Yield Maintenance Loan Documents: What Controls Payoff

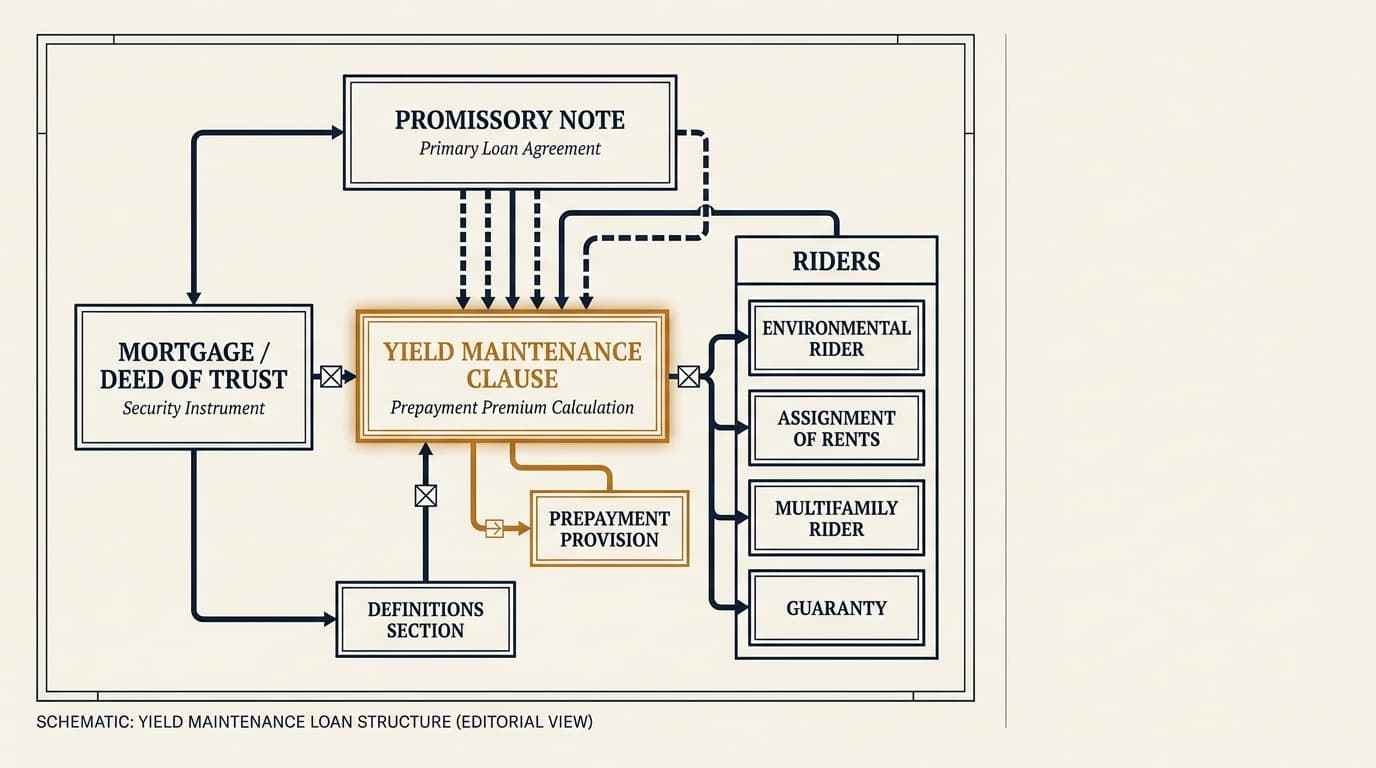

Yield maintenance usually isn’t controlled by a single clause. In most commercial real estate loans, the payoff terms are spread across the promissory note, mortgage or deed of trust, the definitions section, and any riders that change prepayment rights, Treasury selection, or notice requirements.

Most commercial real estate loans do not put yield maintenance in one neat clause. The real rule usually sits across the note, the security instrument, the definitions section, and one or more riders. That matters because the payoff can swing on a small drafting choice, like whether the comparison rate uses a U.S. Treasury spot rate, an interpolated yield, or a fixed spread over a Treasury security.

