CMBS Yield Maintenance: Rules, Lockouts, Defeasance

CMBS yield maintenance follows pooling and servicing agreements, loan documents, and securitization timelines that work differently from portfolio loans. This guide covers how master servicers handle payoff requests, when special servicing changes the process, how lockout periods apply, and why many CMBS loans move from yield maintenance to defeasance before maturity.

CMBS yield maintenance usually is not just a note-level prepayment formula. It sits inside a securitized servicing system with master servicer review, bondholder protections, and, in many loans, a point where defeasance replaces a simple cash payoff. That changes the real-world exit path. The timing, documents, and available options on a commercial mortgage-backed securities loan are often very different from what borrowers expect if they are used to portfolio debt. This article walks through how CMBS yield maintenance actually works, how the master servicer handles payoff requests, what lockouts really block, and when defeasance becomes the only workable way out before maturity.

Key Takeaways

- Many CMBS loans ban voluntary prepayment during an initial lockout period. After that, the note and servicing documents usually allow either yield maintenance or defeasance, not a free-form payoff.

- According to typical Pooling and Servicing Agreement provisions filed with the U.S. Securities and Exchange Commission, the master servicer handles routine borrower requests, while the special servicer usually steps in after defaults, imminent defaults, or specially serviced transfers.

- According to industry guidance on CMBS defeasance process timing, defeasance closings often take several weeks and require coordination among the servicer, counsel, securities broker, accountant, and sometimes rating agencies or other deal parties.

- Borrowers should review the note, loan agreement, and servicing notices early. The rules on lockout, notice periods, successor borrower requirements, and open-window prepayment are often scattered across multiple documents.

- On many securitized loans, a payoff request that looks simple at the property level turns into a document and timing exercise involving servicing fees, cutoff dates, reserve releases, and remittance-cycle constraints.

CMBS yield maintenance: what makes it different

CMBS yield maintenance is different from the version borrowers see in bank loans because the loan has usually been sold into a trust and is administered under a Pooling and Servicing Agreement, or PSA. So prepayment is not judged only under the note and loan agreement. It is also handled inside a servicing framework built to protect bond cash flow.

According to the U.S. Securities and Exchange Commission EDGAR database of CMBS servicing agreements and prospectus filings, securitized commercial loans are governed by deal-specific contracts that divide authority among the master servicer, special servicer, trustee, and other parties. In practice, that makes three issues much more important than they usually are on portfolio loans:

- Prepayment restrictions — many CMBS loans have hard lockouts, defeasance periods, or narrowly defined open windows.

- Servicing authority — borrowers do not work out payoff logistics directly with bond investors; requests move through servicing channels.

- Timing discipline — remittance dates, notice periods, securities purchases, and document review often decide whether a closing hits the target month or slides into the next cycle.

That is why borrowers comparing a sale, refinance, or assumption should treat CMBS as a servicing and document problem first, and a pricing problem second. People often do the reverse, and that is where deals get sideways. For broader context on how these clauses fit into the larger market, see this overview of commercial real estate yield maintenance.

A concise snippet answer for search: CMBS yield maintenance is a prepayment protection structure on securitized commercial mortgages that is administered through CMBS servicing rather than only by the originating lender. Depending on the loan documents, a borrower may face a lockout period, a yield maintenance charge, or a requirement to defease the loan instead of paying it off with cash before maturity.

How the master servicer handles a CMBS payoff request

The master servicer is usually the borrower’s first operational contact on a performing CMBS loan. For a routine payoff or prepayment inquiry, the master servicer typically controls notice requirements, document intake, payoff statement preparation, fee collection, and coordination with the trustee or certificate administrator.

According to Cornell Law School’s overview of securitization structures and transaction-specific CMBS PSAs filed on SEC EDGAR, the master servicer administers performing loans under the PSA, while specially serviced loans move to the special servicer. Borrowers often underestimate how formal this process is. A CMBS payoff request usually takes more than asking for a wire amount.

What the master servicer usually needs

A standard CMBS payoff package usually starts with written notice and a review of whether the requested prepayment date is even allowed under the loan documents. The servicer may also ask for counsel contact information, authority documents, a title company or closing agent contact, and fee deposits before issuing a final statement.

- Borrower identification and loan number

- Requested payoff or release date

- Confirmation that the loan is outside any lockout, or that the prepayment right has otherwise ripened

- Direction on whether the request is for a cash payoff, defeasance, assumption, or quote only

- Servicing or processing fee deposits if the documents allow them

In practice, the main delays usually are not about math. They come from missing notices, unresolved reserve balances, unclear signing authority among borrower affiliates, and closing dates that do not line up with remittance cutoffs.

