Yield Maintenance Calculation Example for CRE Payoffs

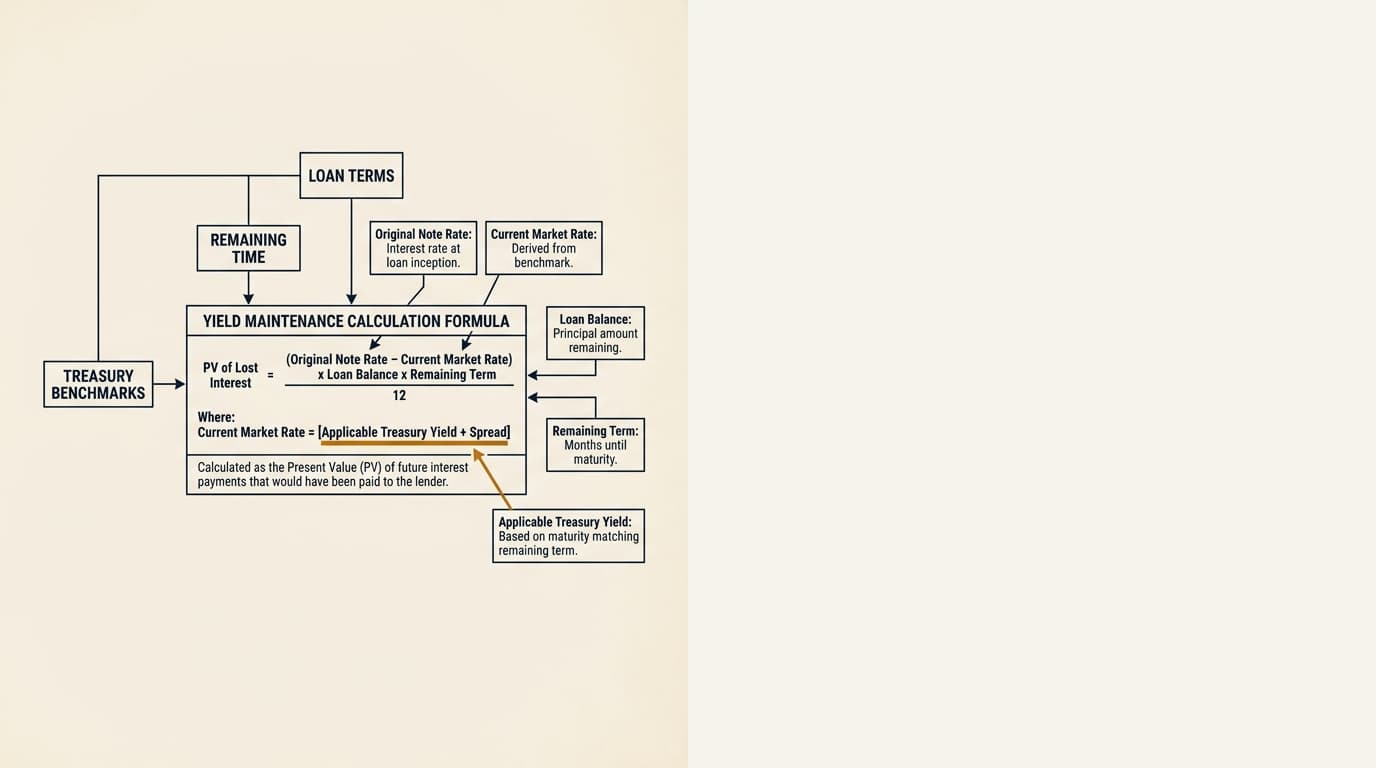

A yield maintenance example uses four inputs: outstanding principal, note rate, the Treasury-based reinvestment rate, and the remaining payment term. It walks through the math step by step, including the monthly cash-flow shortfall, the present value calculation, and the estimated total payoff.

$8.42 million is the estimated payoff on this sample loan, even though the unpaid principal balance is $7.80 million. The gap is the present value of the lender’s lost spread after prepayment, based on a Treasury reinvestment rate and the 60 months left on the loan.

