Yield Maintenance vs Step-Down: Key Cost Differences

Yield maintenance and step-down prepayment terms can lead to very different exit costs on the same commercial mortgage. That difference shapes refinance timing, sale negotiations, and whether paying off the loan early is just a hassle or too expensive to make sense.

Commercial mortgage prepayment terms can swing exit costs by hundreds of thousands of dollars on the same loan balance. If you're comparing yield maintenance vs step-down, the real issue is straightforward: which one fits your likely refinance window, sale timeline, and rate outlook.

This article compares the two where it actually matters, payoff economics before maturity. It covers how each penalty works, how each affects refinance and sale timing, where flexibility shows up or disappears, and what to check in the loan documents before closing.

Yield maintenance vs step-down: the short answer

Yield maintenance usually ties the prepayment charge to the lender's lost yield against a Treasury benchmark. A step-down penalty usually follows a preset schedule such as 5% to 4% to 3% to 2% to 1%. In practice, yield maintenance moves with interest rates and can stay expensive surprisingly late in the term. Step-down structures are easier to model and usually give borrowers more flexibility as the loan ages.

According to the Freddie Mac Multifamily Seller/Servicer Guide on yield maintenance, yield maintenance is meant to preserve the note holder's expected yield after an early payoff. By contrast, agency and bank term sheets often describe step-down penalties as a fixed percentage of the outstanding principal balance that drops each year, though the exact schedule varies by lender and product.

Key Takeaways

- Yield maintenance usually depends on remaining scheduled payments, a spread, and a Treasury-based reinvestment rate, so the penalty can jump when market rates fall.

- Step-down prepayment penalties usually follow a fixed schedule, for example 5%, 4%, 3%, 2%, 1%, which makes refinance and sale modeling more predictable at closing.

- For loans likely to be refinanced or sold within three to five years, step-down terms often preserve more exit flexibility than yield maintenance.

- For borrowers who expect to hold through maturity, the difference may matter less than coupon, proceeds, recourse, and assumption rights.

- Loan documents, not term-sheet labels, decide the outcome. Open periods, lockouts, partial release rights, and assumption language can matter just as much as the penalty formula.