Why payoff statements take longer on CMBS loans

CMBS payoff statements often take longer because the servicer is checking more than principal and interest. It may also need to confirm default interest status, servicing advances, escrow and reserve treatment, release conditions, and the exact prepayment premium mechanics. According to mortgage servicing compliance resources published by the Consumer Financial Protection Bureau, servicing accuracy and process controls are core servicing obligations generally. In CMBS, those controls sit on top of trust-specific requirements.

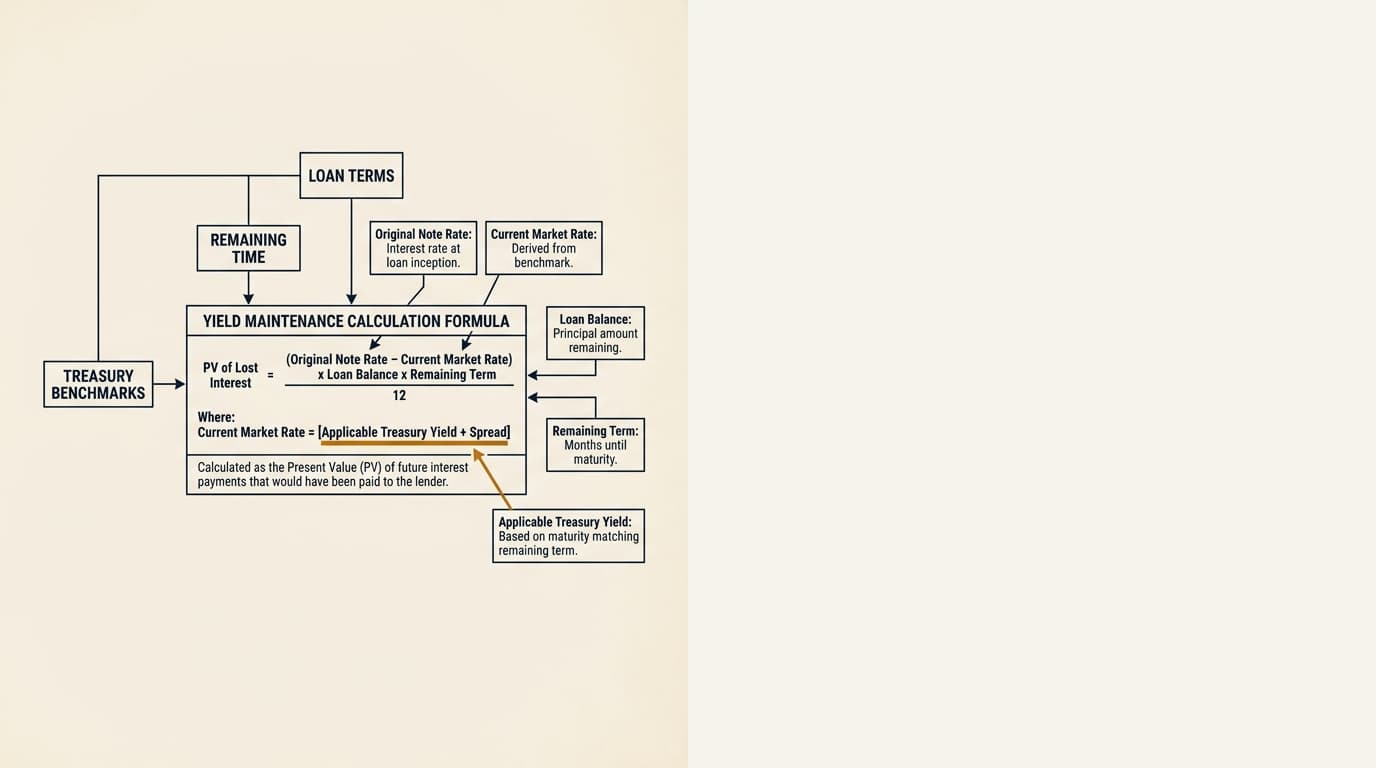

For borrowers, the practical point is simple: the “same-week payoff quote” many people expect from a bank lender often does not happen with securitized debt. If the loan calls for a more detailed economic calculation, this explainer on the yield maintenance formula covers the mechanics without repeating them here.

