Yield Maintenance Treasury Rate: Which Rate Is Used?

Most yield maintenance disputes start with a single input: the Treasury rate. Loan documents usually tie the calculation to a specific Treasury security or an interpolated Treasury yield matched to the remaining term, and even a 10- to 25-basis-point move can materially change the prepayment charge.

The Treasury benchmark in a yield maintenance calculation is usually the U.S. Treasury yield that most closely matches the loan’s remaining term to maturity, but the loan documents control. That sounds like a small detail. It isn’t. A 10- to 25-basis-point shift in the benchmark can change a commercial mortgage prepayment charge by tens of thousands of dollars on a mid-size loan.

This article explains which Treasury is usually used in a yield maintenance treasury rate calculation, how lenders pick it, where the definition usually shows up, and how to check the assumption against source data. For a broader overview of commercial real estate yield maintenance, Graphline’s pillar page covers the full structure, timing, and alternatives.

Key Takeaways

Here’s the short version.

- The benchmark is usually the U.S. Treasury constant maturity yield or another Treasury yield named in the note or deed of trust, chosen to match the remaining term to maturity as closely as the document allows.

- Loan documents often add a spread floor, such as the greater of the Treasury yield plus a stated spread or a stated minimum rate. That can keep the penalty from dropping when market rates fall.

- The U.S. Department of the Treasury daily Treasury par yield curve rates show yields moving daily across standard maturities, so the payoff quote date can materially change the result.

- The Federal Reserve H.15 Selected Interest Rates release publishes standardized tenors, not every exact remaining term. That is why some lenders interpolate and others use the nearest published maturity.

- Check the benchmark definition, quote date, spread, floor, and discounting convention against the payoff statement and the yield maintenance loan documents.

What is the yield maintenance treasury rate?