This article shows where yield maintenance language usually lives, which definitions control when provisions collide, and which restrictions borrowers and counsel should catch before signing. The focus here is document review, not payoff math. For the broader picture of commercial real estate yield maintenance, the pillar page covers the bigger structural and timing issues.

Key Takeaways

- In most CRE loans, the operative yield maintenance terms are spread across several documents, not just the promissory note.

- The payoff amount usually depends on defined terms like "Treasury Rate," "Reinvestment Yield," "Prepayment Premium," "Stated Maturity Date," and "Prepayment Date."

- Riders and addenda often override standard note language, especially on open periods, notice windows, and minimum premium floors.

- Term sheets often leave out restrictions that later appear in draft loan documents, including lockout carve-outs, affiliate transfer limits, and notice timing.

- A sound review means tracing cross-references section by section and confirming which document has priority if the provisions do not match.

Yield maintenance loan documents: the short answer

Yield maintenance loan documents include the promissory note, loan agreement, mortgage or deed of trust, guaranty package where relevant, and any riders or addenda that define prepayment rights and premium calculations. In practice, the payoff language usually starts in the note and then gets reshaped by definitions, riders, securitization language, or a separate prepayment provision in the loan agreement.

According to the Federal Deposit Insurance Corporation examination guidance on prepayment penalties, enforceability and disclosure turn on the actual contract terms, not just the label. In commercial lending, that point matters because two loans can both be called "yield maintenance" and still produce very different payoff numbers based on benchmark selection, floor language, and timing mechanics.

Where yield maintenance appears in loan documents

Most yield maintenance provisions put the payment obligation in the note, then scatter the triggers, conditions, and exceptions elsewhere in the stack. If a borrower reads only the note, there is a good chance they miss a definition or rider that adds cost or cuts back prepayment rights.

A typical document stack splits the clause this way:

| Document | What it usually controls | Why it matters |

|---|---|---|

| Promissory note | Core prepayment provision, premium obligation, maturity references | Usually states that voluntary or involuntary prepayment requires principal plus yield maintenance or a defined premium |

| Loan agreement | Conditions to prepayment, notices, application of payments, casualty or condemnation exceptions | May narrow when prepayment is actually permitted |

| Mortgage or deed of trust | Remedies, acceleration, treatment after default, lien-level enforcement | Can determine whether premium survives acceleration or foreclosure-related events |

| Rider or addendum | Overrides to standard forms, open periods, Treasury definitions, minimum premium floors | Often contains the changes borrowers care about most |

| Term sheet or commitment letter | Business summary of lockout, open period, and premium concept | Useful as a negotiation baseline, but usually less detailed than final documents |

According to the Consumer Financial Protection Bureau Regulation Z materials, prepayment treatment depends on the contractual method stated in the governing instrument. Regulation Z is mostly aimed at consumer lending, not institutional CRE finance, but the contract-reading point still carries over: defined terms and incorporated provisions drive the outcome.

The promissory note usually holds the obligation

The promissory note usually states the borrower's obligation to pay principal, accrued interest, and any prepayment premium or yield maintenance amount. If counsel needs one place to start, this is usually it.

In many fixed-rate CRE notes, the prepayment section does four things: it sets a lockout or restricted period, says whether voluntary prepayment is allowed, defines or cross-references the premium, and lists any open-period exception near maturity. The note may also say whether partial prepayment is prohibited, allowed only above a threshold, or treated as a full prepayment for premium purposes.

The loan agreement usually holds the conditions

The loan agreement often controls the mechanics around what looks like a simple note clause. It may specify notice periods, approved prepayment dates, break-funding language, release conditions, reserve true-ups, and whether exit is allowed after transfers, casualty proceeds, or condemnation awards.

This is where borrowers often find restrictions that the term sheet only hinted at. A term sheet may say "open to prepay in the last 90 days," but the loan agreement may require 30 days' prior notice, payment only on a scheduled interest payment date, and delivery of reserve shortfall funds before the servicer will issue a final payoff quote.

The rider often contains the real edits

Riders often control because lenders use them to modify standard forms without rewriting the note from scratch. In an actual dispute, a specific rider provision often beats a general note clause.

Borrowers should expect riders to address Treasury selection, interpolation methodology, spread adjustments, floors, lockout exceptions, and rights tied to assumption or affiliate transfers. If the rider says "notwithstanding anything to the contrary," pay attention. That is usually the drafter's way of saying this language overrides the boilerplate elsewhere.