Below is a worked example for a commercial mortgage with yield maintenance. It shows the inputs, the intermediate math, and the line items that often show up in real payoff letters in 2026.

Key Takeaways

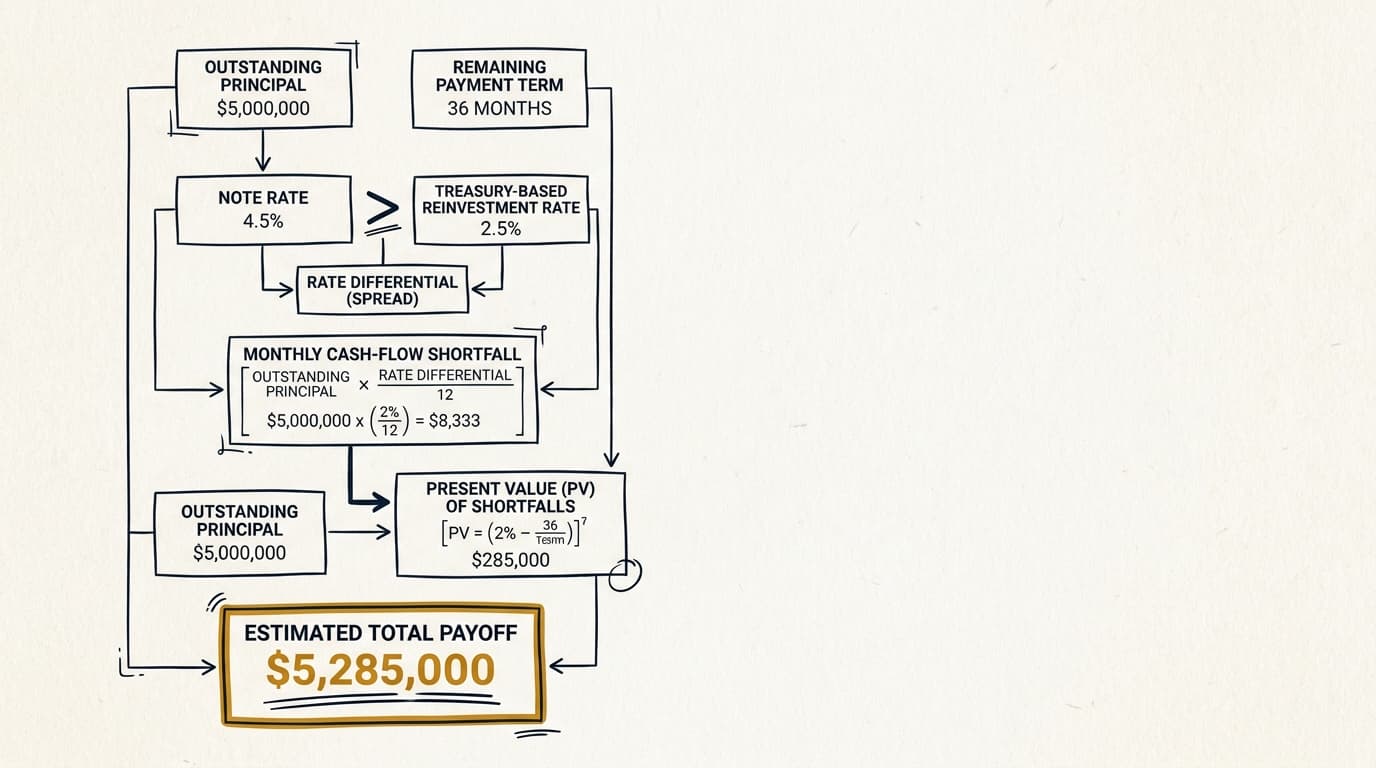

- A yield maintenance calculation usually turns on four inputs: unpaid principal balance, note rate, Treasury-based replacement rate, and remaining term.

- In the example below, a $7.8 million balance at a 6.25% coupon with 60 months left and a 3.80% Treasury-based rate produces an estimated yield maintenance charge of about $619,000.

- Total payoff is not just principal plus penalty. Accrued interest, servicing fees, and any contractual minimum prepayment charge may also apply.

