Yield Maintenance Refinance or Sale: Decide With Net Proceeds

A yield maintenance charge can swing a refinance or sale decision by hundreds of thousands of dollars. The real question is straightforward: take the higher net proceeds available today, or wait and see whether a lower penalty or a better rate environment produces stronger property-level returns.

Yield maintenance can take a real bite out of sale or refinance proceeds, especially when the loan coupon sits well above current Treasury-based reinvestment rates. In a yield maintenance refinance or sale decision, the answer usually comes down to three things: how much cash you actually walk away with at closing, what you expect to earn if you keep the asset longer, and how much risk you are taking by waiting.

This article looks at how borrowers and advisors weigh refinance, sale, and hold decisions when yield maintenance is in play. The focus is practical: net proceeds, the rate backdrop, hold period, and property-level return assumptions, plus the modeling choices and loan-document details that often decide the outcome.

Key Takeaways

These decisions usually turn on the payoff model, not the term sheet headline. A sale price can look great and still lose to a refinance or delayed exit once you include the payoff balance, penalty, defeasance or legal costs, and ordinary closing friction.

- Yield maintenance is usually highest when market rates fall below the loan coupon, because the lender's lost interest spread gets larger. According to the Fannie Mae Multifamily guidance on prepayment premiums, these structures are meant to compensate for lost yield, which is why lower benchmark rates can raise the cost to exit.

- To make the decision cleanly, owners should compare three numbers on the same date: refinance proceeds net of payoff, sale proceeds net of payoff, and the projected internal rate of return from waiting 12 to 36 months.

- Commercial loans can use very different payoff mechanics depending on the note and security instrument. Reviewing the yield maintenance loan documents is necessary before assuming the quoted penalty is final or that an open-period prepayment is available.

- If the asset's leveraged return on the next dollar of equity is below the owner's reinvestment alternative, paying yield maintenance to exit can still make sense even when the penalty is large.

- For securitized debt, the refinance-or-sale analysis may need to include defeasance instead of a simple penalty. That distinction is covered separately in this comparison of yield maintenance vs defeasance.

What yield maintenance refinance or sale means in practice

A yield maintenance refinance or sale analysis asks a narrow question: which option creates the highest risk-adjusted value after loan exit costs? In practice, borrowers are not really choosing between labels like "refinance" or "sale." They are deciding what to do with trapped equity.