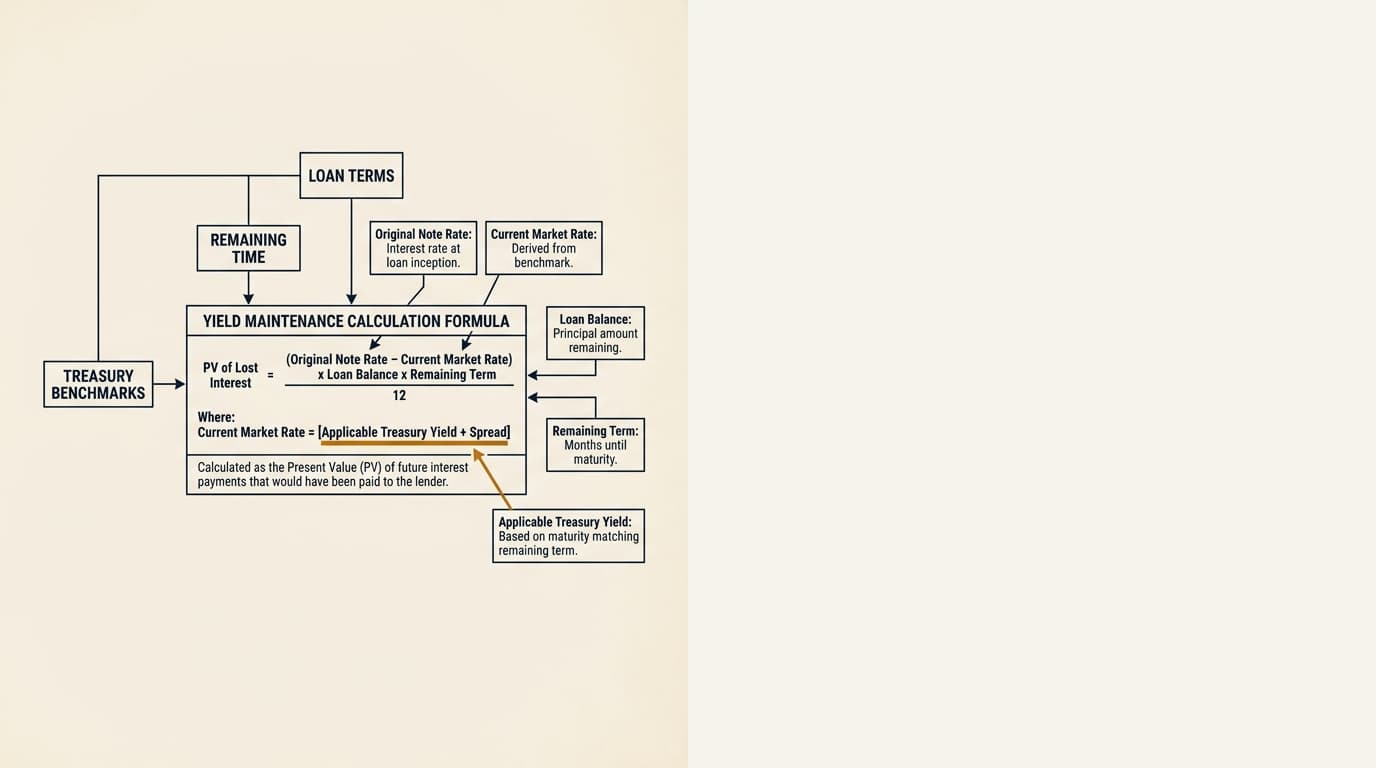

Which definition actually controls the payoff amount

The payoff amount usually depends less on the label "yield maintenance" and more on the defined terms inside the formula. A small shift in one definition can change the premium by tens or hundreds of thousands of dollars on a large loan.

