Yield Maintenance Office Retail: Sale Timing Guide

Office and retail owners usually run into yield maintenance at exactly the wrong time: during tenant rollover, a refinancing gap, or a sale that depends on a clean payoff. This is not just a loan-calculation issue; it can change hold strategy, leasing decisions, and whether a property can sell at all.

Most office and retail owners don’t think about yield maintenance office retail until a lease problem runs straight into a loan deadline. A big rollover, dark space, tenant improvement budget, or delayed sale can turn what looked like a routine prepayment clause into the main constraint on the deal.

This article breaks down how yield maintenance affects office and retail exits differently in 2026, with practical ways to think about sale timing, refinance decisions, and loan assumption. The focus is property-level planning, not generic loan theory.

Key Takeaways

- Yield maintenance can materially change sale proceeds when office or retail assets need to trade before loan maturity, especially when rates have moved down.

- Office properties usually run into trouble at lease rollover because downtime, concession packages, and valuation resets can force an early capital event before the open prepay window.

- Retail properties have a different timing problem: anchor turnover, co-tenancy exposure, and lender scrutiny of the rent roll can shrink the buyer pool and make loan assumption more important.

- The right decision is usually property-specific. Compare sale, refinance, hold, and assumption paths using the actual loan documents, servicer requirements, and current Treasury inputs.