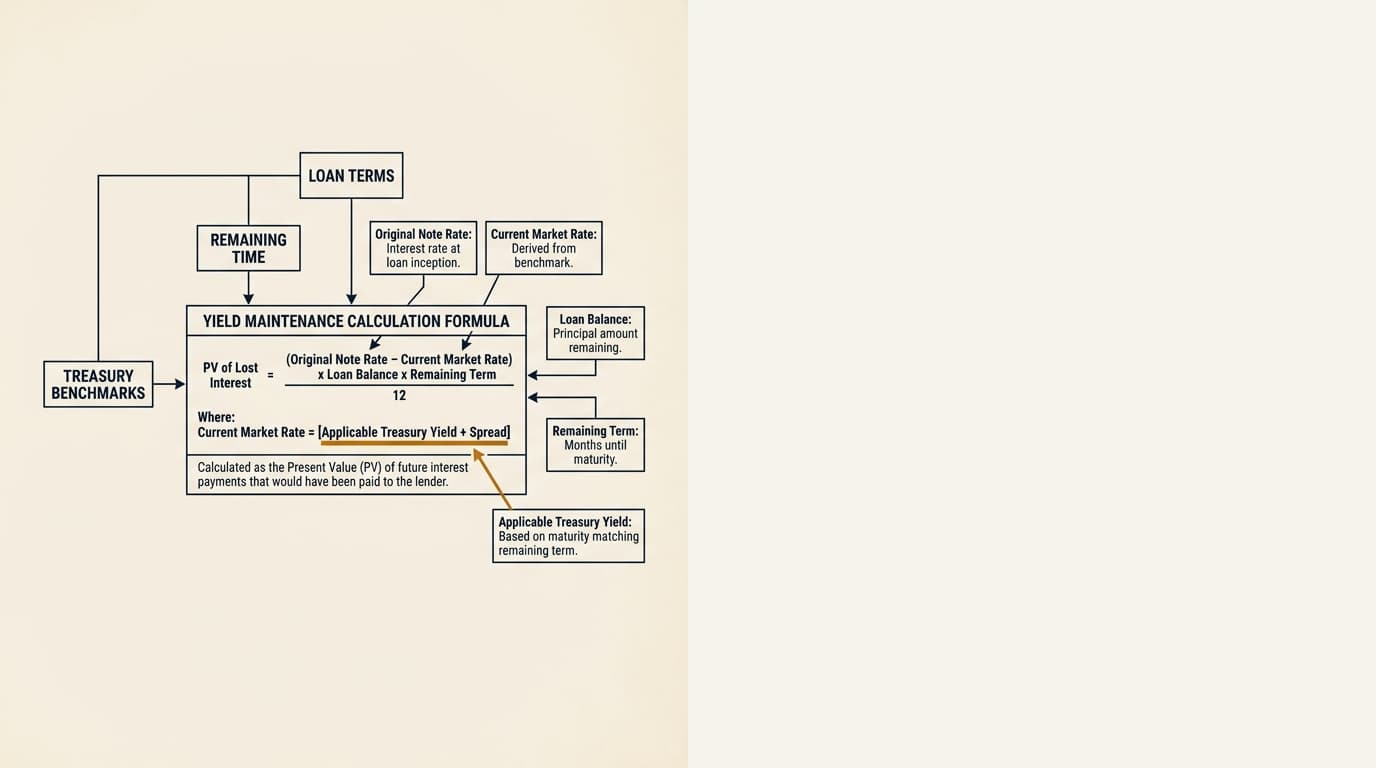

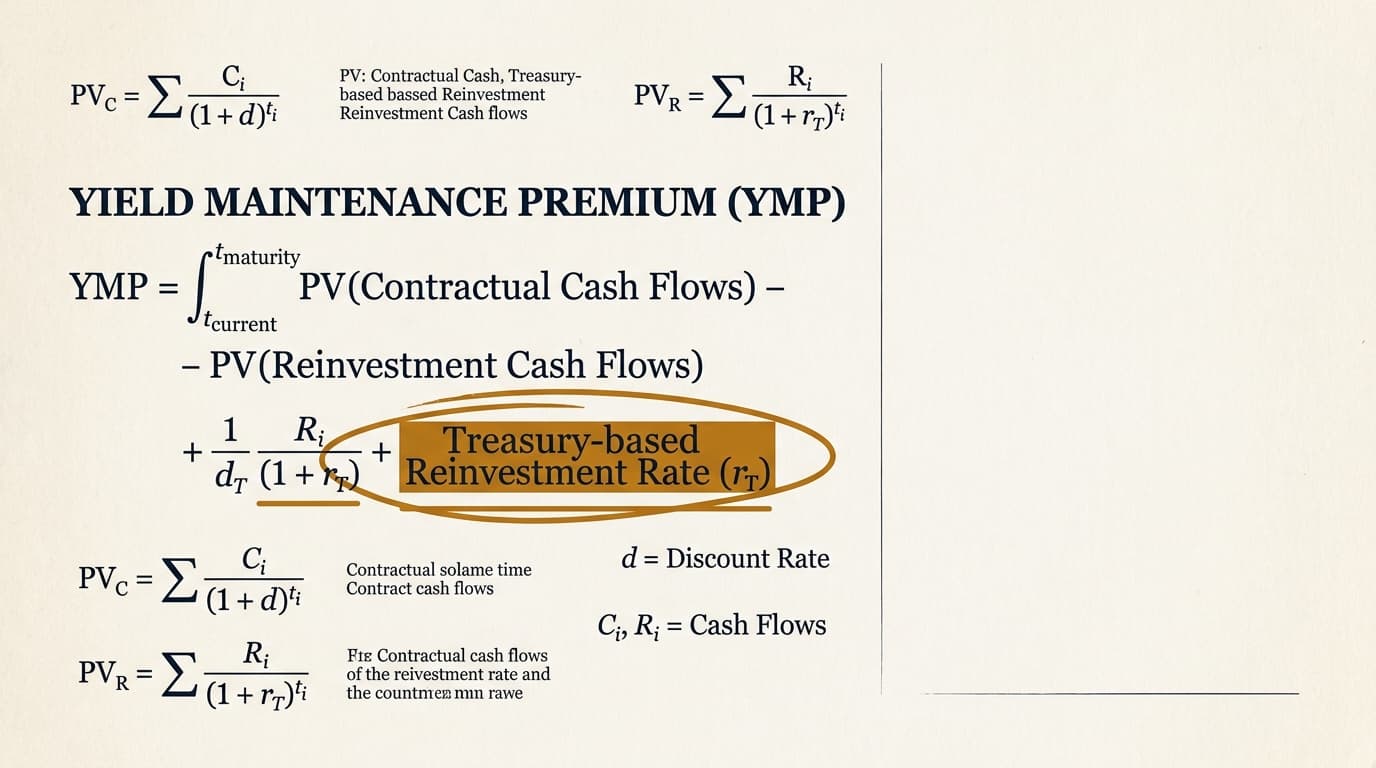

The yield maintenance treasury rate is the Treasury yield used to discount the lender’s lost interest when a loan is prepaid before maturity. In most structures, a lower Treasury yield relative to the note rate means a larger present-value penalty.