CMBS lockout periods and open windows

Most CMBS lockout periods are hard restrictions on voluntary prepayment for a stated period after origination. Once the lockout ends, the borrower still may be limited to yield maintenance, defeasance, or a narrow open period near maturity, depending on the note.

According to Federal Deposit Insurance Corporation materials on structured finance and securitization, structured products are built around expected cash-flow timing. Lockouts and similar prepayment protections help preserve those cash flows for bondholders. In CMBS lending, the distinctions that matter are usually these:

| Term | What it means in practice | Typical borrower impact |

|---|---|---|

| Lockout period | No voluntary prepayment for a stated period | Sale or refinance may be blocked unless the buyer assumes the debt or the deal waits |

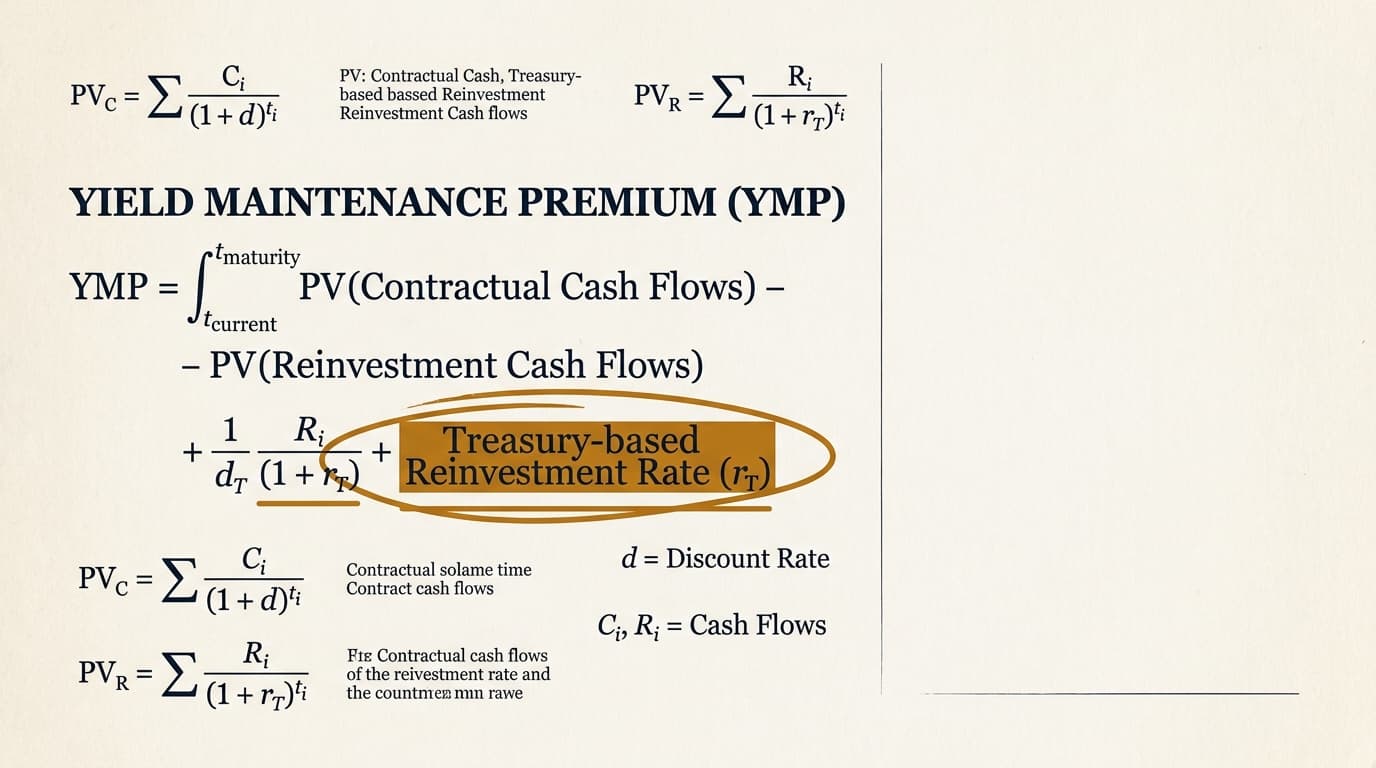

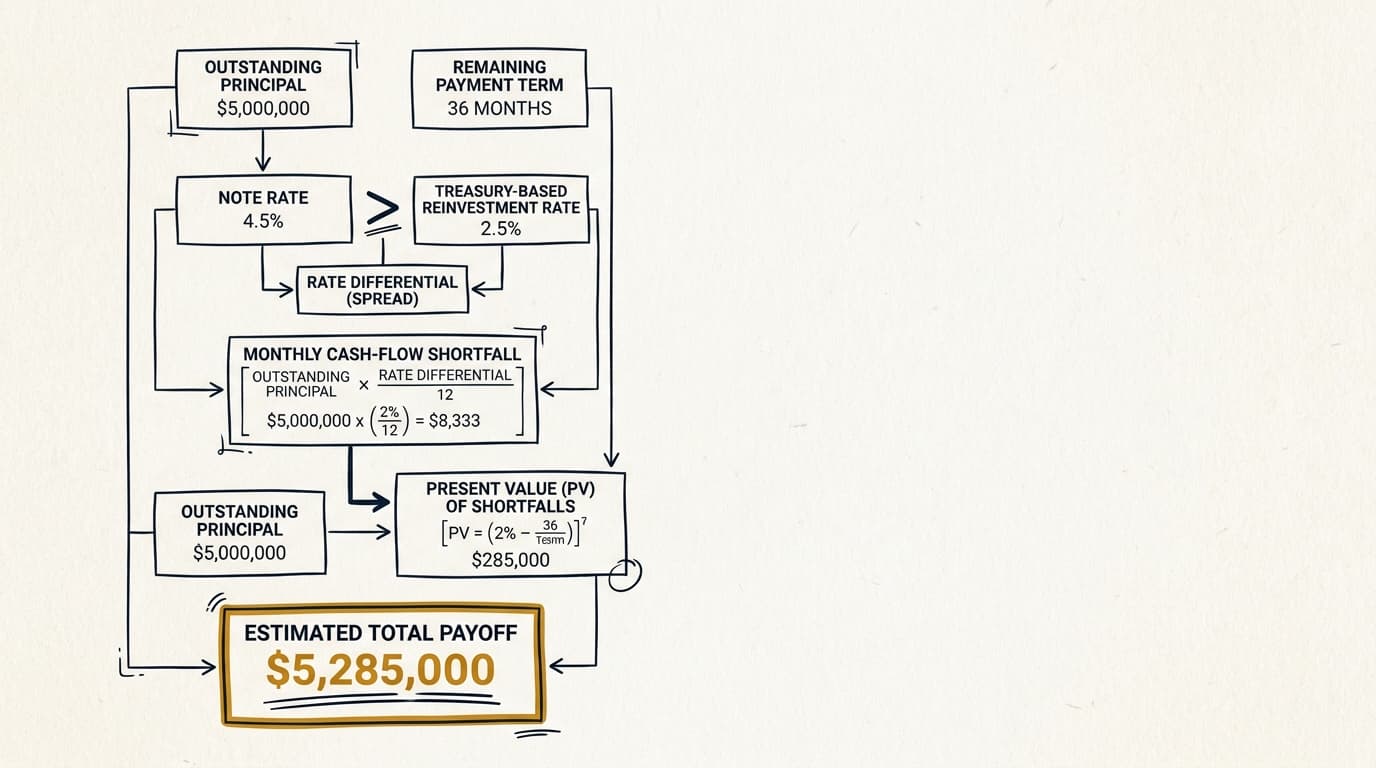

| Yield maintenance period | Cash prepayment may be allowed, but only with a premium tied to discounted scheduled interest | The penalty can be large when market rates are below the note rate |

| Defeasance period | Borrower substitutes government securities collateral instead of paying off the trust directly | Transaction cost includes securities purchase, consultant, legal, and servicing fees |

| Open window | Limited period near maturity when prepayment may be allowed without the earlier premium structure | Closing dates have to be timed carefully around notice provisions and the maturity schedule |

Loan documents vary a lot. Some CMBS loans go from lockout straight into defeasance-only prepayment. Others allow yield maintenance for a period and then open prepayment shortly before maturity. The controlling language is in the note, loan agreement, and securitization servicing notices. That is why a focused review of yield maintenance loan documents should happen before a sale process starts, not after a buyer is already at the table.

When defeasance replaces yield maintenance in CMBS

Many CMBS loans require defeasance instead of a direct cash payoff because substitute collateral preserves the trust’s scheduled payment stream more cleanly than prepayment does. Once the loan enters the defeasance period, the borrower may no longer have a contractual right to satisfy the debt by paying principal plus a yield maintenance premium.

