Yield Maintenance in a Falling Rate Environment

Yield maintenance usually gets more expensive when Treasury rates fall: the lender has to reinvest at a lower rate, so the present value of the interest it loses goes up. This article breaks down the rate mechanics, walks through a simple model, and shows what borrowers should test before they refinance.

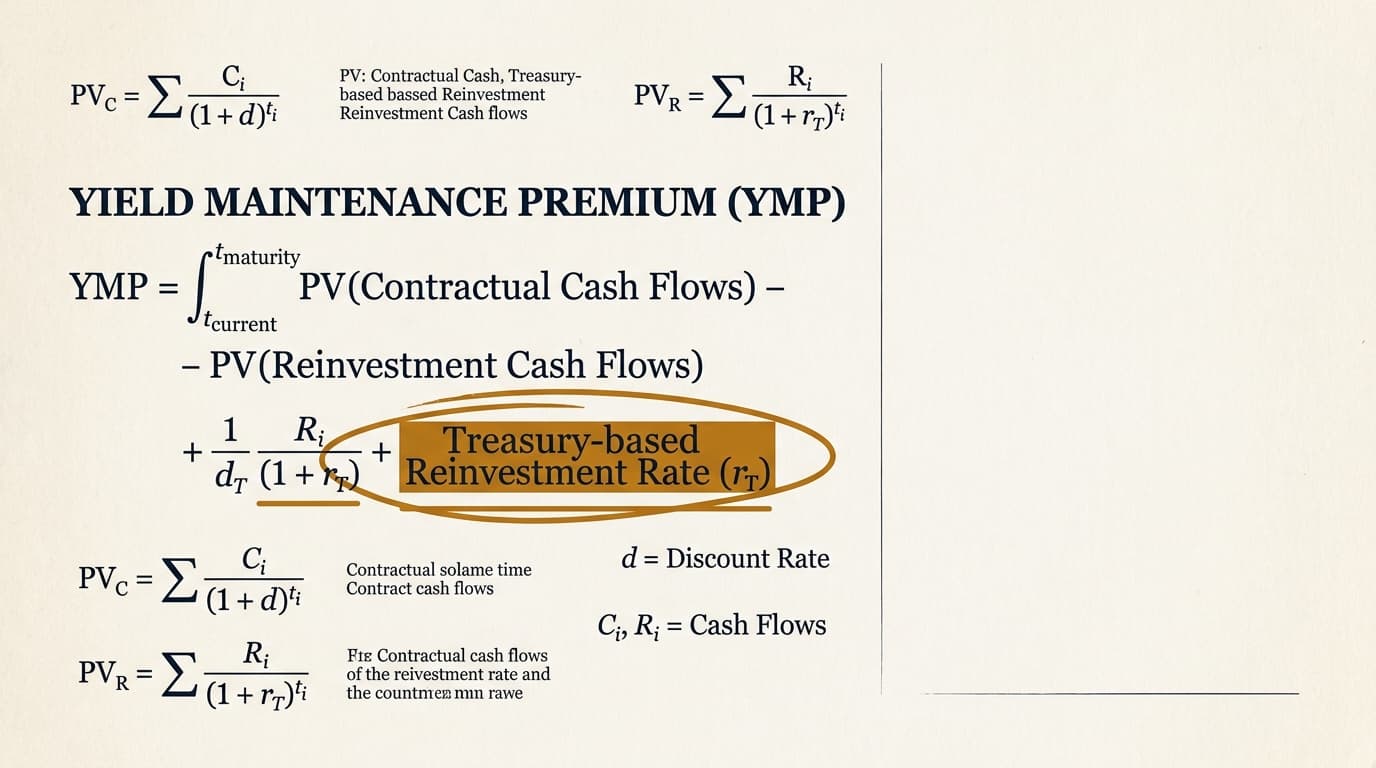

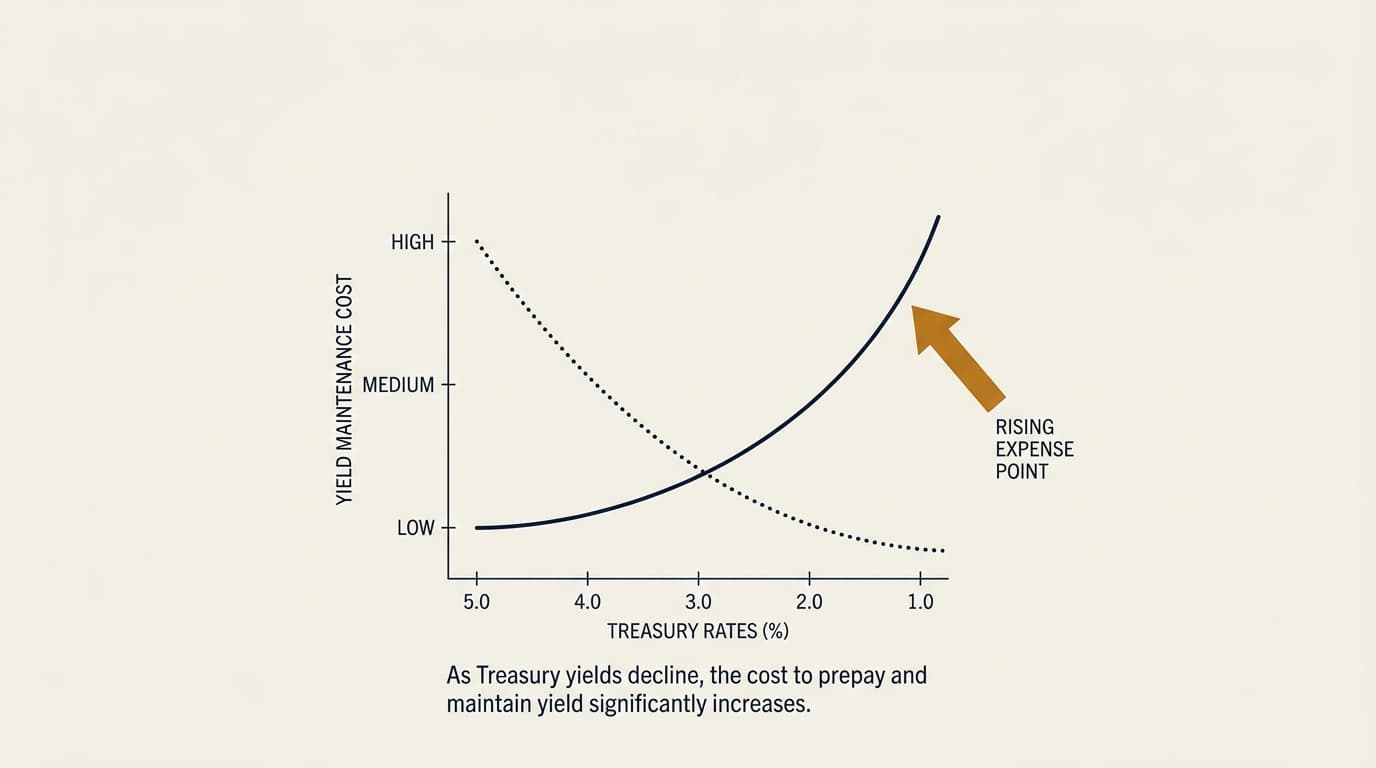

Yield maintenance usually gets more expensive when Treasury yields fall. The reason is mechanical: many loan documents calculate the prepayment charge by discounting the lender’s remaining scheduled interest at a Treasury-based reinvestment rate, and when that discount rate drops, the present value of the lender’s lost income goes up.

For borrowers looking at a refinance in 2026, that sensitivity matters just as much as the rate on the new loan. The question is not only whether the replacement coupon looks better. It is whether the payoff still makes sense once you account for how lower Treasury yields can inflate the exit cost. This article breaks down why that happens, how to model the downside before ordering a payoff, and which document terms can throw off an estimate by a meaningful amount.

Key Takeaways

- Yield maintenance usually rises when Treasury rates fall because the lender is assumed to reinvest prepaid principal at a lower rate, which increases the value of foregone interest.

- Small moves in Treasury yields can change payoff cost a lot, especially when several years remain before open prepayment or maturity.

- A reliable estimate requires the actual note language, including the spread, floor, remaining term, payment schedule, and the Treasury definition used in the clause.

- Borrowers should model at least three rate cases — current Treasury, down 50 basis points, and down 100 basis points — before deciding whether a refinance still clears return hurdles.

- Quoted payoff statements can differ from borrower estimates because of servicing fees, interest through payoff date, and document-specific assumptions.