The definitions to isolate first are:

- Prepayment Premium or Yield Maintenance Premium

- Treasury Rate, Reinvestment Rate, or Applicable Treasury Yield

- Prepayment Date

- Stated Maturity Date

- Outstanding Principal Balance

- Scheduled Payments or Remaining Monthly Payments

- Interest Differential or similar present-value concept

According to the U.S. Department of the Treasury daily Treasury par yield curve rates, Treasury benchmarks are published at standard maturities, but commercial loan documents often call for an adjusted or interpolated maturity that does not line up exactly with a published point. That is why the definition matters more than a loose reference to "Treasuries." For a document-specific explanation of how benchmark drafting changes the math, see the separate article on the yield maintenance formula.

Defined terms beat shorthand descriptions

A term sheet summary like "yield maintenance to Treasury plus 50 basis points" is not enough to predict the payoff. The actual premium depends on how the final documents define the Treasury security, the remaining term, whether interpolation is allowed, and whether a floor applies.

Take two notes with the same coupon and principal balance. One defines the comparison rate as the yield on the Treasury security maturing closest to the remaining loan term, plus 50 basis points, with a zero floor. The other uses an interpolated Treasury rate plus 25 basis points, but also imposes a minimum premium equal to 1% of principal. Both may be sold as yield maintenance loans. Economically, they are not the same loan.

Conflict clauses decide which document wins

When note language and rider language do not match, the answer usually comes from a conflict clause or from ordinary contract interpretation that favors the more specific, later-added provision. Do not assume the note controls just because the premium appears there first.

Look for language like "in the event of any conflict, this rider shall control" or "the provisions of the loan agreement shall supersede inconsistent provisions in the note." Miss that step, and a borrower can lean on a favorable note clause that has already been cut back somewhere else.

Promissory note vs. loan agreement vs. rider: what each document usually does

Each document in the stack has a different job. Reading them as if they all say the same thing is the fastest way to miss a buried prepayment restriction.

| Issue | Promissory note | Loan agreement | Rider/addendum |

|---|---|---|---|

| Whether prepayment is allowed | Usually yes, subject to conditions | Often adds procedural conditions | May narrow or expand exceptions |

| How premium is named | Usually defined here | Sometimes cross-referenced | May restate with edits |

| Treasury benchmark selection | Sometimes general | Less common | Common place for detailed edits |

| Notice requirements | Basic notice | Detailed timing and delivery mechanics | May add servicer-specific rules |

| Open period before maturity | May mention | May condition on no default | Often revised here |

| Premium after default or acceleration | Sometimes ambiguous | May address remedies | Can expressly preserve premium |

This split is one reason document review matters more than lender shorthand in a term sheet. A borrower comparing structures should also understand how other prepayment provisions work in practice. The related discussion of yield maintenance vs step-down helps frame those differences, but it does not replace a line-by-line review of the documents in front of you.