- The loan documents control the exact method, including the spread over Treasury, the discount convention, and whether the charge is subject to a floor such as 1% of principal.

Yield maintenance calculation example

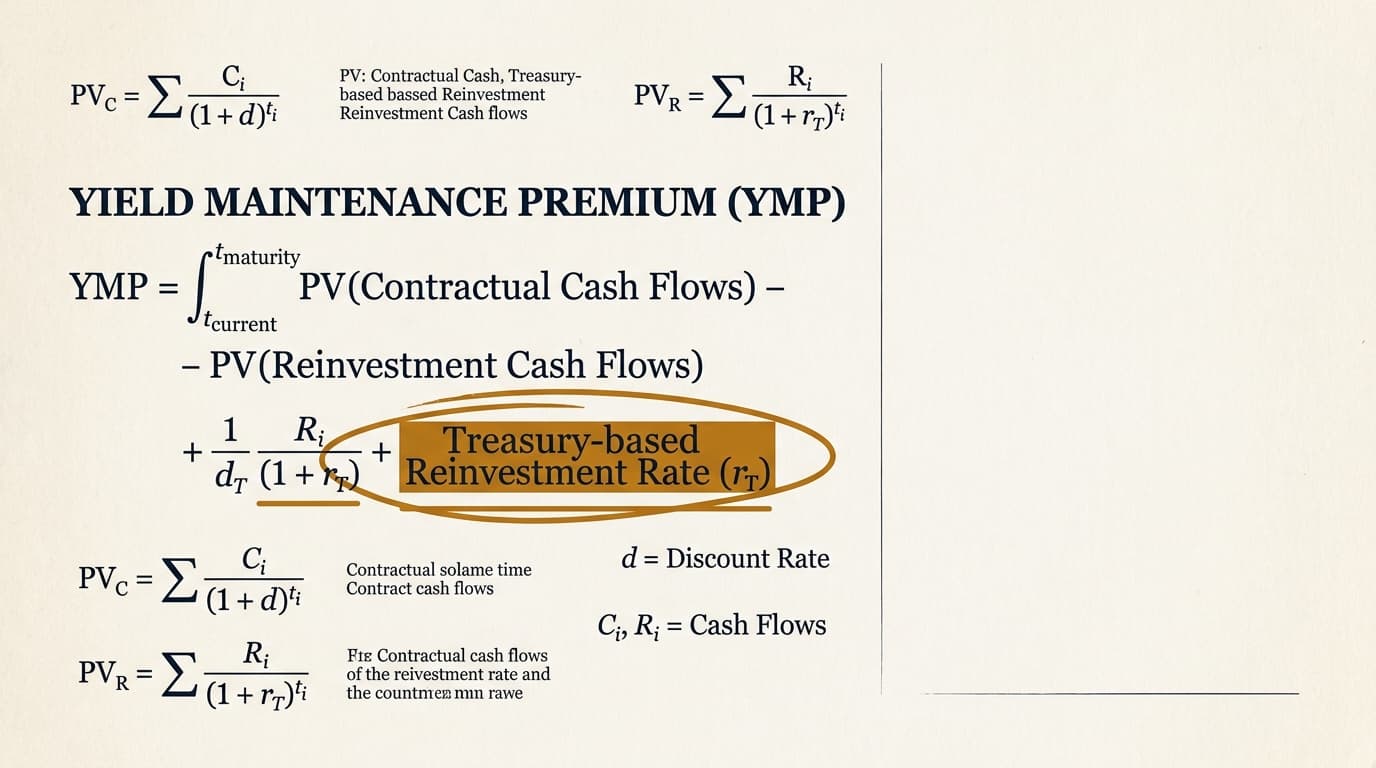

Yield maintenance tries to put the lender in roughly the same position it expected to be in if the loan had stayed outstanding. In most commercial loan documents, that means using a U.S. Treasury yield, sometimes with an added spread, and discounting the remaining shortfall back to the payoff date.

For a broader overview of commercial real estate yield maintenance, see the pillar page. For a clause-level review of what actually controls the math, see yield maintenance loan documents.