According to U.S. Treasury published yield curve data, benchmark government rates move daily. In a traditional yield maintenance structure, those changes affect the premium because the lender compares the note coupon to a reinvestment rate. In defeasance, by contrast, the borrower buys a portfolio of U.S. government securities or agency obligations specified by the documents to replicate the remaining scheduled debt service. Same goal, very different mechanics. And usually a very different closing process.

Why CMBS trusts prefer defeasance

Defeasance preserves bond-level cash flow assumptions built into the securitization more cleanly. Instead of receiving principal back early and having to reinvest it, the trust keeps receiving scheduled payments from substitute collateral.

According to Internal Revenue Service Revenue Ruling 2004-20 on defeasance and REMIC considerations, defeasance structures are built around tax and securitization limits that matter in Real Estate Mortgage Investment Conduit transactions. That is one reason CMBS documents are often more rigid than bank or life company loan documents when it comes to how prepayment can happen.

What this means in practice for borrowers

The operational difference is real. A yield maintenance payoff is mostly a calculation and funding exercise. A defeasance closing is a multi-party securities transaction with separate counsel, a defeasance consultant, servicer review, and successor borrower mechanics.

That is why timing matters more than many sellers think. A borrower working under a purchase agreement with a 30-day closing target may find that defeasance is possible only if the process starts before PSA deadlines begin to squeeze the deal. For a side-by-side cost discussion without repeating that material here, see yield maintenance vs defeasance.

Special servicing scenarios that complicate payoff timing

A loan in special servicing follows a different path because the special servicer is focused on workout and recovery, not routine administration. Once a transfer event happens, even a borrower trying to refinance or sell on a cooperative basis may face slower approvals, added fees, and more servicer discretion.

According to special servicing provisions commonly reflected in SEC-filed CMBS servicing agreements, transfers to special servicing often follow payment defaults, maturity defaults, imminent default determinations, or major borrower requests outside ordinary master-servicing authority. In practice, four scenarios matter most:

- Maturity default — the loan reaches maturity before refinance proceeds are available, which shifts authority and often gives the special servicer more leverage.

- Imminent default designation — even before a missed payment, borrower distress can move the file to special servicing.

- Major consent requests — some assumptions, discounted payoffs, or significant collateral changes can require special-servicer involvement.

- Cash management or reserve disputes — unresolved questions about reserve use or sweeps can delay release figures and closing approvals.

The main issue in special servicing often is not the quoted payoff amount. It is the approvals, legal review, timing, and negotiation posture around the request.

What borrowers should review in CMBS loan documents

The answer on CMBS prepayment rights is in the documents, not in market shorthand. Borrowers should review the note, loan agreement, cash-management provisions, servicing transfer notices, and any assumption or defeasance rider before the property goes to market.

According to CMBS prospectus supplements and servicing exhibits available through SEC EDGAR, drafting varies by deal and vintage. The clauses that most often decide the outcome are:

- Absolute lockout language and its exact start and end dates

- Permitted prepayment method after lockout — cash payoff, yield maintenance, defeasance, or open-period payoff

- Notice requirements — often measured by days before a payment date, not days before the closing date

- Prepayment date conventions — some loans allow prepayment only on scheduled payment dates

- Assumption provisions — important when a sale is possible but payoff is too expensive

- Successor borrower requirements in a defeasance transaction

- Release of reserves and escrows — whether they reduce the payoff at closing or come back later

A common mistake in sale processes is reading only the section labeled “prepayment” and missing related limits in assumption, reserve, transfer, or cash management provisions. The dedicated page on yield maintenance loan documents covers where those clauses often show up.

CMBS payoff timeline: a practical step-by-step process

A CMBS payoff usually goes more smoothly when borrowers start 30 to 60 days before the target closing date, and earlier if defeasance is likely. The timeline is driven less by property-closing habits and more by servicing deadlines, notice periods, and third-party coordination.

- Review the note, loan agreement, and servicing correspondence to confirm whether the loan is in lockout, yield maintenance, or defeasance period.

- Request written guidance from the master servicer on notice requirements, fees, and the permitted prepayment method.

- Engage counsel and, if defeasance is required, retain a defeasance consultant and securities intermediary early.

- Match the property sale or refinance closing date to the loan’s permitted prepayment date and remittance cycle.

- Order a draft payoff or defeasance quote with reserve, escrow, servicing fee, and per diem detail.

- Verify whether any default interest, protective advances, or unresolved reserve items must be cleared before closing.