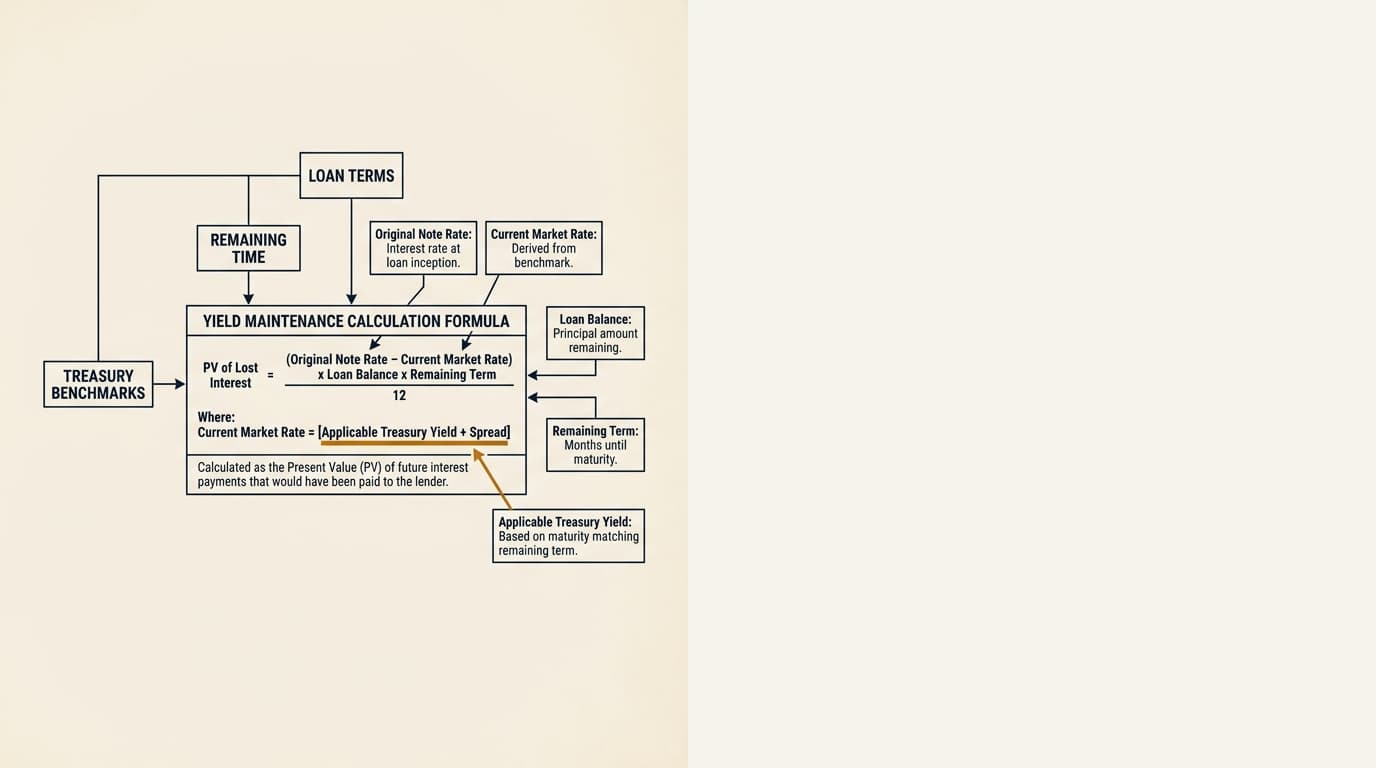

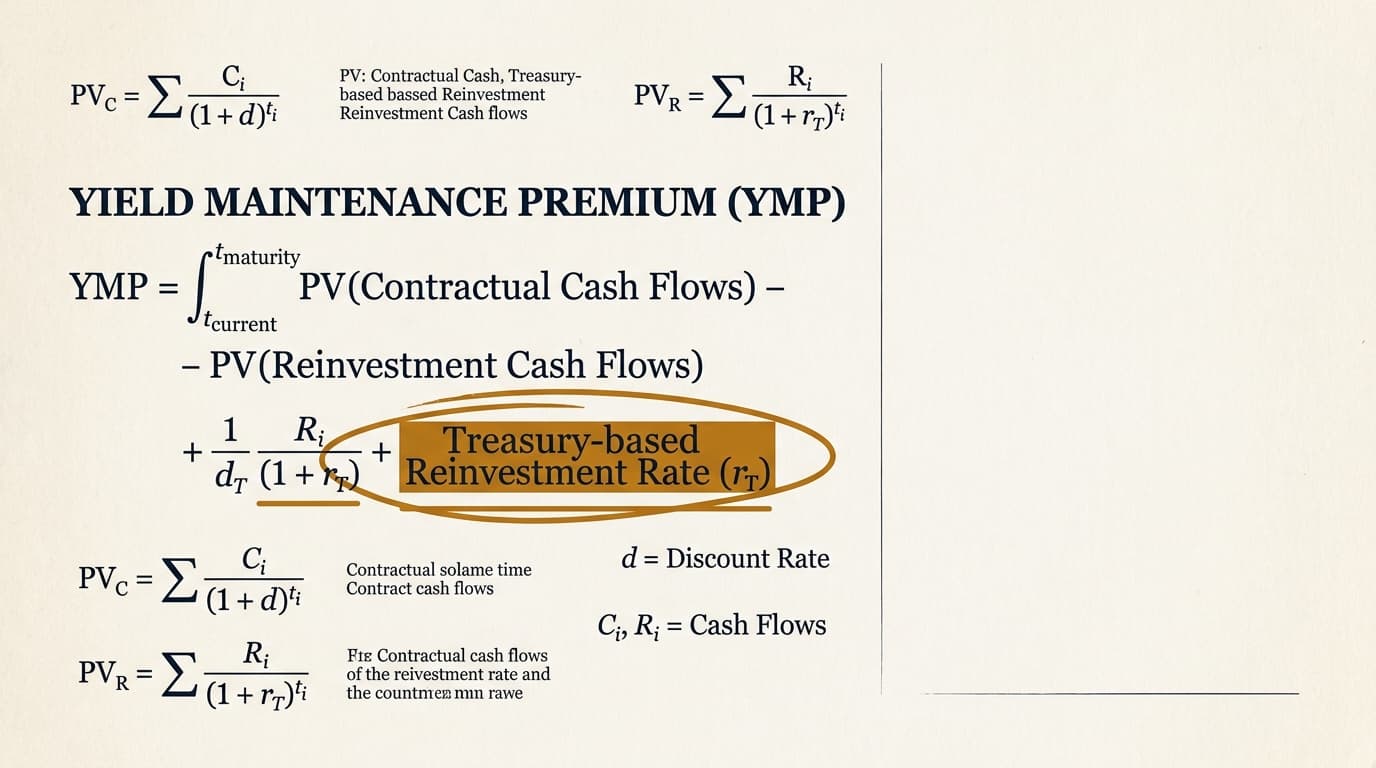

Yield maintenance is a contractual prepayment charge designed to preserve the lender's expected return when a fixed-rate loan gets paid off before maturity. According to the Freddie Mac Optigo Servicing Guide section on prepayment premiums, these charges usually tie back to the gap between the note rate and a specified reinvestment benchmark, discounted over the remaining term. For a broader overview of how this works across loan types, see this pillar page on commercial real estate yield maintenance.

That matters because the real question is rarely, "Can I afford the penalty?" The better question is whether paying it now produces a better outcome than holding the asset until the penalty declines or the loan reaches an open period.

The three variables that drive the answer

Most refinance-or-sale outcomes come back to three variables: penalty size, expected hold period, and property-level return assumptions. Change any one of them enough, and the answer can flip.