What yield maintenance means in practice

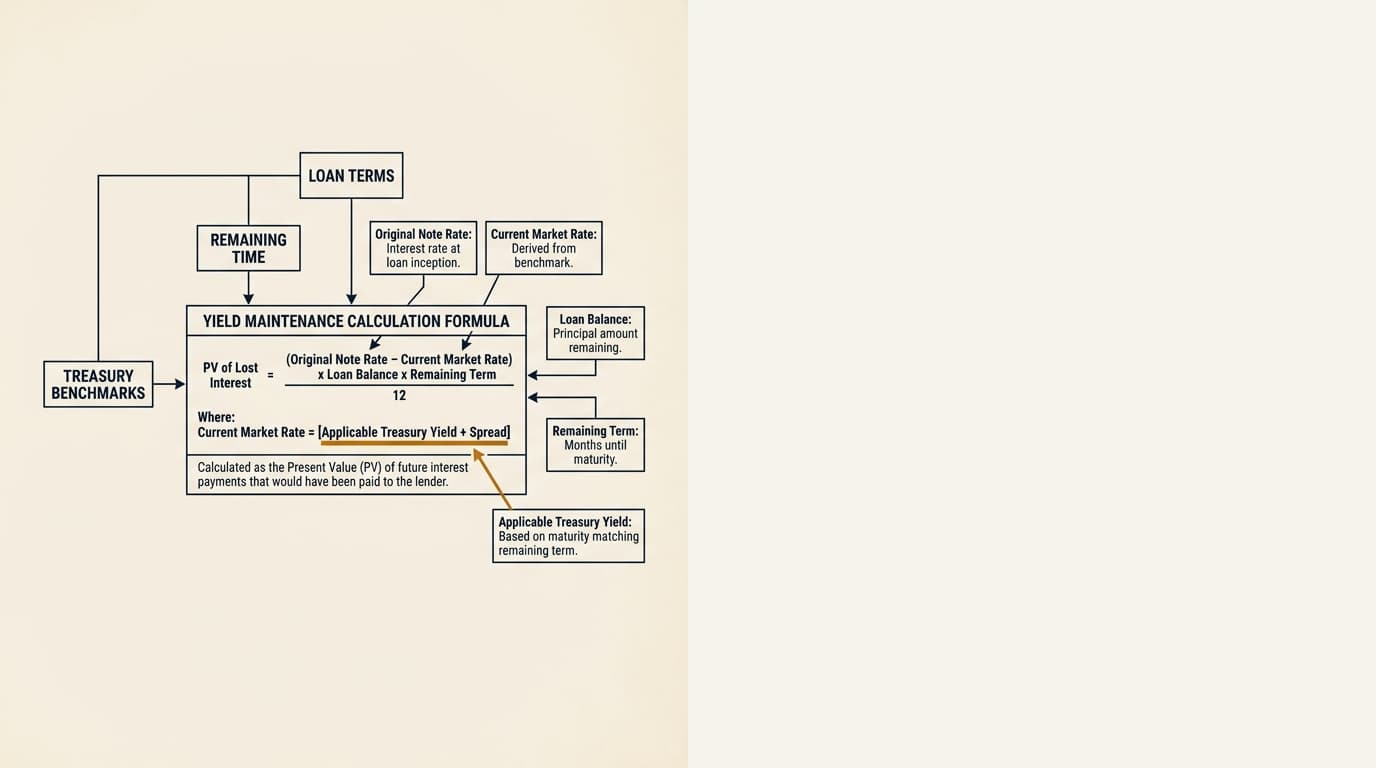

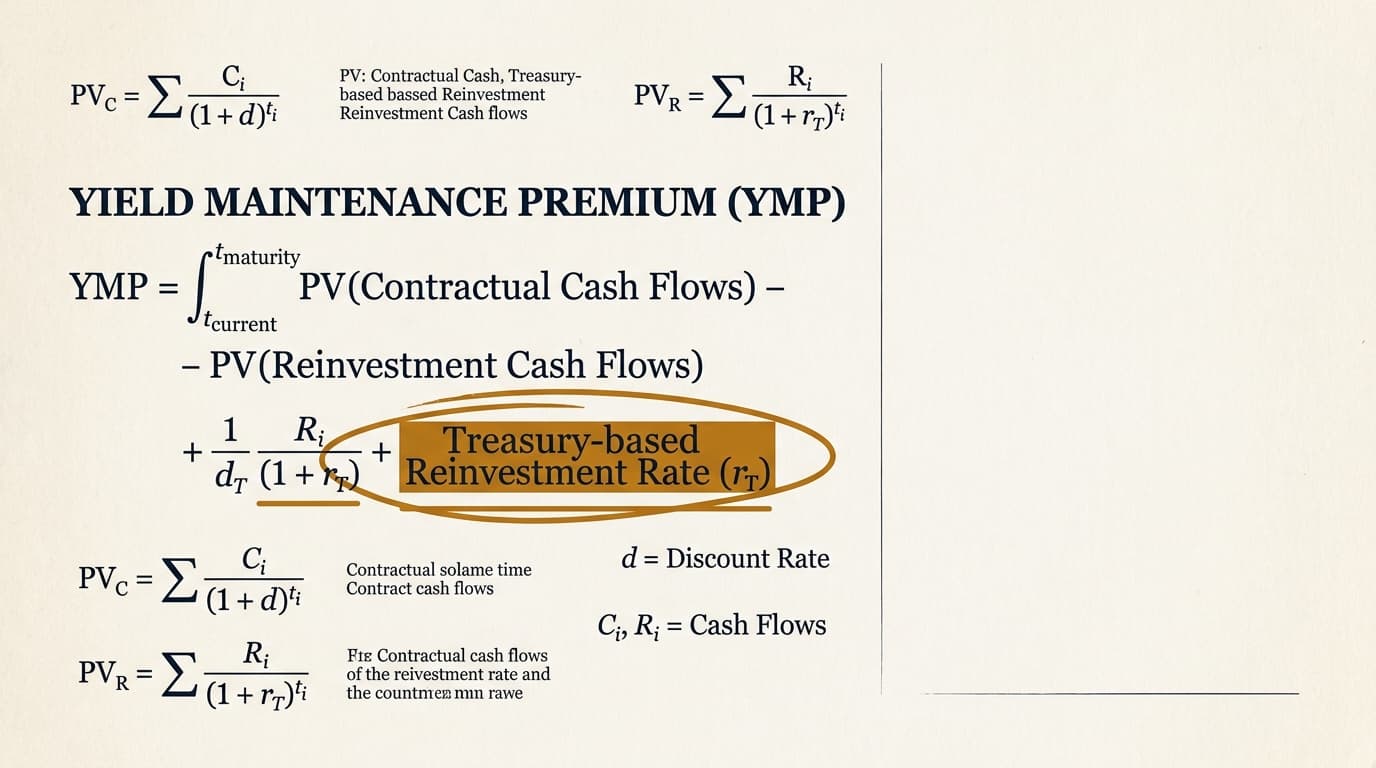

Yield maintenance is supposed to leave the lender in roughly the same economic position after an early payoff by compensating for the loss of above-market loan cash flow. According to the Fannie Mae Multifamily guidance on prepayment premiums, yield maintenance generally compares the loan coupon with a Treasury-based reinvestment rate and discounts the difference over the remaining term.

That creates two practical consequences. First, the penalty is not fixed at origination because part of it depends on rates at the time of prepayment. Second, the penalty can still be large years into the loan if the original coupon sits well above current Treasury yields.

For a full explanation of the math, Graphline's related guide on the yield maintenance formula breaks down the calculation in more detail. For this comparison, the key point is simpler: yield maintenance acts less like a flat fee and more like a market-linked make-whole.

Why yield maintenance can change so much

Yield maintenance is path-dependent. A borrower can model one payoff cost at closing and get a very different result two years later if Treasury rates move.

According to the Consumer Financial Protection Bureau's Regulation Z prepayment provisions, prepayment terms must be disclosed clearly in covered contexts, but clear disclosure does not make commercial loan economics easy to read. In practice, the variables that usually move the result are remaining term, unpaid principal balance, note rate, Treasury benchmark selection, spread, discount method, and any contractual floor.

The borrower takeaway is pretty clear: yield maintenance risk is highest when rates fall after origination and the borrower wants out well before maturity. That is why office, retail, hotel, and multifamily sponsors spend so much time on this clause when they are underwriting refinance options or sale timing.