Sample loan inputs for the worked payoff case

This example uses a standard fixed-rate commercial mortgage with monthly amortization and a balloon maturity. The numbers are illustrative, but the method is the same one you see in many lender payoff provisions and agency servicing guides.

| Input | Sample value |

|---|---|

| Unpaid principal balance | $7,800,000 |

| Note interest rate | 6.25% |

| Amortization | 30 years |

| Remaining term to maturity | 60 months |

| Treasury-based reinvestment rate | 3.80% |

| Compounding/payment frequency | Monthly |

| Assumed minimum prepayment charge | Greater of yield maintenance or 1% of balance |

Freddie Mac’s explanation of yield maintenance and defeasance says the point is to protect the lender’s expected yield when a borrower prepays early. The Freddie Mac Optigo Seller/Servicer Guide makes the broader point: these provisions are document-driven, and the loan may instead have a lockout, defeasance, or some other prepayment structure. And under Freddie Mac servicing guidance on payoff statements, the number that matters is the servicer’s payoff statement, not your spreadsheet.

Step 1: Calculate the remaining monthly payment

Start with the contractual monthly debt service. Because the loan amortizes over 30 years at 6.25%, the payment comes from that 30-year schedule, not the 60 months left until the balloon date.

Monthly note rate = 6.25% / 12 = 0.520833%.

Number of amortization payments = 360.

Using the standard mortgage payment formula, the monthly payment on a $7,800,000 balance is approximately $48,024.

That payment includes both interest and scheduled principal. If you want the formula itself, see yield maintenance formula.

Step 2: Estimate the lender’s monthly reinvestment shortfall

The basic idea is simple: compare the loan’s contractual cash flow with what the lender could earn by reinvesting the prepaid funds at the Treasury-based replacement rate. In a simplified model, you can approximate that shortfall as the coupon minus the replacement rate, applied to the scheduled outstanding balance on each remaining payment date.

Here, the spread is:

- Note rate: 6.25%

- Replacement rate: 3.80%

- Interest-rate shortfall: 2.45%

Monthly shortfall rate = 2.45% / 12 = 0.204167%.

For a quick estimate, apply that monthly shortfall rate to the scheduled loan balance each month for the next 60 months. As the balance declines, the shortfall declines too. The first month’s lost spread is about:

$7,800,000 × 0.204167% = $15,925

By the final month, the scheduled balance is lower, so the shortfall is smaller. Add up those monthly shortfalls on an undiscounted basis and you get roughly $690,000 to $710,000, depending on the exact amortization schedule you use.

Step 3: Discount the shortfall over the remaining term

This is where the rough estimate becomes an actual yield maintenance model. The lender would have received those lost cash flows over 60 months, not all at once, so you discount each one back using the replacement rate required by the loan documents.

Monthly discount rate = 3.80% / 12 = 0.316667%.

Applying that discount rate to each monthly shortfall in the 60-month schedule produces an estimated present value of about $619,000.

That $619,000 is the estimated yield maintenance charge in this case study.

| Component | Estimated amount |

|---|---|

| Unpaid principal balance | $7,800,000 |

| Estimated present value of lost spread | $619,000 |

| 1% minimum prepayment charge | $78,000 |

| Applicable penalty | $619,000 |

| Estimated gross payoff before accrued interest and fees | $8,419,000 |

Because the calculated amount is higher than the 1% floor, yield maintenance controls here. If the Treasury-based rate were much closer to the coupon, the 1% floor might control instead.