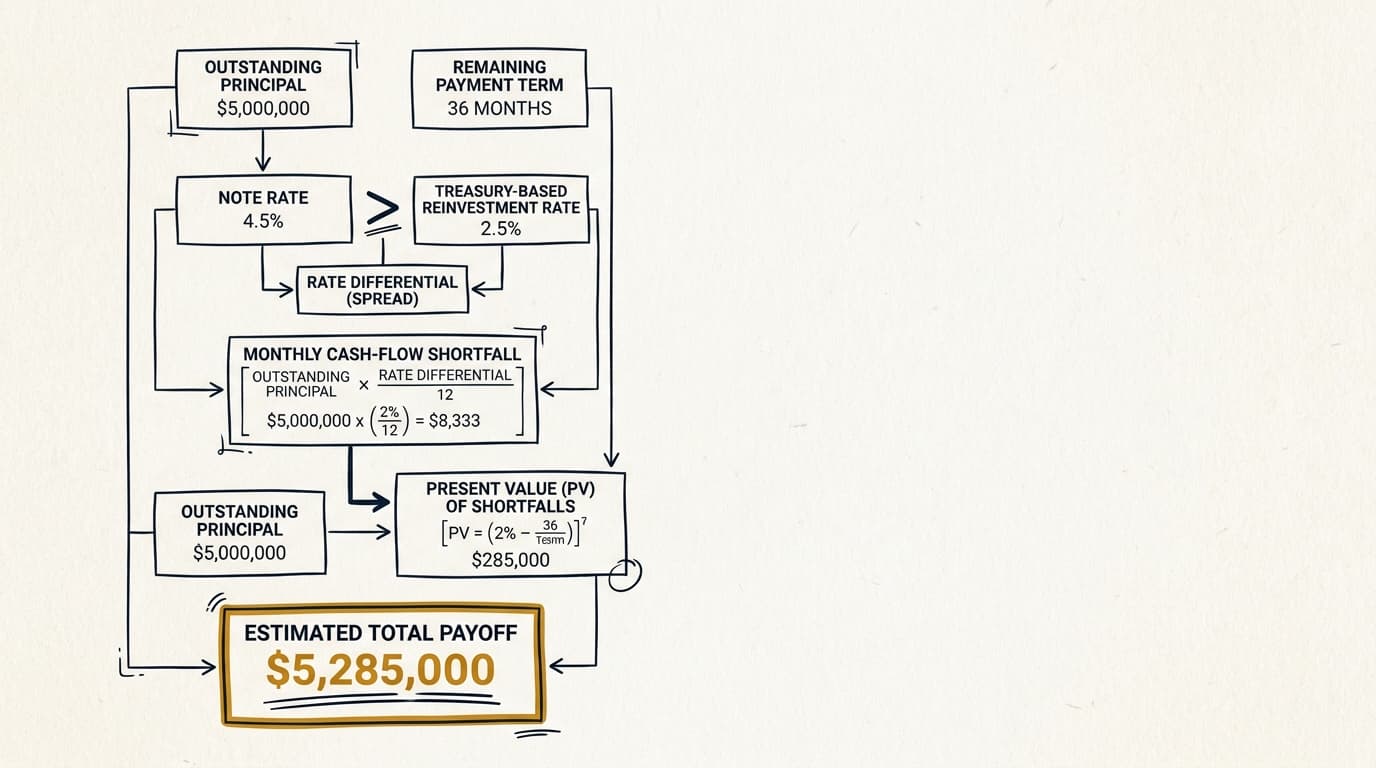

- Penalty size today. This includes unpaid principal balance, accrued interest, yield maintenance or defeasance, servicer fees, legal costs, and any spread required by the note formula. For the underlying math, use this explainer on the yield maintenance formula.

- Hold period if the owner waits. A 6-month delay and a 24-month delay are not remotely the same decision. The longer the delay, the more the analysis depends on NOI growth, cap rates, leasing risk, and capital expenditure assumptions.

- Return on retained equity. If the property can produce a low-teens leveraged return over the wait period, holding may outweigh a large current penalty. If expected returns are weak, exiting now may be better despite the fee.

Refinance vs sell vs wait: a side-by-side decision framework

The refinance, sale, and wait options should be modeled on a net present value basis using the same valuation date. Comparing nominal sale price to nominal refinance proceeds without adjusting for timing leads to bad conclusions.

| Option | Main objective | Primary inputs | Main risk | Best fit scenario |

|---|---|---|---|---|

| Refinance now | Reduce debt cost, pull cash out, or extend term | Current payoff, new rate, proceeds, DSCR, lender fees | Penalty offsets rate savings | New debt materially improves annual cash flow or solves near-term maturity risk |

| Sell now | Monetize equity and redeploy capital | Sale price, closing costs, payoff, taxes, penalty | Penalty reduces net proceeds below hold value | Buyer demand is strong and alternative investments offer higher returns |

| Wait | Preserve value until penalty declines or open period arrives | Future payoff, NOI growth, cap rate, carry costs, leasing risk | Rates, rents, or values move unfavorably | Expected hold-period return exceeds immediate exit economics |

Why net proceeds matter more than gross price

Gross sale price is not enough, because it ignores the debt exit cost that determines distributable equity. In plenty of cases, the difference between a good outcome and a bad one is not the sale cap rate. It is how much of the proceeds the payoff eats up.

According to the Consumer Financial Protection Bureau's Regulation Z resource, payoff statements in lending contexts are meant to identify the amount required to satisfy the obligation as of a specific date. In commercial real estate, that date sensitivity matters even more because yield maintenance can move with benchmark rates and with elapsed term. At Graphline, we treat the payoff statement as the anchor. The decision should rest on a defensible number, not a casual estimate from an early call.

How to model the refinance decision with yield maintenance

A refinance with yield maintenance works only if the present value of future benefits is greater than the all-in cost of getting out of the existing loan. Those benefits might include lower debt service, an extended maturity, released reserves, or additional proceeds.

Start with annual debt-service savings, because that is the usual reason owners consider paying the penalty. If the existing loan carries a 6.25% fixed coupon and a refinance would close at 5.40%, the apparent 85-basis-point improvement looks attractive on paper. But if the payoff includes a seven-figure prepayment charge, the break-even period can easily run past the owner's expected hold.