That comes straight from the math. The lender compares the loan’s contract cash flows with reinvestment at a Treasury-based discount rate, usually with an added spread. If the replacement rate sits well below the loan coupon, the lender’s economic loss is bigger. Graphline’s separate page on the yield maintenance formula walks through the calculation in detail.

Investopedia’s reference on yield maintenance describes the purpose clearly: compensate investors for the gap between the original loan yield and what the market will pay after prepayment. In commercial real estate lending, that market proxy is usually a Treasury yield because Treasuries are liquid, easy to observe, and published daily by official sources.

Which Treasury yield is typically used in yield maintenance?

Most loan documents point to a Treasury yield that matches the loan’s remaining term, not the original term and not just whatever is published on the prepayment date. In practice, that usually means a constant maturity Treasury series, a Treasury note or bond maturing near the same date, or an interpolated yield between two published maturities.

In CRE payoff work, three conventions show up most often:

| Document convention | How it works | Audit implication |

|---|---|---|

| Nearest published Treasury maturity | Use the Treasury tenor closest to the remaining scheduled term, such as 5-year or 7-year. | Check whether the lender rounded up or down and whether the document allows that method. |

| Interpolated Treasury yield | Blend two published Treasury maturities to approximate the exact remaining term. | Verify the interpolation method and source curve date. |

| Treasury security maturing closest to loan maturity | Use a specific on-the-run or comparable Treasury note or bond near the scheduled maturity date. | Confirm the exact security selected and whether the document calls for bid, ask, or yield data. |

The Treasury’s daily par yield curve page publishes standard maturities including 1 month, 2 month, 3 month, 4 month, 6 month, 1 year, 2 year, 3 year, 5 year, 7 year, 10 year, 20 year, and 30 year. Many loan documents drafted for securitized or balance-sheet execution refer to those standard maturities indirectly, using terms like “Treasury Rate,” “Interpolated Treasury Rate,” or “U.S. Treasury yield with a maturity comparable to the remaining Average Life.”

The practical point for borrowers is simple: there is no single Treasury used for every loan. The benchmark is whatever the note, mortgage, or rider says it is. That is why document review comes before math review every time.

How lenders select the Treasury benchmark

Lenders and servicers usually start with the time remaining between the proposed prepayment date and the scheduled maturity date, then apply the definition in the loan documents. If the documents are precise, the process is mostly mechanical. If they are loose, judgment creeps in, and that is where disputes start.

- Identify the scheduled maturity date and the intended payoff date.

- Calculate the remaining term, usually in months or as a year fraction.

- Read the defined term for “Treasury Rate” or similar language in the note and security instrument.

- Pull the source series from the named publication date or determination date.

- Apply any interpolation, spread, or floor required by the documents.

- Use that rate in the present-value discounting step.

The Federal Reserve’s H.15 Selected Interest Rates publication provides Treasury yields through market series commonly used in lending and finance documents. Cornell Law School’s Legal Information Institute explanation of present value makes the second piece clear: lower discount rates produce higher present values. That is the direct reason benchmark selection changes payoff amounts.

If the documents are ambiguous, focus the audit on whether the servicer used a method that fits past practice, document hierarchy, and any defined calculation-agent authority. This comes up a lot in securitized loans, which Graphline covers separately on its page about cmbs yield maintenance.