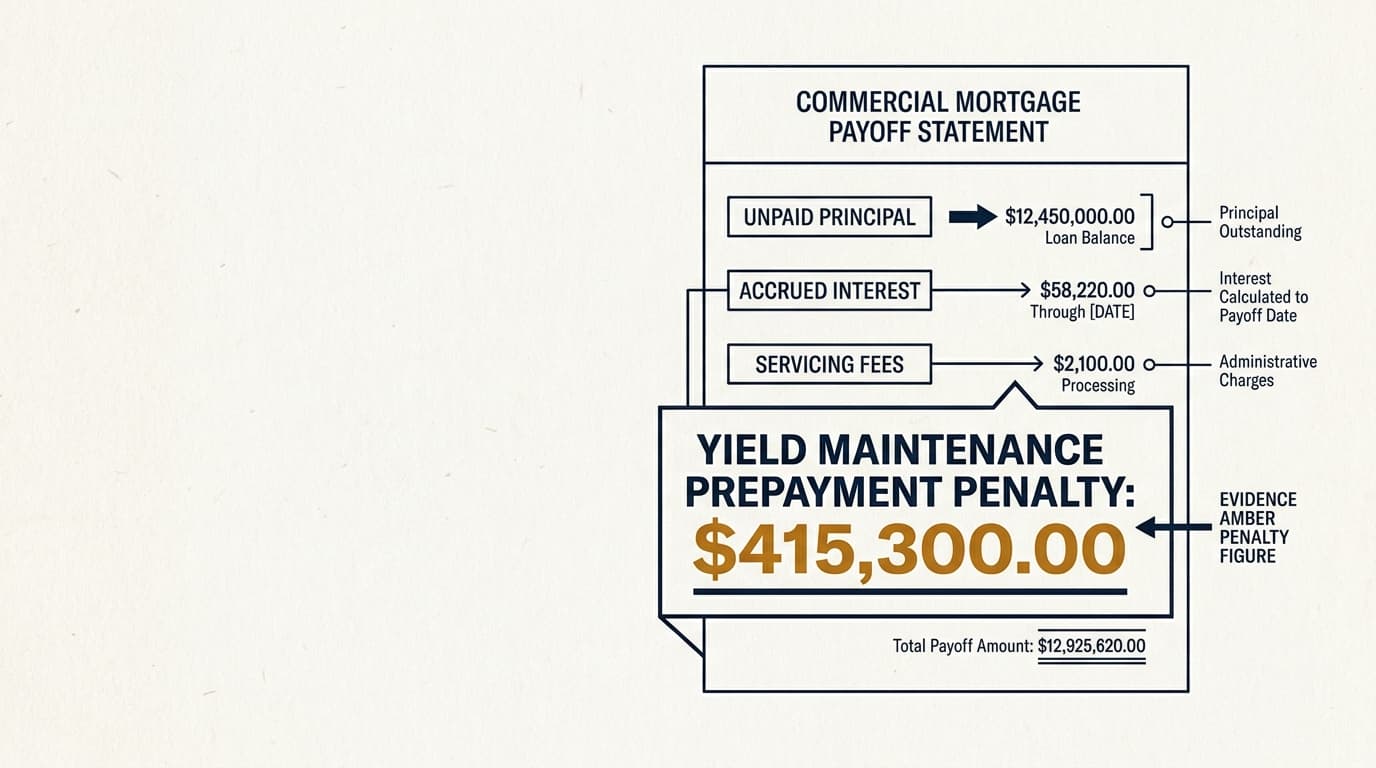

Step 4: Add principal and any contractual minimum prepayment amount

An estimated payoff starts with principal and the prepayment charge, then adds whatever else the note and servicing instructions require. Real payoff statements often include per diem interest through the payoff date, late fees if any are outstanding, document fees, and servicing charges.

- Start with the unpaid principal balance of $7,800,000.

- Add the calculated yield maintenance amount of $619,000.

- Compare that result against any contractual minimum, such as 1% of principal.

- Add accrued interest through the payoff good-through date.

- Add any servicing, legal, wire, or release fees listed in the payoff letter.

Freddie Mac guidance on commercial payoff statements is clear on one point: payoff figures are date-specific and need to be confirmed in a formal statement. Fannie Mae’s explanation of defeasance and yield maintenance makes the same practical point in different words: the exact premium depends on the note and the reinvestment benchmark in effect when the borrower prepays.