- Circulate signature authority documents, entity certificates, and successor borrower materials before final documents are issued.

- Confirm final wires and cutoff times with the servicer, trustee, closing agent, and all transaction counterparties.

That sequence may sound procedural, but it has real strategic value. If the documents show a near-term open window, waiting may be cheaper than forcing a defeasance. If the open window is too far off, assumption or a repriced sale may be more realistic than trying to rush a refinance. Borrowers sizing up the economics in context should also review yield maintenance refinance or sale.

Decision framework: sale, refinance, assumption, or defeasance

The best exit route depends on timing, the rate environment, the buyer profile, and the exact CMBS document set. In practice, the lowest headline penalty is not always the lowest all-in cost.

The table below sums up how advisors usually compare the main options on a securitized loan:

| Scenario | Best-fit option | Why it may work | Main constraints |

|---|---|---|---|

| Property sale during absolute lockout | Assumption or delayed closing | A buyer may keep the existing debt in place if the assumption terms work | Assumption approval, assumption fees, buyer underwriting, transfer tests |

| Sale after lockout but in defeasance period | Defeasance | Often the only permitted way to release the real estate collateral | Securities cost, legal complexity, longer lead time |

| Refinance near open window | Wait for open prepayment period | Can avoid the earlier premium structure if the timing is close | Rate-lock risk, extension risk on the new financing |

| Loan under performance stress | Negotiated resolution with special servicer | May allow an extension, modification, or discounted resolution in limited cases | Special servicing fees, slower approvals, no assurance of consent |

| Falling-rate market with cash payoff still allowed | Model yield maintenance carefully | The penalty may be higher than expected because the reinvestment benchmark is lower | Premium volatility until the quote date |

This is where CMBS analysis gets more specific than a generic penalty discussion. A borrower deciding between a sale and a refinance should compare more than the prepayment cost. Legal fees, servicing fees, defeasance expenses, reserve-release timing, buyer tolerance for assumption, and whether a one-month delay blows up the business plan all matter. The article on yield maintenance vs step-down is a useful contrast because many borrowers come into CMBS expecting more flexibility than securitized loans usually offer.

One edge case deserves real attention: if a sale contract gets signed before counsel confirms that the loan is actually defeasance-only, the seller may underwrite the wrong net proceeds by several hundred thousand dollars or more on a larger balance. That shortfall usually does not come from one hidden fee. It comes from the pileup of substitute collateral pricing, advisory fees, legal review, servicer fees, and timeline slippage into the next payment cycle.

Frequently Asked Questions

Can a CMBS loan be prepaid with cash instead of defeasance?

Some CMBS loans allow cash prepayment with a yield maintenance premium after lockout, but many require defeasance for most of the remaining term. The answer is in the note and loan agreement. According to SEC-filed CMBS transaction documents, prepayment rights vary by deal, so borrowers should confirm the exact language before signing a sale contract or refinancing term sheet.

How long does a CMBS payoff or defeasance usually take?

A routine cash payoff on a performing CMBS loan can move fairly quickly if the documents allow it and notice has already been given. Defeasance usually takes longer because it requires securities purchases, legal documents, and servicer coordination. According to industry process guidance for CMBS defeasance, several weeks is a reasonable planning assumption, and tighter timelines usually work only with early coordination.

What happens if the loan has transferred to special servicing?

Once a CMBS loan is in special servicing, borrower requests are no longer handled as routine master-servicer administration. Approval timing, fees, and available resolutions can change materially. According to special servicing authority provisions in CMBS servicing agreements, the special servicer generally has broader discretion over workouts, modifications, and certain payoff-related requests.

Is CMBS yield maintenance the same in New York, Texas, or California?

The core economics are usually driven by the loan documents and securitization structure, not by the property location. But local counsel, transfer taxes, recording requirements, and closing customs can still change timing and total cost. Legal and closing logistics in New York may differ from Texas or California even when the CMBS prepayment language is identical. Borrowers should coordinate early with state-specific counsel and the servicer when a defeasance or assumption is tied to a property sale.

Where should borrowers look first to confirm whether yield maintenance applies?

Start with the promissory note, loan agreement, and any defeasance rider or servicing transfer notice. The prepayment section alone may not be enough because notice timing, open-window rules, and reserve treatment often appear elsewhere. This guide to yield maintenance prepayment penalty can help frame what the quoted figures are meant to capture once the governing provisions are confirmed.