Yield maintenance in a falling rate environment: the direct answer

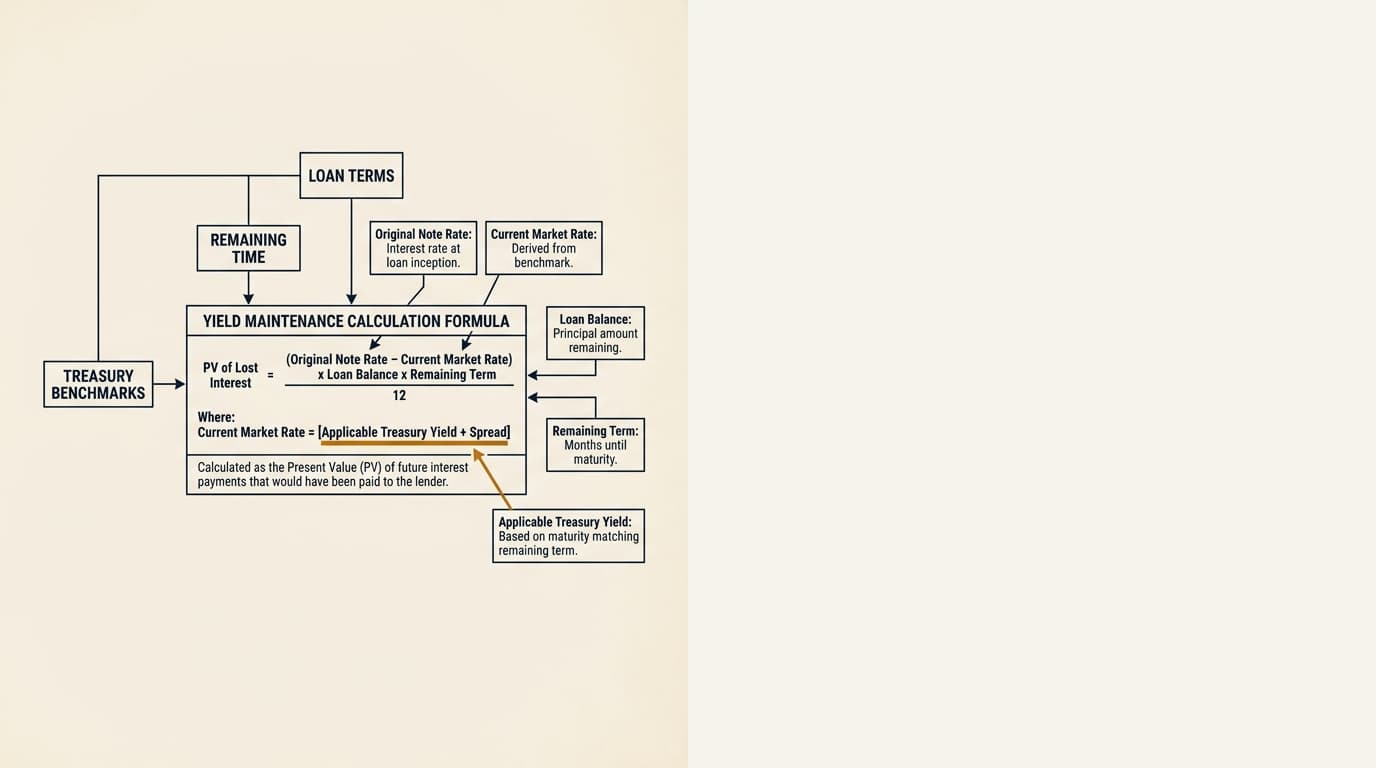

Yield maintenance usually increases in a falling rate environment because the lender’s comparison rate falls. In most structures, the lender gets paid for the difference between the note rate cash flow and what it could earn by reinvesting at a Treasury-based rate, with a stated spread added or subtracted.

According to the Federal Reserve Bank of New York Treasury market rate publications, Treasury yields move daily and can shift meaningfully during a refinance process. When those benchmark yields decline, the discounted value of the lender’s lost interest stream rises, and the prepayment charge rises with it. For a broader overview of commercial real estate yield maintenance, the main point is simple: falling benchmark rates often make an early exit more expensive, even when the new loan rate looks appealing.