Refinance example: lower rate but limited benefit

This is where a lot of refinance cases fall apart. A lower coupon by itself does not justify the transaction. The refinance works only if the owner's total benefit during the expected hold period is greater than the current exit cost.

| Input | Amount |

|---|---|

| Current loan balance | $12,000,000 |

| Current note rate | 6.25% |

| Years remaining | 5.0 |

| Quoted yield maintenance and fees | $1,050,000 |

| Refinance rate | 5.40% |

| Estimated annual debt-service savings | $102,000 |

| New lender and closing costs | $180,000 |

In this scenario, the owner spends roughly $1,230,000 to exit and close the new debt, before any time-value adjustment. Annual savings of $102,000 imply a simple payback of more than 12 years. If the owner expects to sell in three years, the refinance is weak unless it also fixes another problem, such as a looming cash-management trigger, recourse issue, or an inability to fund tenant improvements under the current structure.

When refinancing still makes sense

Refinancing can still be the best option even with a large penalty if the current loan creates a bigger economic problem than the penalty itself. That comes up often when maturity risk, debt-service coverage, or reserve lockups are constraining the business plan.

- Maturity risk is near-term. If the existing loan matures before lease-up or stabilization is complete, an early refinance may remove the risk of having to refinance later under worse conditions.

- The new loan releases trapped capital. Additional proceeds may fund capital expenditures that lift NOI faster than the penalty destroys value.

- The current structure limits operations. Cash-management sweeps, reserve controls, or recourse terms can justify a costly refinance if they interfere with leasing or sale timing.

For comparison with more flexible borrower structures, this article on yield maintenance vs step-down explains why different prepayment regimes create different timing incentives.

How to model the sale decision with yield maintenance

A sale decision under yield maintenance should be judged on after-debt, after-friction equity proceeds, not on asset value by itself. Owners who focus only on cap-rate compression or a broker opinion of value can overstate what they will actually collect.

The sale model should include at least six items: contract price, broker fee, transfer and closing costs, current payoff balance, yield maintenance or defeasance amount, and expected taxes. In some deals, yield maintenance is not even the largest haircut. Taxes can be worse. That treatment varies by structure and jurisdiction, so it needs its own review separate from the debt analysis.

Sale example: strong price, weaker distributable cash

A higher asset value does not automatically make an immediate sale the best move if the debt structure captures a large share of the gain. The number that matters is net equity released at closing.

| Input | Amount |

|---|---|

| Sale price | $20,000,000 |

| Brokerage and closing costs | $550,000 |

| Loan payoff balance | $11,800,000 |

| Yield maintenance and servicer fees | $1,150,000 |

| Net cash before taxes | $6,500,000 |

If the owner believes the property can generate a 10% unlevered return on current value over the next 24 months through rent growth and lease rollover, waiting may produce a better total equity outcome even if the sale market is liquid today. But that only holds if the underwriting on rent growth, downtime, and exit cap rate is credible. This is exactly where optimistic hold cases tend to drift.

What buyers and brokers often miss

Sale negotiations often go sideways when the owner's expected net proceeds are anchored to value instead of payoff economics. A bidder may think the owner should take a market-clearing price, while the owner is effectively building the debt penalty into the reserve price.

That disconnect usually leaves three practical alternatives:

- Delay marketing until the penalty drops or the loan reaches a more favorable prepayment window.

- Explore loan assumption if the documents allow it and the buyer can qualify.

- Reposition and hold if incremental NOI growth is likely to offset the cost of waiting.

The assumption route is a separate analysis. It should never be treated as automatically available. The note and servicing requirements control.

When waiting is financially rational

Waiting makes sense when the expected value created during the hold period is greater than the cost and risk of delaying the transaction. That value can come from a lower future penalty, higher NOI, debt amortization, or a better sale or refinance market.

Two situations come up again and again. First, the existing loan is close to an open period or a materially cheaper prepayment window. Second, the property has clear near-term value creation, such as signed but not yet commenced leases, below-market in-place rents, or capital projects with a short payback.