Why small benchmark changes affect the penalty

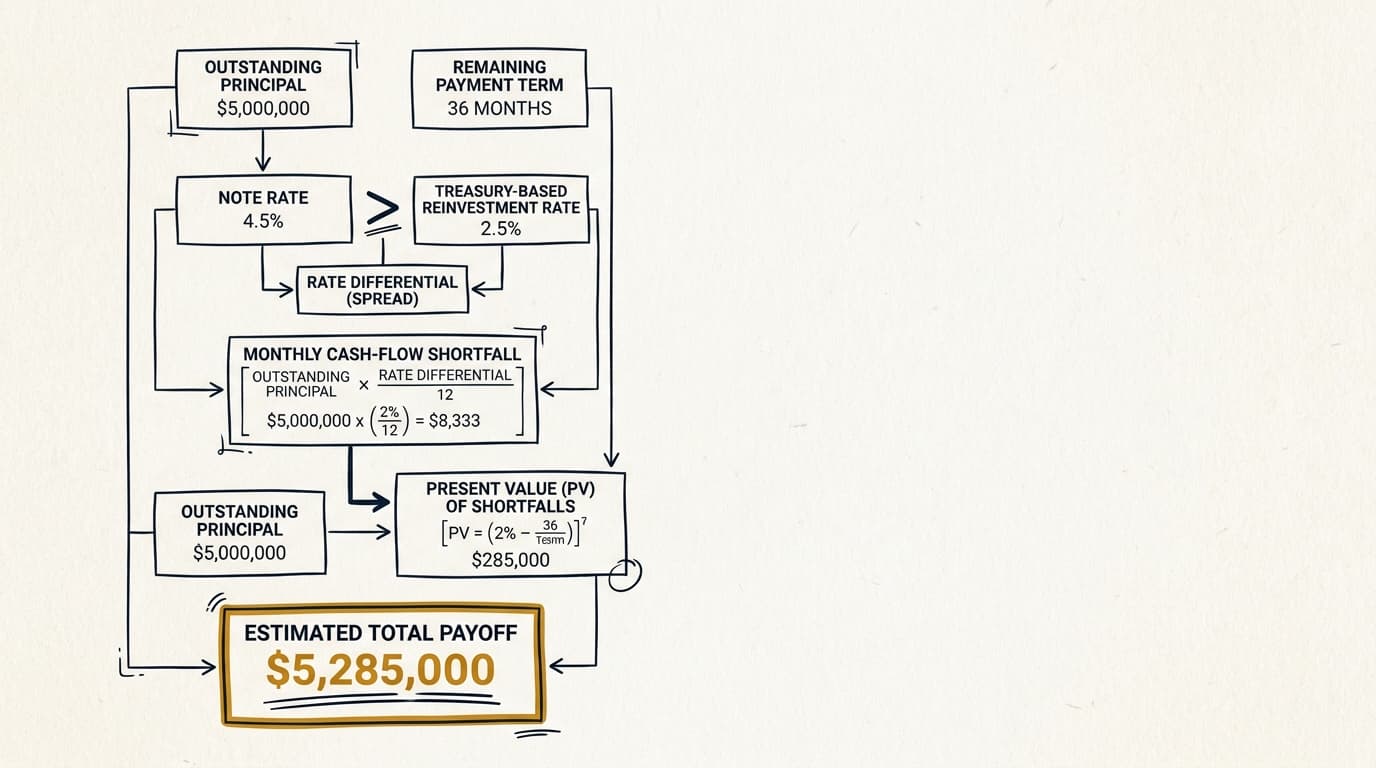

A small Treasury move can produce a large penalty difference because the benchmark is applied across every remaining scheduled payment and the balloon balance. The effect gets stronger on larger balances, low-amortization structures, and loans with several years left to maturity.

Take a simplified example: a $10 million loan with a 6.00% note rate, interest-only payments, and 4.0 years remaining. If the lender discounts the remaining cash flows at 4.50% instead of 4.25%, the present value of the lender’s forgone yield changes materially because every monthly interest shortfall is discounted at a different rate. On a structure like that, a 25-basis-point benchmark move can change the penalty by well over $50,000, sometimes more, depending on the spread and any floor language.

This is fixed-income math, not lender creativity. The U.S. Securities and Exchange Commission’s investor education on fixed-income securities notes that bond values are highly sensitive to market yields, especially when cash flows extend over longer periods. Yield maintenance applies that same logic to loan cash flows.

The effect gets even stronger when rates fall, because the gap between the note rate and the Treasury-based reinvestment rate widens. Readers comparing exit structures should also look at Graphline’s analysis of yield maintenance vs step-down and yield maintenance vs defeasance.