What yield maintenance office retail means in practice

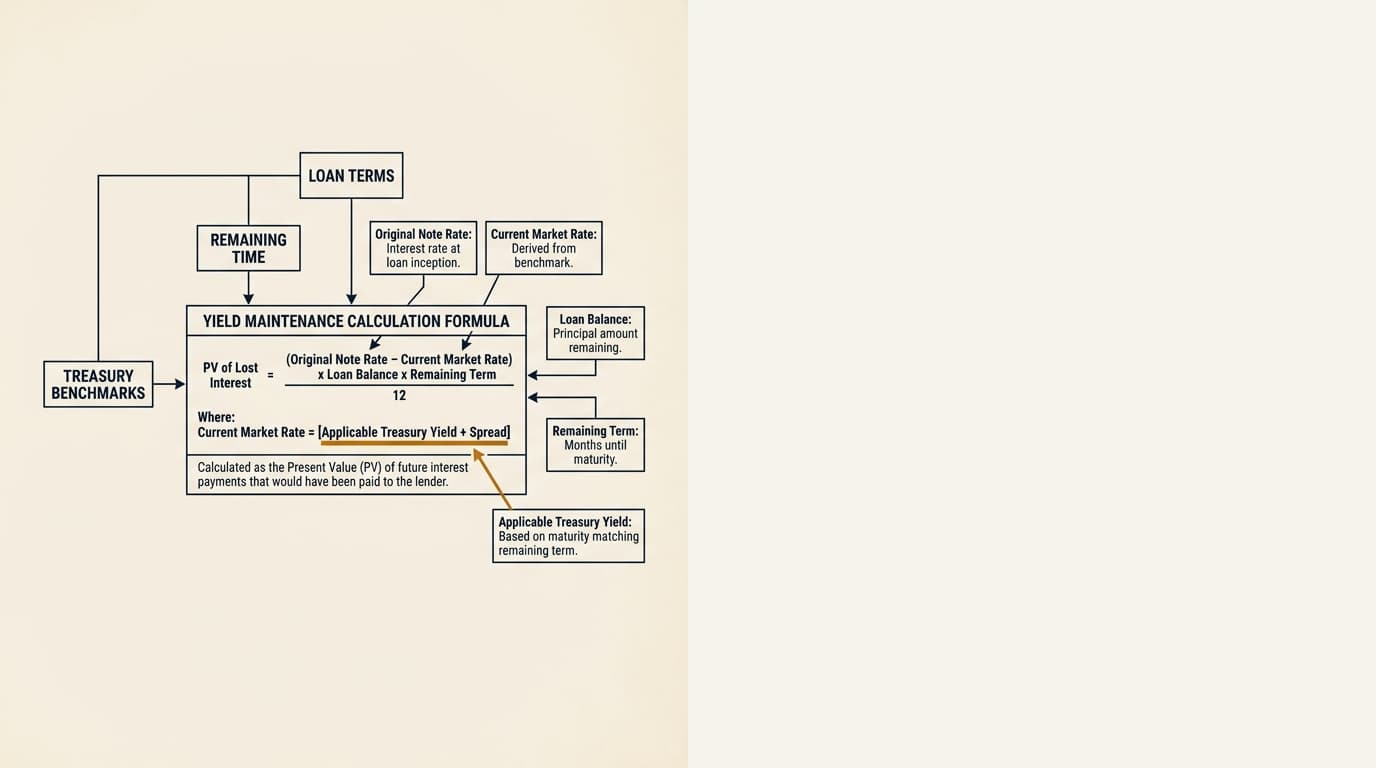

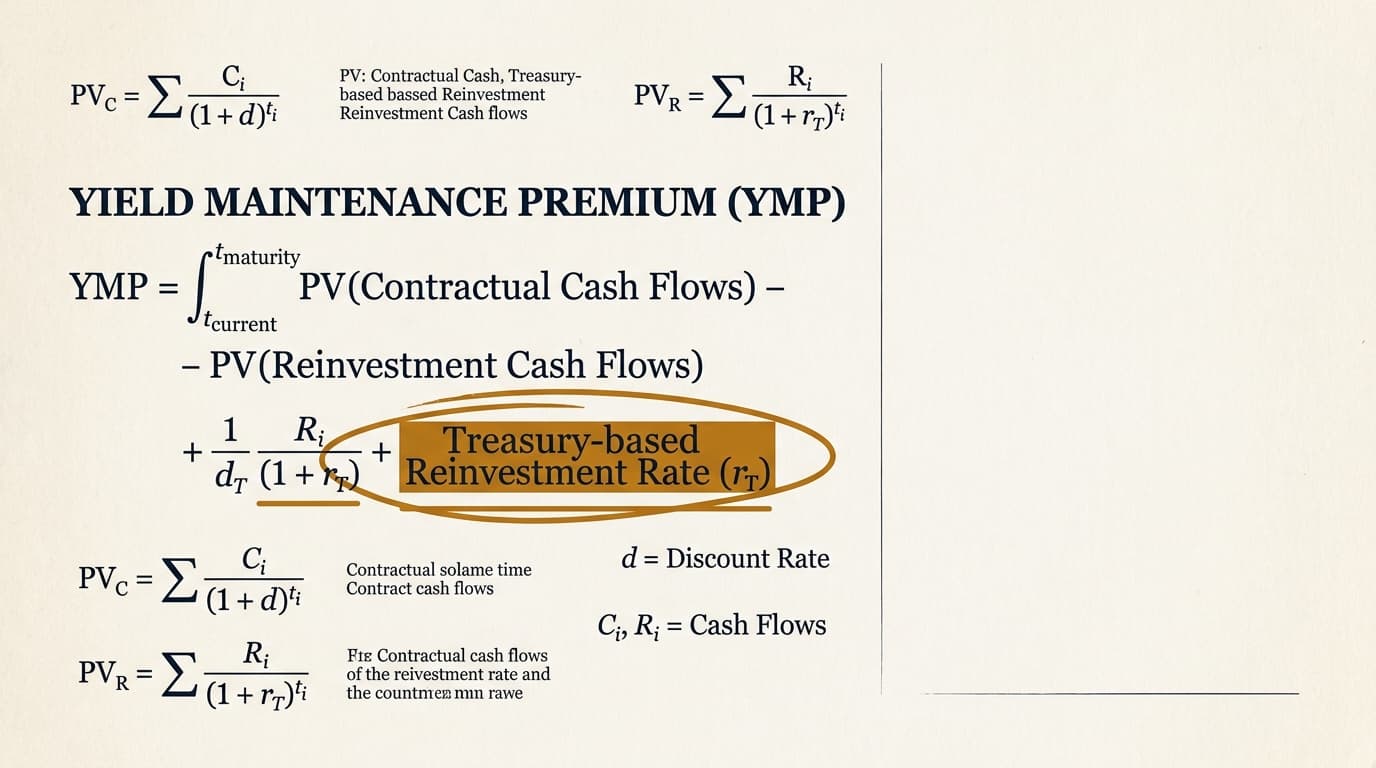

Yield maintenance is a prepayment formula that protects a lender’s expected yield when a fixed-rate loan gets paid off before maturity. For office and retail owners, it becomes an exit-planning problem when the property is already under leasing or valuation pressure.