A simple wait-versus-exit test

You can simplify the wait decision into a spread test: compare the expected equity gain from holding with the opportunity cost of capital and the downside risk if the market moves against you. If the expected gain is thin and heavily assumption-driven, immediate execution usually deserves more weight.

Example:

- Current sale net of payoff: $6.5 million

- Projected sale net of payoff in 18 months: $7.3 million

- Incremental gain from waiting: $800,000

- Required return on equity capital: 12%

- Opportunity cost on $6.5 million over 18 months: about $1.17 million on a simple annualized basis

Under that simplified framework, waiting underperforms the owner's alternative use of capital unless the property-level forecast improves or the owner's real reinvestment hurdle is lower. This is where a lot of hold recommendations fail. They focus on nominal future proceeds and skip the harder question of whether the added value actually pays for time and risk.

A practical decision matrix by hold period and rate environment

Hold period and rate environment usually decide which option deserves the most attention. Short holds tend to favor an immediate sale only when the current market is offering unusually strong pricing or when waiting does little to reduce the prepayment cost.

| Expected hold period | Rate environment | Likely best option | Reason |

|---|---|---|---|

| 0-12 months | Rates lower than note coupon | Wait or sell only with strong pricing | Penalty is often elevated; refinance savings may not recoup cost |

| 0-12 months | Rates near or above note coupon | Sell or refinance can work | Penalty pressure may be lower, improving immediate economics |

| 12-36 months | Stable rates, NOI growth visible | Wait often merits review | Owner may capture amortization, NOI lift, and lower future exit cost |

| 36+ months | Asset strategy changing | Case-specific | Decision depends more on business plan and capital allocation than penalty alone |

This framework is meant to be practical, not mechanical. Benchmark rates matter, but they are only one input. The property's ability to earn on retained equity matters at least as much as the penalty schedule.

Original analysis: the break-even hold period

The most useful internal metric is the break-even hold period, the point where the value created by waiting exceeds the immediate cost to exit. Most source material explains how prepayment cost is calculated. Far fewer sources connect that cost to an actual hold strategy at the property level.

One workable formula is:

Break-even months ≈ (current exit cost disadvantage) ÷ (monthly value creation from waiting)

Monthly value creation includes expected NOI growth translated into value, scheduled principal amortization, and the estimated monthly decline in prepayment cost, minus carry costs and required capital expenditures.

Example:

- Current penalty disadvantage versus preferred immediate action: $900,000

- Monthly debt amortization benefit: $22,000

- Monthly expected reduction in prepayment cost: $18,000

- Monthly NOI-related value creation net of capex carry: $35,000

- Total monthly value creation: $75,000

The break-even hold period is roughly 12 months. If the owner's underwriting supports a hold beyond 12 months and market risk is acceptable, waiting deserves a real look. If the likely hold is only 6 to 9 months, immediate execution may still be the better outcome, even if the owner hates the penalty. And most owners do.

Edge cases that change the answer

Several edge cases can overwhelm the base model even when the spreadsheet points somewhere else. Usually the issue is loan structure, property condition, or buyer constraints, not the penalty formula itself.

Cash management, lockbox, and servicer consent issues

Operational controls can materially reduce the value of waiting. If excess cash is trapped in lender-controlled accounts or major decisions require servicer consent, the owner's flexibility may be much lower than the hold model assumes.

Near-term lease rollover

Large lease expirations can make waiting much riskier than the spreadsheet suggests. A projected 100-basis-point cap-rate benefit from NOI growth disappears fast if anchor tenancy rolls and downtime lasts longer than underwriting assumed.

Assumption or structured sale alternatives

Some transactions can avoid or defer the economic effect of prepayment through loan assumption or other structured transfers, but the documents and lender approval govern. The controlling terms usually sit in the note, loan agreement, and related servicing provisions. That is why the yield maintenance loan documents review is part of transaction strategy, not a box-checking exercise.

What to review in the payoff statement and loan documents

The payoff statement and the governing loan documents decide whether the modeled penalty is actually payable on the proposed date and structure. A broker opinion or a lender conversation is not a substitute for the contract.