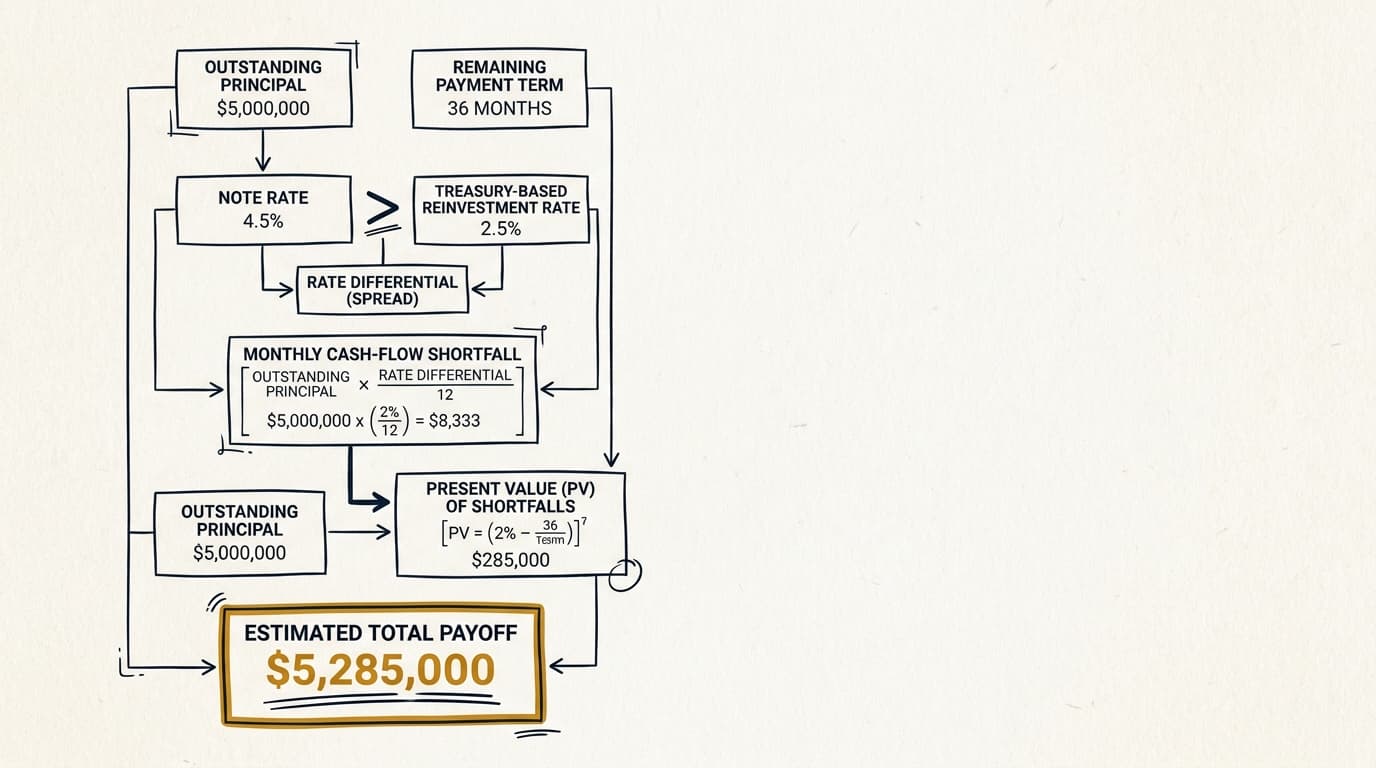

The five document terms that change the number most

Five drafting choices usually move the final payoff number the most: benchmark definition, spread, floor, payment schedule assumption, and timing mechanics.