Why lower Treasury rates increase yield maintenance cost

Lower Treasury rates increase yield maintenance cost because the clause is built to preserve the lender’s expected yield after prepayment. If the lender is assumed to reinvest at a lower rate, it earns less on replacement assets, so the borrower has to cover more of that gap.

According to the Board of Governors of the Federal Reserve System H.15 Selected Interest Rates release, U.S. Treasury yields are a standard market benchmark for fixed-income discounting. Many commercial mortgage notes tie the prepayment calculation to a Treasury with a maturity that roughly matches the remaining loan term, sometimes with a spread adjustment and sometimes with a floor. The mechanics vary by document. That is why the governing language in the yield maintenance loan documents matters more than any shortcut.

A simple way to think about it:

- The loan note rate sets the interest cash flow the lender expected to receive.

- The Treasury-based rate sets what the lender is assumed to earn after prepayment.

- The wider that gap, and the longer it lasts, the higher the penalty.

According to the U.S. Department of the Treasury daily Treasury yield curve resource, intermediate and longer-dated Treasuries can move sharply during easing cycles. In practice, a 75 to 150 basis point drop in the relevant Treasury benchmark can increase the payoff charge enough to wipe out much of the expected refinance benefit.

Duration makes the sensitivity worse

Rate sensitivity gets worse when the loan has more protected term left. More remaining monthly payments means more future interest cash flow has to be valued against that lower reinvestment rate.

That is why two loans with the same balance and coupon can produce very different results. A borrower 18 months from open prepayment may see a manageable charge. A borrower with six years left may face a much larger cost from the same Treasury move. If you want the underlying math, the separate page on yield maintenance formula walks through the calculation structure in more detail.