What a step-down prepayment penalty means in practice

A step-down penalty usually charges a stated percentage of the outstanding principal balance that declines on a fixed annual schedule. In plain terms, a 5-4-3-2-1 structure means a payoff in year one triggers a 5% charge, year two 4%, and so on until the open period or maturity.

This structure is common for a reason. It is easy to explain, easy to model, and much less sensitive to market-rate swings than yield maintenance. According to the Freddie Mac Multifamily Seller/Servicer Guide section on declining prepayment premiums, some multifamily products allow declining premium structures instead of yield maintenance, subject to product rules and deal terms.

That said, step-down language still needs a careful read. Some schedules apply on loan-anniversary dates, others on calendar periods. Some loans have lockouts before the first step-down year even starts. Some include open periods only in the final 90 or 180 days. Those details can change exit cost in a meaningful way on a sale or refinance that lands near a cutoff date.

Why step-down is easier to underwrite

Step-down penalties are generally deterministic at closing. If the schedule is fixed and the payoff date is known, the borrower can estimate the charge without trying to guess Treasury yields.

That predictability matters in acquisition models and refinance memos. Sponsors can map specific hold periods, estimate return drag from a sale in year three versus year four, and negotiate buyer credits with less guesswork. The trade-off is that a fixed schedule can end up costing more than a market-linked structure in some rising-rate scenarios, especially if a refinance happens after rates move up sharply.