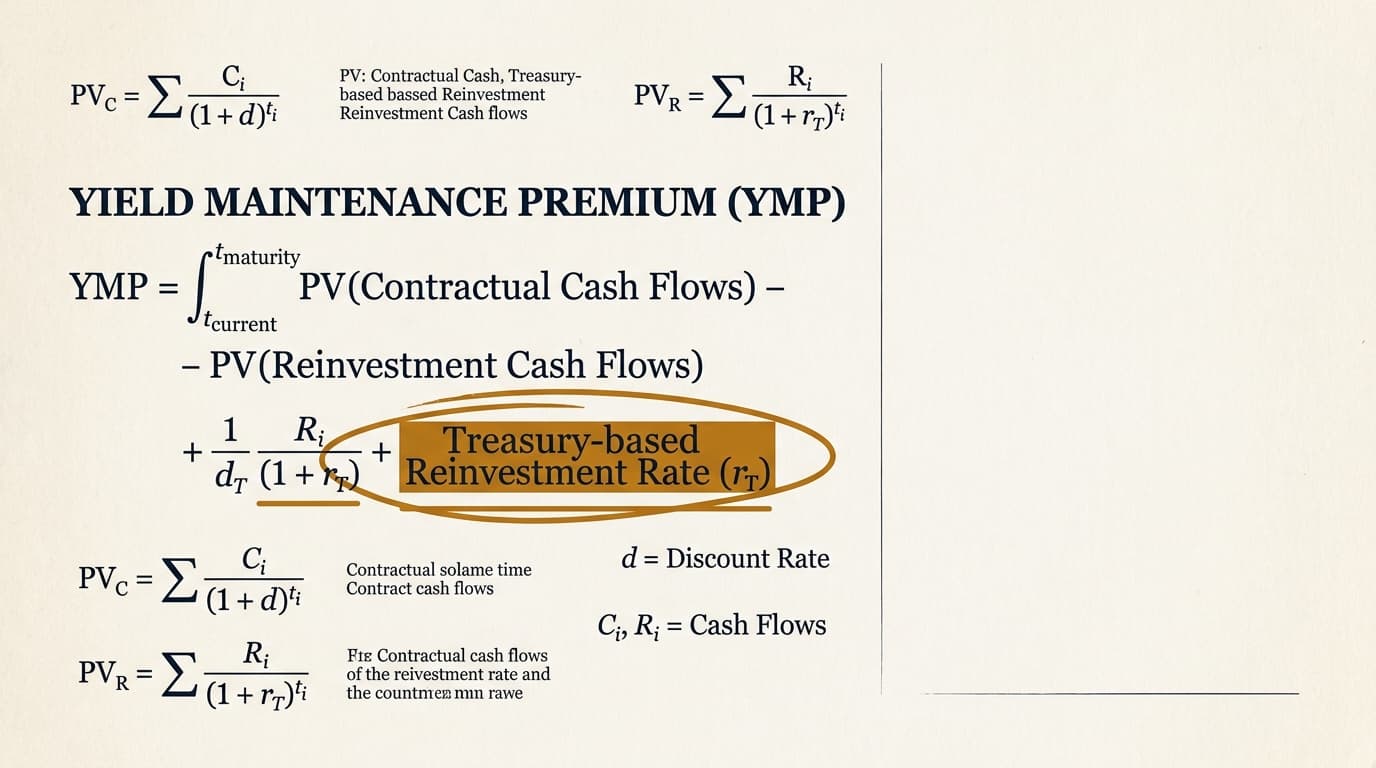

1. Treasury benchmark definition

The benchmark may be the yield on a specific Treasury security, a Treasury constant maturity, an interpolated Treasury rate, or another lender-defined reinvestment rate. Each approach can produce a different discount rate and a different premium.

According to the U.S. Treasury interest rate statistics resources, published Treasury data includes standard maturity points, not every possible remaining loan term. If the document requires interpolation, the servicer or lender has less room to improvise than if the document allows selection of the "closest" maturity without further detail.

2. Spread over Treasury

The added spread may be 0 basis points, 25 basis points, 50 basis points, or another negotiated number. A higher spread usually reduces the premium because it raises the discount rate used in the present-value calculation.

This point is often buried in the definitions instead of stated cleanly in the term sheet. Experienced counsel usually checks it early, because it can materially change the economics.

3. Minimum premium floor

Many loan documents include a floor, such as 1% of principal or the greater of the formula amount and a fixed minimum. Floors matter most when rates rise and the pure formula would otherwise produce a low premium or none at all.

Borrowers miss floors all the time because they tend to appear at the end of the definition, after the dense present-value language. But that last sentence may matter more than the rest of the formula.

4. Scheduled payment assumption

The premium may be based on the present value of remaining scheduled monthly payments, monthly interest-only installments, or some other payment stream defined in the note. Interest-only periods, amortization start dates, and balloon structures all change the stream being discounted.

A loan with 24 months of interest-only payments followed by amortization can produce a very different premium path from a fully amortizing loan with the same rate and maturity. The documents need to say exactly which stream applies.

5. Prepayment date and notice timing

The effective prepayment date may be the date funds are received, the next scheduled payment date after notice, or another date the documents specify. A 30-day notice requirement can change the remaining term used in the calculation and, in turn, the premium.

If you are reviewing an actual payoff quote, compare the quote to the contract language and the notice that was already delivered. This is not a minor back-office issue. The separate article on a yield maintenance prepayment penalty walks through how these mechanics show up in real payoff practice.

Hidden restrictions borrowers miss in term sheets

Term sheets often capture the economic concept and skip the operational restrictions that show up later in the documents. That gap is common. It is also where borrowers get surprised.

The restrictions borrowers most often miss include:

- No partial prepayments except from specified casualty or condemnation proceeds

- Prepayment only on a payment date, not any business day

- Advance written notice of 15, 30, or even 60 days

- No open-period right while a default exists, even a minor reporting default

- Servicer or lender fee reimbursement for counsel, calculation agents, or rating agency review in securitized structures

- Affiliate transfer restrictions that block indirect exits without lender consent

- Assumption carve-outs that are narrower than the business team described

A common example: a borrower sees "open prepayment during final 90 days" in the commitment letter and assumes a sale can close at any point in that window. The final documents allow prepayment only on the first day of a month, require 30 days' prior notice, and suspend the right if reserve deposits or financial reporting are outstanding. The summary was not exactly wrong. It just was not enough.