According to the Consumer Financial Protection Bureau explanation of prepayment penalties, a prepayment charge compensates a lender for early payoff, although commercial loan terms are governed by negotiated documents rather than consumer rules. In commercial real estate, the exact method is set by the note, loan agreement, or securitized servicing standard. That’s why reviewing yield maintenance loan documents should come first, before any sale or refinance process starts.

For a direct explanation of the broader concept, see Graphline's pillar on commercial real estate yield maintenance. In office and retail, the real issue usually isn’t the formula itself. It’s whether the penalty hits at the exact moment net operating income, cap rate expectations, and leasing costs are already moving against the owner.

Why office and retail face different yield maintenance pressure points

Office and retail both use long-term fixed-rate debt, but the cash-flow stress shows up on different timelines. That matters because yield maintenance cost depends heavily on when the owner needs to exit, not just whether the owner wants to.

According to CBRE U.S. Office Figures for Q4 2025, office availability remained elevated nationally, with leasing conditions still uneven by market and building quality. According to JLL U.S. retail market research, retail vacancy has generally remained tighter than office, but performance still varies sharply by center type, tenant mix, and anchor strength. Those operating differences lead to different financing triggers.

| Property type | Common trigger | How yield maintenance becomes a problem | Typical workaround to test |

|---|---|---|---|

| Office | Large rollover or move-out | Value drops before maturity, but owner needs capital or sale proceeds immediately | Short hold, extension, recapitalization, or discounted sale after penalty analysis |

| Retail | Anchor risk or co-tenancy exposure | Buyer underwriting weakens while penalty still blocks a clean exit | Loan assumption, delayed sale, partial leasing cure, or refinance comparison |

Put simply, office owners usually get pushed into a decision by vacancy and leasing capital needs. Retail owners usually get pushed there by tenant-credit events and buyer caution around lease durability.