What changes the result most in practice

Most of the movement comes from three things: the interest-rate spread, the remaining term, and the balance path. A lower Treasury-based replacement rate, a longer remaining term, or a slower amortization schedule will usually increase the penalty.

| Scenario | Effect on estimated penalty | Why |

|---|---|---|

| Treasury rate falls from 3.80% to 3.00% | Higher | The lender’s reinvestment alternative is worse, so the lost spread is larger. |

| Remaining term drops from 60 months to 24 months | Lower | There are fewer future cash-flow periods left to discount. |

| Loan is interest-only for the remaining term | Higher | The balance stays larger for longer, which increases the monthly shortfall base. |

| Coupon and Treasury are close | Lower, sometimes near the floor | The protected spread is small. |

This is where a lot of high-level explainers get a little too neat. Two loans can have the same current balance and very different prepayment charges if one has an interest-only tail, a different Treasury spread requirement, or more time left. For planning a refinance or sale, that difference matters a lot more than any generic rule of thumb. If the loan is securitized, the analysis may also overlap with servicer rules discussed in cmbs yield maintenance and the comparison in yield maintenance vs defeasance.

Common document terms that alter a yield maintenance calculation example

The note and related loan documents determine the actual payoff method. The same basic inputs can still produce different results depending on how the documents define the Treasury index, spread adjustments, payment assumptions, and floors.

Which Treasury rate is used

Some notes refer to the U.S. Treasury yield that most closely matches the remaining term to maturity. Others use a specific interpolated maturity or add a spread. The U.S. Department of the Treasury daily yield curve data shows why this matters: yields move by maturity point, so using the 5-year point instead of an interpolated remaining term can change the answer.

Minimum penalty floors

Many commercial notes include a floor, often 1% of the outstanding balance, even when the pure yield maintenance result is lower. That matters more when rates are higher, or when the loan is late in its term and the spread-based charge has shrunk.

Scheduled balance versus actual balance method

Some calculations use the scheduled amortization stream that would have applied if the loan had not been prepaid. Others frame the lender’s loss around remaining installments or different principal assumptions. The governing language usually sits in the note, rider, or servicing provisions discussed in yield maintenance loan documents.

Yield maintenance calculation example vs. actual payoff statement

A spreadsheet example helps with planning, but it is not a payoff quote. The actual payoff statement may be different because of timing conventions, servicing fees, lockout restrictions, default interest, per diem accruals, and document-specific rounding.

That gap matters when a refinance or sale is on a real timeline. Model the penalty early, then get the formal payoff figure before a rate lock, purchase agreement amendment, or closing. For transaction-level timing analysis, see yield maintenance refinance or sale and the structure comparison in yield maintenance vs step-down. For another payoff-focused discussion, see yield maintenance prepayment penalty.

Frequently Asked Questions

What is a simple yield maintenance calculation example?

A simple yield maintenance calculation starts with the unpaid principal balance, measures the gap between the note rate and the Treasury-based replacement rate, applies that spread to the scheduled balance over the remaining term, and discounts those monthly shortfalls back to present value. In the worked case here, that produces an estimated penalty of about $619,000 on a $7.8 million loan.

Why does the Treasury rate matter so much in a yield maintenance calculation example?

The Treasury rate stands in for the lender’s reinvestment return after prepayment. If Treasury yields fall while the loan coupon stays fixed, the lender’s lost spread gets larger, and the yield maintenance charge usually rises. As the U.S. Treasury yield curve data makes obvious, even small moves in benchmark yields can materially change a present-value calculation on a large balance.

Is the payoff always principal plus the yield maintenance amount?

No. The formal payoff statement may also include accrued interest through the good-through date, servicing fees, legal or release fees, and any other charges required by the note. The example here shows the main economic pieces, but the amount you actually wire comes from the servicer’s payoff letter.

Do yield maintenance calculations differ by property type or region?

The math usually comes from the loan documents, not the property’s location. But market practice does vary by lender program, asset class, and whether the loan is securitized or held on balance sheet. A multifamily agency loan may follow different servicing conventions than a CMBS office loan, even if both use Treasury-based make-whole concepts. Local counsel and the servicer should still confirm state-specific release mechanics and recording fees.

When is an estimate too rough to rely on?

An estimate stops being good enough when the loan documents are unclear on the Treasury benchmark, the loan has an interest-only period, the payoff date keeps moving, or the deal is close enough to closing that fee-level accuracy matters. At that point, get the formal payoff statement and check it against the note.