proceeds.

Edge cases that change the payoff number

Several situations can change the payoff statement in ways borrowers do not expect. Usually the problem is not the math. It is the documents, the servicing process, or the transaction timeline.

Loans in default

A defaulted loan can carry both a prepayment premium and default interest, depending on governing law and document language. Courts in some jurisdictions take a hard look at whether a make-whole is enforceable after acceleration, while others enforce it if the documents are clear. There is no universal answer here. It is state-specific and document-specific.

Partial prepayments

Many commercial mortgages do not allow partial prepayments at all. If partial curtailments are allowed, the premium method may differ from a full payoff, and borrowers should not assume the same formula applies automatically.

Open-window miscalculations

Some loans become open only during a narrow period before maturity, and the operative date may be the lender’s receipt date rather than the borrower’s wire initiation date. Miss that by one business day and the premium can come back.

Servicer instructions versus document language

The statement should apply the contract, not rewrite it. If a payoff quote uses a benchmark date, spread, or remittance convention that does not match the note, counsel or the borrower’s analyst should ask for backup. Servicing templates often compress assumptions that need to be checked against the actual rider language.

How to review a payoff statement before wiring funds

A payoff statement is a transaction document, not just an accounting printout. Borrowers, counsel, and mortgage bankers should reconcile it to the note, the closing calendar, and the sources-and-uses schedule before funds move.

- Match the payoff date to the closing date. If the wire date changes, get a revised statement.

- Confirm per diem interest. Check the daily accrual against the note rate and outstanding principal.

- Verify the benchmark source and date. Treasury-based clauses often depend on a specific observation date or interpolation method.

- Reconcile fees. Statement fees, legal fees, assumption review fees, and release fees should have a documentary basis.

- Check for escrow shortages or reserve balances. Taxes, insurance, and replacement reserves can affect net cash at closing even if they are not part of the premium itself.

- Request backup for the premium. A one-page summary is rarely enough on a large institutional payoff.

Borrowers that handle payoffs regularly usually build a checklist because the cost of a date mistake can exceed the administrative fee many times over. That sounds mundane, but it matters. As CRE capital stacks have gotten more layered and servicing chains more fragmented, payoff verification has become an operational issue, not just a legal one.

Frequently Asked Questions

Is a yield maintenance prepayment penalty the same as the total payoff amount?

No. The penalty is only one line item in the total payoff. The full wire usually includes unpaid principal, accrued interest, the yield maintenance premium, statement or servicing fees, and sometimes default interest, legal fees, or protective advances.

Does a yield maintenance prepayment penalty always apply when a property is sold?

No. It usually applies only if the sale requires the existing loan to be paid off before the no-premium date. If the buyer assumes the loan and the lender approves the assumption, a sale may close without triggering a prepayment premium, although assumption fees and underwriting conditions may still apply.

Why did the payoff amount change from one week to the next?

The payoff amount can change because accrued interest increases each day and the yield maintenance premium may be recalculated using a different Treasury benchmark or remittance date. Even if principal is unchanged, market-rate movement and closing delays can change the final demand.

Are yield maintenance penalties different in New York, Texas, or California?

Yes. Enforcement questions can vary by state law, especially when a loan is in default or has been accelerated. The calculation method comes from the contract, but courts do not always treat make-whole provisions the same way across jurisdictions. For state-specific enforceability questions, counsel should review the governing law clause and current case law in the relevant state.

Can a borrower negotiate the payoff amount after the statement is issued?

Sometimes, but usually only at the margins. Portfolio lenders may have some discretion, especially if they want to keep the relationship or originate the refinance. Securitized or heavily serviced loans usually offer much less flexibility because the servicer has to apply the documents and servicing standard rather than waive economics informally.