Yield maintenance vs step-down: side-by-side comparison

Yield maintenance and step-down clauses deal with the same lender concern, reinvestment risk after early payoff, but they assign that risk differently. Yield maintenance pushes more rate risk onto the borrower. Step-down gives the borrower more certainty and may leave the lender less fully protected in some cases.

| Feature | Yield maintenance | Step-down |

|---|---|---|

| Core design | Market-linked make-whole based on remaining cash flow and benchmark rate | Fixed percentage of outstanding principal declining by schedule |

| Rate sensitivity | High | Low |

| Ease of modeling at closing | Moderate to low | High |

| Refinance flexibility | Often limited when rates have fallen | Improves predictably over time |

| Sale negotiation certainty | Lower because future payoff cost can move | Higher because schedule is known |

| Late-term penalty risk | Can remain meaningful until open period | Usually modest if schedule has stepped down materially |

| Common use cases | Life company, agency, some portfolio and securitized structures | Bank, debt fund, some agency and portfolio structures |

Borrowers comparing these structures should separate simplicity from total cost. A simpler clause is not automatically cheaper. The right comparison is expected cost under the borrower's likely exit scenarios, not whatever label appears on the term sheet.

How each structure changes refinance economics

Prepayment structure directly affects whether a refinance creates real savings or just swaps one cost for another. In many cases, the headline rate on the new loan matters less than the all-in cost of getting out of the old one.

According to the Federal Reserve's open market operations framework, Treasury yields move constantly with macro conditions, and those moves feed straight into make-whole economics for yield maintenance structures. So a borrower can see a lower refinance coupon at exactly the moment when the yield maintenance penalty makes the deal hard to justify.