A simplified example of rate sensitivity

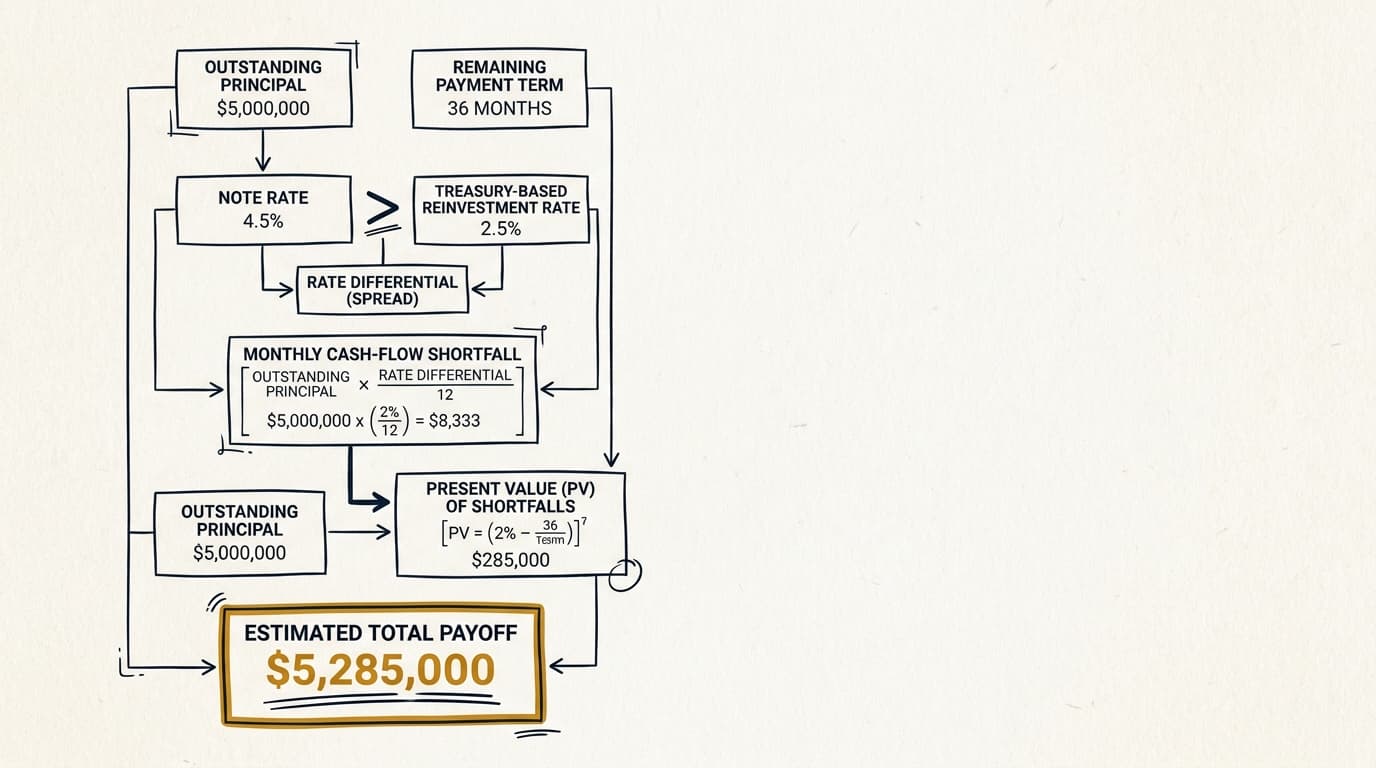

A modest Treasury decline can add hundreds of thousands of dollars to a payoff estimate on a mid-size commercial loan. The exact amount depends on amortization, remaining term, spread, and whether the note includes a minimum prepayment charge.

Assume a borrower has a $10 million fixed-rate loan at 6.00%, with five years left before maturity and monthly debt service. For this illustration, the note uses a Treasury-based comparison rate and no unusual servicing adjustments.

| Scenario | Relevant Treasury rate | Approximate rate gap vs. note | Illustrative yield maintenance result |

|---|---|---|---|

| A | 4.50% | 1.50% | $620,000 |

| B | 4.00% | 2.00% | $790,000 |

| C | 3.50% | 2.50% | $975,000 |

These figures are illustrative, not universal payoff amounts. The practical point is that a 100 basis point drop in the benchmark can produce a larger-than-expected increase in cost because every remaining interest shortfall is discounted at a lower rate.

Borrowers often focus on the new loan coupon and miss this convexity. A refinance that looks accretive at application can stop making economic sense by closing if Treasury yields fall during the quote period. For a transaction-level walk-through, see this yield maintenance calculation example.

How borrowers should model yield maintenance before refinancing

A workable borrower model should test payoff cost under multiple Treasury scenarios before anyone treats a refinance decision as final. The goal is not to match the servicer’s number down to the dollar. The goal is to understand how exposed net proceeds and debt-service savings are to benchmark rate moves.

- Pull the note, allonge, and servicing correspondence to confirm the exact prepayment language.

- Identify the current outstanding principal, maturity date, payment frequency, and any open-prepayment date.

- Determine which Treasury benchmark the clause uses and whether the document applies a spread, floor, or minimum penalty.

- Project the remaining scheduled payments through the protected period or maturity, as the document requires.

- Run at least three benchmark cases: current Treasury, 50 basis points lower, and 100 basis points lower.

- Add non-formula items such as accrued interest, servicing fees, legal charges, or statement fees if the servicer typically includes them.

- Compare the all-in payoff against refinance proceeds, replacement loan costs, and expected hold-period savings.

According to the Consumer Financial Protection Bureau explanation of prepayment penalties, the contract controls how a prepayment charge is assessed. In commercial loans, that means a spreadsheet built on generic assumptions can be directionally useful and still wrong on the final number if it misses a document-specific Treasury definition or floor. Borrowers dealing with cmbs yield maintenance should also account for servicer procedures and timing requirements, which can affect when a quote is valid and what extra line items appear.

The minimum three-scenario test

The minimum practical screen is a base case plus two downside Treasury cases. This shows whether the transaction still works if rates move in the borrower’s favor on the refinance coupon but against the payoff formula.

For example, if a refinance saves 85 basis points on loan coupon but a 75 basis point Treasury decline adds $300,000 to the prepayment charge, the breakeven hold period can get much longer. At that point, the real question is not whether the new rate is lower. It is whether the property will be held long enough to earn back the added exit cost. That analysis often overlaps with the decision path in yield maintenance refinance or sale.

What to review in loan documents before relying on a model

Document wording determines the benchmark, the spread, and the timing conventions used in the payoff. Small drafting differences can change the result enough to make an otherwise careful estimate unreliable.

- Treasury definition: Some notes specify a constant maturity Treasury. Others use a Treasury security with comparable remaining term.

- Spread adjustment: The comparison rate may be Treasury plus a stated number of basis points.

- Floor: Some clauses keep the comparison rate from falling below a stated minimum.