That kind of drafting gap is also why CMBS borrowers compare exit structures early. For context on that choice, see the separate analysis of yield maintenance vs defeasance.

A practical review checklist before signing

A good review starts with document mapping, not formula modeling. The goal is to find every clause that affects whether prepayment is allowed, when it becomes effective, and how the premium is calculated.

- Locate every reference to prepayment, yield maintenance, prepayment premium, Treasury rate, reinvestment rate, and maturity in the full draft package.

- Build a one-page term map showing which document contains the obligation, the formula, the benchmark definition, the notice rule, and the open-period exception.

- Check whether any rider or addendum says it overrides inconsistent note or loan agreement language.

- Confirm whether partial prepayment is prohibited, restricted, or treated as a full prepayment for premium purposes.

- Verify the benchmark definition line by line, including interpolation, spread, and any minimum premium floor.

- Review whether prepayment is available only on scheduled payment dates and whether notice changes the effective payoff date.

- Test default-related limits, including whether minor covenant defaults suspend open-period rights.

- Compare the signed term sheet against the final documents and mark any new conditions that were not disclosed earlier.

- Ask for a worked sample payoff under the draft language before closing, especially on larger fixed-rate loans.

This checklist does not replace legal review. It does give borrowers and in-house teams a practical way to spot the provisions most likely to affect an eventual exit.

Edge cases that change interpretation

Some edge cases change how yield maintenance provisions work even when the core clause looks straightforward. These scenarios rarely show up in marketing summaries, but they matter when the loan is in trouble or the borrower is trying to get out.

Acceleration after default

Some jurisdictions and some document forms treat a prepayment premium differently after acceleration unless the documents expressly preserve it as liquidated damages or as an amount due upon any redemption before a stated date. This issue is heavily state-specific, and the exact wording matters.

Borrowers and counsel should review governing law, remedy provisions, and any language stating that the premium remains due after acceleration, foreclosure action, or lender election of remedies. According to the Legal Information Institute explanation of liquidated damages doctrine, enforceability often depends on whether the amount is framed as a reasonable estimate of damages rather than a penalty.

Casualty and condemnation proceeds

Loan agreements sometimes say that applying casualty or condemnation proceeds to principal is not a voluntary prepayment, while other forms still impose a premium unless restoration conditions are satisfied. You have to read the documents together.

This comes up often because the mortgage may discuss restoration and application of proceeds, while the note separately defines what counts as a prepayment event.

Affiliate transfers and assumptions

Some borrowers assume that a property sale to an affiliate or a permitted transfer avoids the economics of a prepayment. In many CRE documents, that is true only if the lender approves an assumption under tight conditions.

If the assumption path is narrow or discretionary, the practical result may be a blocked sale unless the premium is paid. That issue should be identified before signing, not when the property is already under contract.

Frequently Asked Questions

Where is yield maintenance usually located in loan documents?

Yield maintenance is usually stated in the promissory note, then modified or conditioned by the loan agreement, mortgage or deed of trust, and any prepayment rider or addendum. The controlling language often depends on cross-referenced definitions and conflict clauses, not one standalone paragraph.

Does the promissory note always control the payoff premium?

No. A rider, addendum, or loan agreement can override the note if the documents say that the specific or later-added provision controls. Borrowers should check for "notwithstanding" language and any clause stating which document governs if the terms are inconsistent.

What definitions matter most in yield maintenance loan documents?

The key definitions are usually Prepayment Premium, Yield Maintenance Premium, Treasury Rate or Reinvestment Rate, Stated Maturity Date, Prepayment Date, Outstanding Principal Balance, and Remaining Scheduled Payments. A small change in any of those terms can materially change the payoff amount.

Can yield maintenance terms vary by state or governing law?

Yes. The drafting may look similar across markets, but enforceability of prepayment premiums after acceleration, default, or certain remedies can vary by governing law and by the exact contract wording. Counsel should review both the loan documents and the law named in the governing-law clause.

What should borrowers compare between a term sheet and final documents?

Borrowers should compare lockout periods, open-period rights, notice requirements, Treasury benchmark definitions, premium floors, partial prepayment restrictions, assumption language, and default-related limits. Final documents often add operational conditions that do not appear in the term sheet summary.