According to the Fannie Mae Uniform Instruments glossary and note structure references, note and security instrument definitions control payment obligations as written. In commercial loans, bespoke riders and servicing agreements can matter even more. Before deciding that refinance, sale, or wait is the best path, confirm these items:

- Identify the exact prepayment clause. Confirm whether the loan uses yield maintenance, defeasance, step-down, or another premium structure.

- Verify the benchmark and spread. The Treasury reference, spread, and discounting conventions can change the penalty materially.

- Check open-period rights. Some loans allow prepayment without premium during the final months before maturity.

- Confirm notice and timing requirements. Missing a notice window can shift the payoff date and cost.

- Review transfer and assumption provisions. A sale may be more workable if assumption is allowed.

- Match the payoff quote to the proposed closing date. A stale quote can distort the decision.

For examples of how payoff charges appear in practice, see this page on the yield maintenance prepayment penalty in an actual loan payoff.

Step-by-step: how to decide whether to refinance, sell, or wait

A defensible decision uses one integrated model, not three separate back-of-envelope estimates. The process below is built for owners, asset managers, brokers, and lenders evaluating the same asset on the same date.

- Request a dated payoff statement that includes unpaid principal, accrued interest, prepayment premium, servicing fees, and per diem assumptions.

- Review the governing note, loan agreement, and servicing provisions to confirm how prepayment, assumption, notice, and any open period actually work.

- Build a refinance case that includes new loan proceeds, lender fees, reserves, and annual debt-service savings.

- Build a sale case that includes contract price, brokerage, transfer costs, payoff amount, and estimated taxes.

- Build a wait case for 12, 24, and 36 months using explicit assumptions for NOI, cap rate, amortization, leasing risk, and future payoff cost.

- Discount all three cases to the same valuation date using the owner's real return hurdle or weighted average cost of capital.

- Stress-test the model for lower rents, slower lease-up, wider exit cap rates, and smaller reductions in the penalty.

- Select the path with the strongest risk-adjusted net present value, not the one with the prettiest headline rate or sale price.

This process also helps separate two questions that often get blurred together: whether the current loan is expensive to exit, and whether the property is still the best use of equity. They are related, but they are not the same question.

Frequently Asked Questions

Should I refinance or sell if my loan has yield maintenance?

The better option depends on net proceeds and expected hold-period returns, not on the penalty alone. If refinancing creates debt-service savings or strategic benefits that exceed the current payoff cost during your likely hold, refinance may work. If a sale releases equity that can earn more elsewhere, selling may be better. If neither immediate option clears your return hurdle, waiting is often the rational answer.

Does yield maintenance usually make selling a property uneconomic?

No. Yield maintenance reduces net sale proceeds, but it does not automatically make a sale uneconomic. A sale can still make sense if buyer pricing is strong, the property has limited future upside, the owner's alternative investments are better, or the hold-period risks are high. The right test is net cash after payoff and transaction costs versus expected risk-adjusted value from holding.

Is refinancing with yield maintenance worth it just to get a lower interest rate?

Usually not, unless the debt-service savings are large enough to recover the payoff cost within the expected hold period. A rate reduction that looks meaningful in basis points can still be economically weak after you include the prepayment premium, legal fees, lender costs, and the time value of money. Refinance decisions get stronger when the new loan also solves maturity risk or provides strategic proceeds.

How does the rate environment affect a yield maintenance refinance or sale decision?

When benchmark rates are below the existing note coupon, yield maintenance is often higher because the lender's reinvestment loss is larger. That usually makes an immediate refinance or sale less attractive. When rates rise toward or above the note coupon, the penalty may shrink, which can improve immediate exit economics. The exact result depends on the loan's benchmark, spread, and remaining term.

Does this analysis vary by market or property type?

Yes. Market-specific leasing risk, cap rates, and buyer liquidity can change whether waiting adds value. A multifamily asset in a market with stable occupancy and modest cap-rate volatility may justify waiting more often than an office asset facing heavy rollover in a soft leasing market. Local transfer taxes, title costs, and buyer demand also affect net sale proceeds, so the same loan structure can lead to different answers in different markets.