Office yield maintenance during tenant rollover and valuation pressure

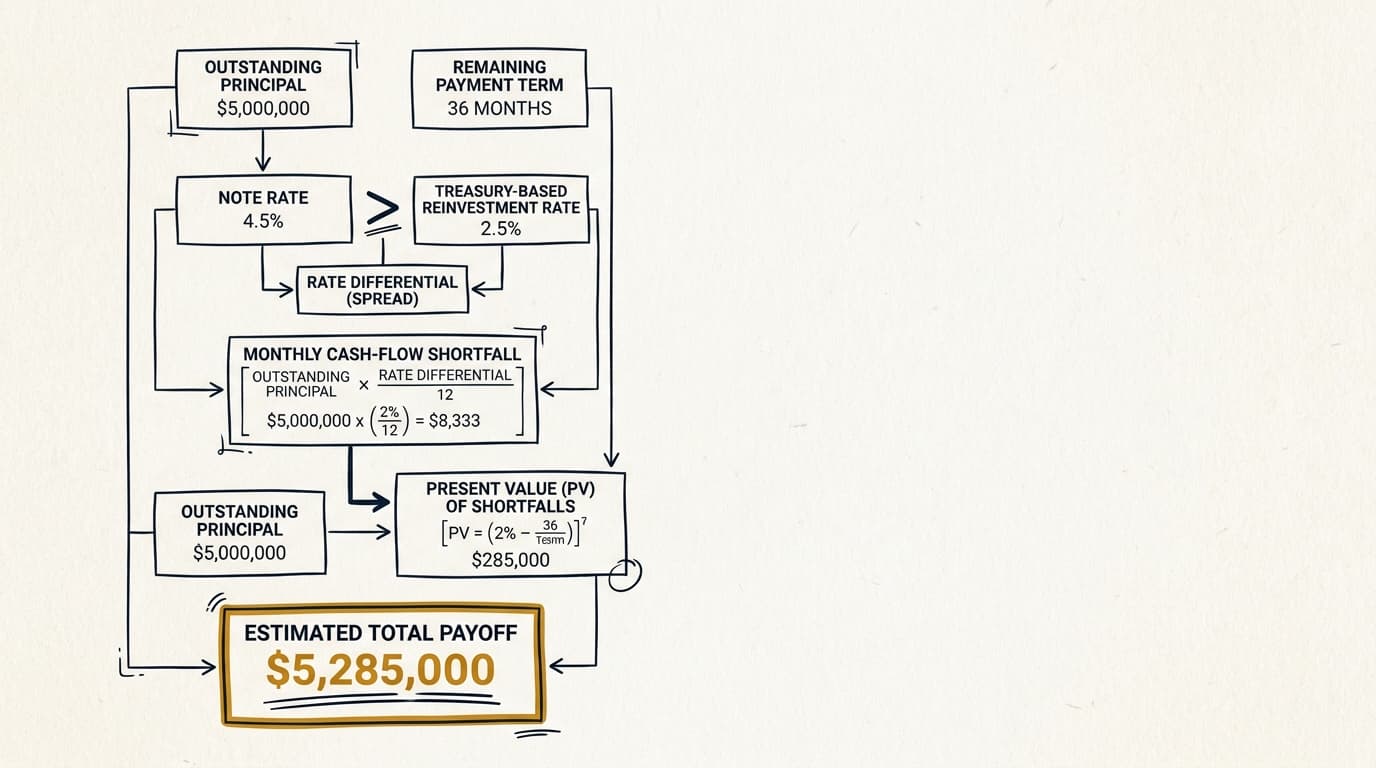

Office yield maintenance risk is highest when lease expiration arrives before the loan’s open prepayment date. In that setup, an owner can face lower income, higher tenant improvement costs, and a payoff penalty all at once.

According to Federal Reserve open market operations resources and U.S. Department of the Treasury interest rate statistics, Treasury yields move materially over a loan’s life, which affects how expensive yield maintenance may be when a rollover forces action. If prevailing Treasury rates are below the contract rate benchmarked in the loan, the penalty can be substantial. The math itself is covered separately in the yield maintenance formula guide and the detailed yield maintenance calculation example.

Office example: sale under leasing pressure

A realistic office scenario looks like this: a suburban building with 35% tenant rollover in 12 months, a loan maturing in four years, and a prepayment structure that stays closed for another 24 months. If the departing tenant occupied the top floor and paid above current market rent, the owner’s decision is not just whether to sell. The owner has to compare three numbers at the same time: expected sale price today, leasing capital needed to stabilize, and the yield maintenance payoff amount.

In practice, the penalty can wipe out the benefit of selling before the market fully reprices the vacancy. It can also block a refinance if debt service coverage fails under stressed underwriting. According to the Office of the Comptroller of the Currency's Commercial Real Estate Lending handbook, lenders evaluate repayment capacity, leasing risk, and collateral protection together rather than as separate issues. That’s why yield maintenance should be modeled alongside projected downtime and concession cost, not tacked on after a term sheet shows up.

Retail yield maintenance under anchor risk and co-tenancy clauses

Retail yield maintenance gets most disruptive when a tenancy event changes buyer or lender perception faster than the loan’s prepayment window changes. A dark anchor, expiring grocer, or weak junior-anchor sales report can hit value immediately even if the mortgage is still closed to an economical payoff.

According to ICSC retail research, traffic, tenant mix, and center format drive very different outcomes across retail assets. In neighborhood and power centers, one lease event can change co-tenancy rights, percentage-rent expectations, and renewal assumptions for smaller tenants. That makes timing unusually sensitive. A retail asset may still produce current cash flow while the market applies a much steeper cap rate because future rollover now looks shaky.

Why retail sale processes get stuck

Retail sale friction usually shows up when a buyer discounts the center for tenant rollover, but the seller still has to satisfy a high yield maintenance amount. The result is a bid-ask gap caused partly by operations and partly by the debt structure.

That gap gets wider when the buyer cannot assume the existing loan. Some fixed-rate retail loans permit assumption subject to lender approval, fees, and buyer underwriting. Others, particularly securitized structures, involve more rigid servicing procedures, which is why owners should compare yield maintenance vs defeasance and review transaction-specific rules for cmbs yield maintenance where applicable. If assumption is available, Graphline's guide to yield maintenance assumption sale explains when it can preserve value by avoiding immediate prepayment.

How to evaluate a sale, refinance, hold, or assumption

The best choice is the one that leaves the highest net value after penalty, leasing costs, and timing risk are all counted. Treating yield maintenance as a standalone fee line is a mistake. It changes which exit strategies are actually available in economic terms.

- Pull the note, loan agreement, and any servicing correspondence to confirm lockout dates, open prepayment windows, and the exact payoff method.

- Request a current payoff quote and ask which Treasury benchmark date and spread assumptions are being used.

- Model sale proceeds net of yield maintenance, transfer costs, leasing commissions, tenant improvements, and expected closing delay.

- Model a refinance using current debt-service coverage, debt yield, and valuation assumptions based on in-place and forward rent rolls.