Treasury rate selection example

An audit example shows why the exact Treasury series matters more than many borrowers expect. Two lenders can produce different payoff charges from the same balance if one uses the nearest published maturity and the other interpolates, even when both are acting within broad document language.

| Input | Scenario A | Scenario B |

|---|---|---|

| Outstanding principal | $8,250,000 | $8,250,000 |

| Note rate | 5.85% | 5.85% |

| Remaining term | 6.4 years | 6.4 years |

| Treasury method | Nearest published maturity | Interpolated between 5Y and 7Y |

| Benchmark result | 4.18% | 4.07% |

| Spread added | +0.50% | +0.50% |

| Discount rate used | 4.68% | 4.57% |

In that setup, Scenario B produces a lower discount rate and therefore a higher present-value penalty. That is not a math mistake. It is a benchmark-definition issue. If you are reviewing a quote, ask for the exact Treasury source, the publication date, the selected tenor, and any interpolation workpaper. Those details drive the answer.

For a fuller numerical walkthrough, Graphline’s yield maintenance calculation example shows how the benchmark rate flows into the payoff amount.

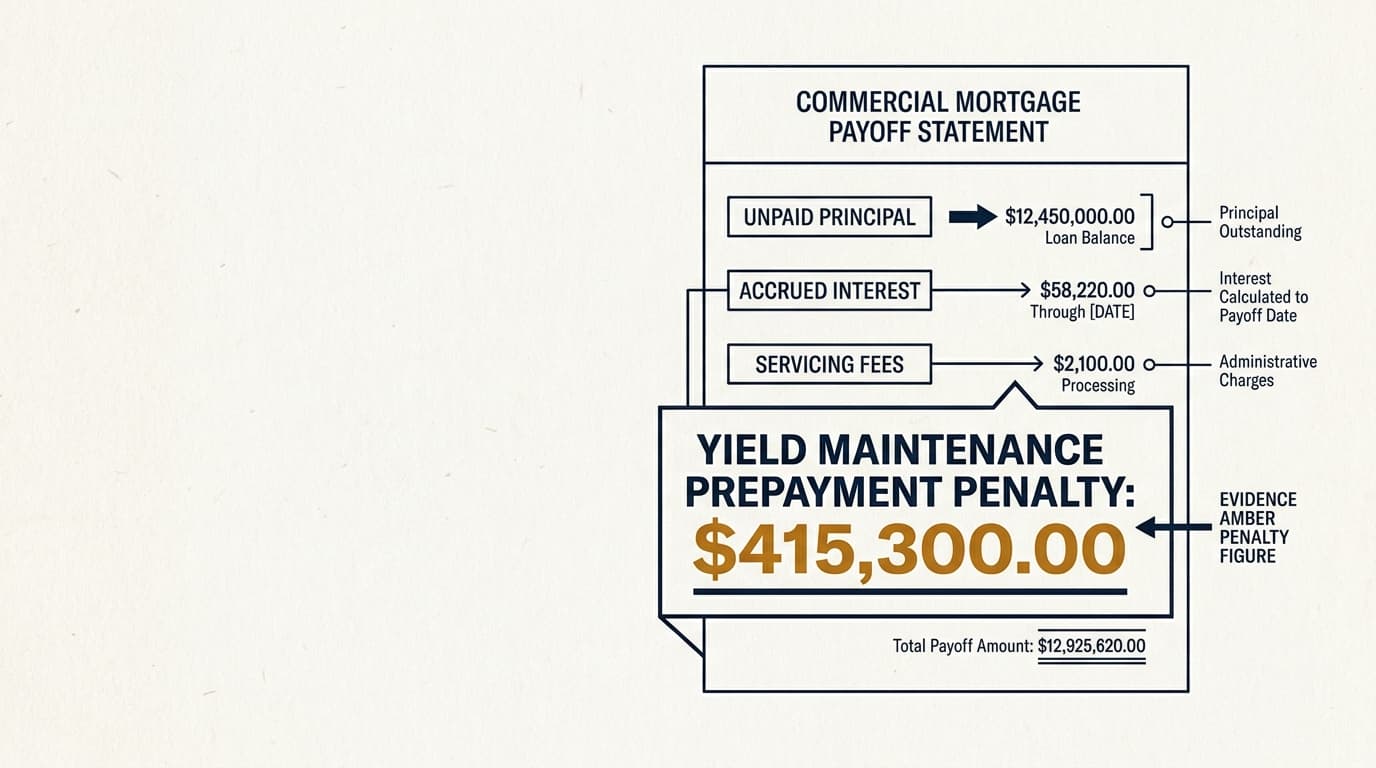

What to audit in lender payoff calculations

The cleanest way to audit a yield maintenance treasury rate is to test the lender’s benchmark selection before you test the rest of the formula. If the benchmark is wrong, the downstream present-value math can be flawless and the answer can still be wrong.