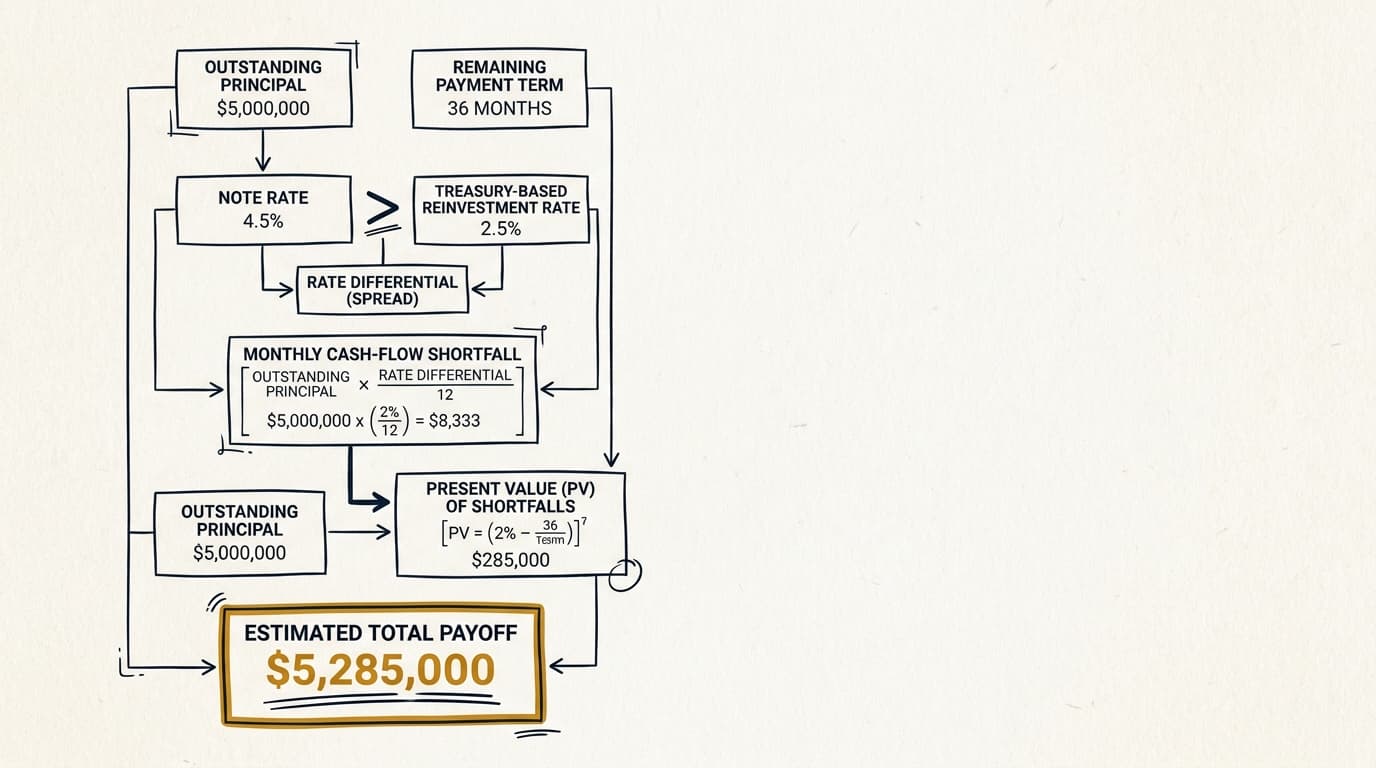

Refinance example: $10 million loan

A simplified example makes the difference clear. Assume a borrower has a $10 million fixed-rate commercial loan originated at 6.50% with five years remaining.

- Step-down case: the note has a 3% prepayment charge this year. Estimated penalty: $300,000.

- Yield maintenance case: the note uses a Treasury-based make-whole method. If comparable Treasury yields are materially below the note rate, the premium can exceed $300,000 by a wide margin, depending on discount rate, spread, and remaining amortization.

The refinance decision is not just a coupon comparison. Borrowers need to compare: (1) old debt service, (2) new debt service, (3) penalty, (4) lender fees, (5) legal and third-party costs, and (6) expected hold period after refinancing. A refinance that saves 75 basis points can still destroy value if the existing loan carries a large yield maintenance charge.

For a broader framework on exit timing, see Graphline's pillar page on commercial real estate yield maintenance, which explains where these clauses fit in the wider prepayment picture.

How each structure affects sale timing and buyer negotiations

On a sale, the prepayment clause affects not just net proceeds but also how much room the seller has on pricing and timing. A known step-down fee is easier to build into an asking-price strategy than a yield maintenance amount that can change with rates and settlement timing.

That matters even more in volatile markets. A seller under yield maintenance may choose to wait for an open period, maturity, or a more favorable rate backdrop. A seller under a step-down schedule may decide a slightly lower purchase price still works because the reduced penalty preserves target proceeds.

Buyer assumption and timing issues

Assumption rights can sometimes eliminate the need to prepay at all, but they are highly document-specific. According to the Freddie Mac Multifamily Seller/Servicer Guide and the Fannie Mae Multifamily Selling and Servicing Guide, assumptions require lender approval, underwriting, fees, and product-specific conditions.

In practice, a strict yield maintenance clause can push sellers into loan assumption discussions earlier in the sale process. A step-down structure may make a clean payoff more workable, especially once the penalty drops below the level that would blow up bid negotiations.

For borrowers comparing securitized options, the related guide on yield maintenance vs defeasance covers a separate but often related exit issue in CMBS structures.

Scenario analysis: when yield maintenance costs more and when step-down costs more

This decision is scenario-driven. Neither clause is always better. The better clause is the one that minimizes expected exit cost across realistic hold-period and rate-path assumptions.

| Scenario | Likely better for borrower | Why |

|---|---|---|

| Expected sale in 24-36 months, uncertain rates | Step-down | Known declining schedule preserves planning flexibility |

| Long hold to maturity, low probability of early payoff | Either, depending on coupon and proceeds | Penalty may never be incurred, so other loan terms may dominate |

| Falling-rate environment after origination | Step-down | Yield maintenance charges often rise when Treasury benchmarks fall |

| Rising-rate environment and midterm refinance | Yield maintenance may be less punitive | Make-whole amount can compress if reinvestment rates rise |

| Business plan depends on flexible sale timing | Step-down | Fixed costs are easier to price into negotiations |

| Lender offers materially lower coupon in exchange for yield maintenance | Depends on hold certainty | Lower ongoing debt service may offset reduced exit flexibility |

This is where a lot of term-sheet comparisons go sideways. They compare note rate and ignore option value. A step-down clause effectively gives the borrower a more predictable exit option. Yield maintenance usually protects the lender's reinvestment risk more fully, which can support better pricing, but that lower coupon should be weighed against the chance of an early refinance or sale.

A practical decision framework

Borrowers can evaluate yield maintenance vs step-down by assigning probabilities to likely exits instead of relying on a single base case. That is simply a better underwriting method for assets with lease rollover, renovation plans, partnership deadlines, or uncertain capital-markets timing.