- Protected period: The charge may run to maturity, the first open-prepayment date, or another specified date.

- Minimum charge: A note may require at least 1% of principal or a fixed minimum even when the formula produces less.

- Notice and quote timing: The benchmark may be set on a specific determination date, not the closing date.

Borrowers comparing structures should not assume every loan behaves this way. Some executions use a declining schedule instead, which is better addressed in yield maintenance vs step-down. Others, especially securitized loans, may push the borrower toward a different exit framework, covered in yield maintenance vs defeasance and cmbs yield maintenance vs defeasance.

Decision framework: refinance, sell, wait, or consider another exit

The right choice depends on holding period, the likely path of Treasury yields, and whether the loan is close to a lower-cost prepayment window. A lower replacement coupon does not automatically justify an early payoff when the prepayment charge grows faster than the debt-service savings.

| Scenario | Usually favors | Why |

|---|---|---|

| Hold 7+ years, strong coupon reduction, moderate penalty | Refinance now | A longer hold period gives the borrower more time to recover the upfront payoff cost. |

| Open prepayment date within 6-12 months | Wait | A near-term drop in the penalty may be worth more than the immediate rate savings. |

| Pending sale with assumable debt option | Assumption analysis | Buyer assumption may preserve value better than paying the charge. |

| CMBS structure with complex servicing and securities replacement economics | Alternative exit review | Transaction costs and timing can differ from a balance-sheet loan. |

This is where borrower-side analysis matters more than generic explanations. If the property is likely to be sold in 24 months, paying a seven-figure charge to lower debt service today may not pencil. If the asset will be held for another decade, that same charge may be recoverable. Borrowers with a possible buyer assumption should review yield maintenance assumption sale, and those negotiating new originations should study yield maintenance borrower negotiation before closing, not after rates move.

Edge cases that change the outcome

Several common exceptions can change the economic answer even when the rate logic is straightforward. Borrowers often miss these in back-of-the-envelope models.

Loans near open prepayment

A loan close to its open window can behave very differently from a loan with years of protection left. In that situation, the real question is how many scheduled payments are still subject to the clause, not just whether Treasury yields are low.

That timing issue is covered in more detail in yield maintenance before maturity. A borrower 90 days from open prepay may get a better result by waiting, even if replacement rates move up a bit in the meantime.

Property type and exit constraints

Property operations can affect whether a borrower has the option to wait. Office and retail assets dealing with lease rollover or sale timing pressure may not have the same flexibility as stabilized multifamily assets.

Those differences show up in transaction planning, not in the formula itself. See yield maintenance office retail and yield maintenance multifamily loans for asset-specific considerations, and yield maintenance accounting tax for finance-team treatment after payoff.

Frequently Asked Questions

Why does yield maintenance go up when interest rates go down?

Yield maintenance usually rises when interest rates fall because the lender’s reinvestment benchmark, often tied to a Treasury yield, also falls. That lower reinvestment rate increases the present value of the interest income the lender loses when the borrower prepays early.

How much can a Treasury move change a yield maintenance payoff?

The change can be significant. On a multi-million-dollar fixed-rate loan with several years remaining, a 50 to 100 basis point drop in the relevant Treasury can add hundreds of thousands of dollars to the payoff estimate. The actual impact depends on term remaining, note rate, amortization, spread, floor, and quote date.

Can a borrower estimate yield maintenance without an official payoff statement?

Yes, but it is still only an estimate. A borrower can model the likely charge using the note language, balance, payment schedule, and current Treasury benchmark, then test lower-rate scenarios. The final payoff statement may still differ because of accrued interest, servicing fees, legal charges, and document-specific conventions.

Does yield maintenance behave the same way in every state or market?

No. The core math may be similar, but enforcement, servicing practice, and transaction timing can vary by loan structure, jurisdiction, and lender type. A life company balance-sheet loan in Texas may have different quote procedures and document language than a securitized loan secured by a property in New York or California, so local counsel and the actual note terms still matter.

What should borrowers review first before refinancing a loan with yield maintenance?

Start with the promissory note and any rider that defines prepayment, the Treasury benchmark, spread, floor, protected period, and notice requirements. Then model the payoff under current and lower Treasury scenarios before comparing refinance savings. If the clause is ambiguous, confirm the servicer’s interpretation before assuming the transaction works.