- Pull the note, mortgage, rider, and any servicing commentary that defines the Treasury benchmark.

- Confirm the exact determination date stated in the payoff statement.

- Match the remaining term to the Treasury tenor or interpolation method required by the documents.

- Cross-check the published yield against the Treasury daily yield curve data or another specifically named source in the loan documents.

- Verify any added spread, minimum rate, or floor.

- Recalculate the present value and compare it to the lender’s payoff statement.

In practice, four document issues drive a lot of disputes:

- Source ambiguity: the documents say “Treasury yield” but do not identify the publication series.

- Term-matching ambiguity: the documents allow either the nearest maturity or an interpolated equivalent.

- Date ambiguity: the benchmark may be set as of the quote date, lock date, or a date a specified number of business days before prepayment.

- Floor mechanics: the lender may apply a minimum spread-adjusted rate that overrides the observed Treasury yield.

Those points often sit in ancillary definitions rather than the prepayment paragraph itself. That is why reviewing the full yield maintenance loan documents matters just as much as reviewing the payoff statement. If you are evaluating the broader prepayment economics, Graphline’s analysis of the yield maintenance prepayment penalty explains how the benchmark fits into the total charge.

Common document variations and edge cases

Document wording varies enough that two loans originated in the same year can still use different Treasury selection methods. Edge cases matter most when the remaining term falls between standard tenors, Treasury markets are moving fast, or the loan is in servicing.

What happens when the remaining term falls between standard tenors?

If the remaining term does not line up with a standard Treasury maturity, lenders usually either choose the nearest published tenor or interpolate between the two surrounding tenors. The right method depends on the contract language, not on market custom alone.

As of 2026, Treasury publishes only specific standard maturities, so a 6.4-year remaining term does not have a directly published daily par yield. That is the most common reason interpolation disputes come up.

Does the payoff quote date change the rate?

Yes. Treasury yields are market rates published daily, so a different quote date can produce a different benchmark even when every other input stays the same. That is why revised payoff letters can move meaningfully over short periods.

The Treasury interest rate resource center updates rates on an ongoing basis using market data. For borrowers deciding whether to refinance or sell, this timing issue often overlaps with the analysis in Graphline’s page on yield maintenance refinance or sale.

Are CMBS loans different?

Often, yes. CMBS documents may define the benchmark and determination mechanics more rigidly, and servicer administration can add procedural timing requirements to the quote process. The benchmark itself may still be Treasury-based, but the documentation and servicing workflow are usually more formal.

That matters because a benchmark dispute that gets resolved informally on a balance-sheet loan may require servicer-level documentation on a securitized loan.

Frequently Asked Questions

Which Treasury rate is used for yield maintenance?

The rate used for yield maintenance is usually the U.S. Treasury yield named in the loan documents for a maturity comparable to the loan’s remaining term. Many documents use a constant maturity Treasury series, the nearest published Treasury tenor, or an interpolated Treasury yield. The note and mortgage control the selection.

How much can a small Treasury rate change affect a yield maintenance penalty?

On a multi-million-dollar CRE loan with several years remaining, a 10- to 25-basis-point move can change the penalty by tens of thousands of dollars. The exact effect depends on the balance, remaining amortization, note rate, spread, and whether the loan has a floor on the discount rate.

Where do I verify the Treasury yield used in a payoff statement?

You can verify the benchmark against the source named in the loan documents, often the U.S. Department of the Treasury daily par yield curve rates or a Federal Reserve rate publication. The audit should also confirm the quote date, remaining term, and any interpolation or spread added by the lender.

Do CMBS and balance-sheet lenders use the same Treasury benchmark method?

Not always. Both may use Treasury-based benchmarks, but CMBS documents and servicing agreements often define the method more tightly and impose more formal determination procedures. That can affect how the benchmark is selected, documented, and challenged.

Does Treasury rate selection vary by market or region?

The Treasury benchmark itself is national, so the underlying U.S. Treasury yield does not vary by region. What does vary by lender, loan program, or servicing platform is the document language governing selection, interpolation, spread, and floors. A New York office loan and a Texas industrial loan can end up with different benchmark mechanics if the note forms differ, even though the Treasury market data are the same.