- Estimate the probability of payoff in each year before maturity.

- Model the contractual prepayment cost for each year under the step-down schedule.

- Model a range of yield maintenance outcomes under higher, flat, and lower Treasury-rate scenarios.

- Add refinance fees, legal costs, defeasance risk where relevant, and expected sale friction.

- Compare expected total exit cost, not just the average penalty percentage.

This expected-value approach is about as close as you get to practitioner-level underwriting for prepayment terms. It captures an important point that borrowers sometimes miss: yield maintenance is not just a fee structure. It is also an interest-rate exposure embedded in the loan.

What borrowers should review before closing

The most important prepayment terms are often buried in definitions, exceptions, and timing provisions, not in the headline label. Borrowers should read the note, loan agreement, and any rider language closely before assuming that a step-down or yield maintenance clause works the way the term sheet suggests.

Document terms that change the outcome

Several provisions can materially change the economics:

- Lockout period: Some loans prohibit prepayment entirely for an initial period.

- Open period: Some allow prepayment without premium in the final 90, 180, or 270 days.

- Treasury benchmark selection: Yield maintenance clauses may specify a constant maturity Treasury, interpolated Treasury, or another benchmark method.

- Penalty floor: Some make-whole clauses include a minimum premium, such as 1% of principal.

- Partial release or partial prepayment rights: These can matter for multi-asset or phased sale strategies.

- Assumption rights: Assumability can preserve value where payoff is expensive.

According to the Consumer Financial Protection Bureau's disclosure resources, disclosures matter, but commercial borrowers should not rely on summary descriptions alone. The enforceable terms are in the signed loan documents.

How to model prepayment risk before signing

Borrowers should test prepayment structures before closing by building them into acquisition and refinance models instead of treating them like legal boilerplate. That exercise usually gives a clearer answer than negotiating on instinct.

- Identify the most likely exit windows for refinance, sale, recapitalization, or assumption.

- Pull the exact prepayment language from the draft term sheet and loan documents.

- Calculate the step-down penalty by year and month using projected principal balances.

- Run multiple interest-rate scenarios to estimate a range of yield maintenance outcomes.

- Add transaction costs such as legal fees, servicing fees, lender charges, and replacement-debt costs.

- Test net sale proceeds and refinance savings under each prepayment structure.

- Negotiate for open periods, lower floors, or more favorable assumption language if exit flexibility matters to the business plan.

Graphline is built around that practical need: payoff statements should be auditable, document-based, and fast enough to use in live deal analysis, not after the decision has already been made.

Frequently Asked Questions

Is yield maintenance always more expensive than a step-down prepayment penalty?

No. Yield maintenance is often more expensive when market rates have fallen below the loan coupon, but it can be less punitive in rising-rate scenarios. The actual result depends on the note rate, remaining term, benchmark Treasury yield, spread, discount method, and any minimum penalty floor in the loan documents.

Which structure is better for a borrower planning to sell within three years?

A step-down structure is often easier to manage for a sale inside three years because the penalty is usually fixed and visible from closing. That makes net proceeds easier to model and buyer negotiations easier to manage. Yield maintenance can work against a near-term sale if rates fall after origination and the make-whole amount increases.

Do banks, life companies, and agency lenders use the same prepayment structures?

No. Structures vary by lender type, product, and asset class. Life company and agency executions often use yield maintenance or other make-whole provisions, while bank and portfolio loans more often use step-down schedules, though there are plenty of exceptions. Borrowers should confirm the exact structure in draft documents rather than rely on lender category alone.

Does prepayment treatment vary by property type or market?

Yes. Multifamily agency executions may offer different prepayment options than office, retail, industrial, or hotel loans, and borrower leverage in negotiating terms can vary by market liquidity and lender competition. In primary markets with strong lender demand, sponsors may have more success negotiating open periods or alternative structures than in thinner markets or transitional asset situations.

Can a borrower avoid both yield maintenance and step-down penalties by assigning the loan to a buyer?

Sometimes, but only if the loan is assumable and the lender approves the buyer. Assumption typically requires underwriting, legal review, fees, and satisfaction of loan-document conditions. Where assumability is limited or timing is tight, payoff may still be the practical path.