- Test whether loan assumption is permitted and whether the likely buyer pool can satisfy lender or servicer underwriting.

- Compare the economics of waiting for a lower-penalty period against the risk of further vacancy, rent loss, or anchor disruption.

Owners who need a broader decision tree can use the related analysis on yield maintenance refinance or sale, and those negotiating new debt should review yield maintenance borrower negotiation before the next closing, not after a problem surfaces.

A decision framework for office vs. retail exit planning

Office and retail owners should underwrite yield maintenance against the actual source of asset-level uncertainty. The practical question isn’t whether the penalty exists. It’s whether waiting improves value more than it increases leasing and market risk.

| Scenario | Office bias | Retail bias | What it means in practice |

|---|---|---|---|

| Large near-term rollover | Often sell or recap before vacancy is reflected in trailing NOI, if penalty is still survivable | Less common unless anchor or major junior anchor | Office values can reset quickly when downtime and TI packages are repriced |

| Strong in-place cash flow but weak future lease profile | Refinance may be difficult | Buyer underwriting may still work for necessity retail with strong sales | Retail can sometimes hold value longer if tenant sales and traffic remain stable |

| Assumable in-place fixed-rate debt | Useful, but buyer demand may be narrow | Often more valuable if current coupon is below market | Assumption can preserve deal economics where direct payoff destroys proceeds |

| Penalty burns off within 12-18 months | Short extension may make sense if leasing path is visible | Waiting may be preferable if anchor renewal probability is high | The hold decision depends on whether property risk is likely to improve before open prepay |

This is where a lot of generic yield-maintenance pages fall flat: the same penalty amount can be manageable for a retail center with durable daily-needs tenancy and completely unworkable for an office building facing one large move-out. Property type changes what the same loan term actually means.

Documents and data to review before you market the asset

A clean sale process starts with a clean payoff file. Missing loan details can waste weeks during bid rounds, especially when the real answer is that the penalty is higher than the broker’s first underwriting assumed.

- Current rent roll with expiration schedule and known tenant notice events

- Estoppel status for major leases and any co-tenancy or kick-out provisions

- Loan note, mortgage or deed of trust, and servicing commentary on prepayment

- Most recent payoff letter and quote validity period

- Treasury benchmark reference used by the lender or servicer, which may differ by document wording; see yield maintenance treasury rate

- Open prepayment date, defeasance trigger if applicable, and maturity date; see yield maintenance before maturity

- Any assumptions about release prices, partial prepayments, or buyer assumption rights

For a direct look at how the penalty shows up in a payoff, see Graphline's page on the yield maintenance prepayment penalty. In a lot of deals, that documentation is what determines whether a buyer sharpens pricing or comes back late in diligence with a retrade.

Frequently Asked Questions

How does yield maintenance affect an office building sale during a major lease rollover?

Yield maintenance can cut net sale proceeds at the same time the buyer discounts the building for upcoming vacancy, tenant improvement costs, and leasing commissions. In office, that combination hits hardest when one tenant represents a large share of rentable area and the loan stays closed to economical prepayment for another one to three years.

Is yield maintenance usually worse for office or retail properties?

The penalty formula itself is not inherently worse for one property type, but the business impact often is. Office owners are more likely to face abrupt value pressure from large rollover and downtime. Retail owners are more likely to face transaction friction from anchor changes, co-tenancy rights, and buyer concerns about lease durability.

Can a retail buyer assume the seller's loan and avoid yield maintenance?

Sometimes. Whether a retail buyer can assume the loan depends on the loan documents, lender or servicer approval rights, buyer credit, and any assumption fee or structural conditions. CMBS loans may involve stricter servicing steps, so the answer can vary a lot by loan type and document language.

Which markets make yield maintenance office retail planning more sensitive?

Markets with high office availability, volatile cap rates, or a sharp split between Class A and commodity space tend to make office payoff timing more sensitive. For retail, markets with heavy anchor competition, changing consumer traffic patterns, or local tenant concentration can widen the gap between current income and buyer underwriting. Local leasing conditions matter as much as the loan term.

What should owners review first before listing an office or retail property with yield maintenance?

Start with the note, loan agreement, and latest payoff quote. Confirm the lockout period, open prepayment date, benchmark Treasury reference, assumption rights, and any servicing requirements. Then compare net sale proceeds against a hold or refinance case using updated rent-roll assumptions rather than trailing numbers alone.