Commercial Real Estate Yield Maintenance Guide 2026

Yield maintenance is a commercial real estate prepayment clause that compensates the lender if a loan is paid off before maturity. In practice, the cost turns on the loan rate, time remaining, the Treasury benchmark in the formula, and the exact wording of the note and rider.

Commercial real estate yield maintenance can turn an early loan payoff into a very expensive decision. On some fixed-rate loans, the prepayment charge runs into six or seven figures. Freddie Mac’s Multifamily Seller/Servicer Guide Section 8403.1 and its multifamily borrower prepayment resources make the broader point clearly: many multifamily loans do not allow a simple early payoff at par. Instead, they use defeasance, yield maintenance, lockouts, or some mix of the three. This article breaks down how yield maintenance works, when it applies, how lenders and servicers calculate it, and how it stacks up against defeasance and step-down provisions in sale, refinance, and early payoff decisions.

The details matter in 2026 because the same loan can produce very different exit costs depending on Treasury rates, time left on the note, servicing rules, and the actual loan language. If you are looking at a sale or refinance, you need to know which documents control, which inputs move the number, and where the real decision points sit.

Key Takeaways

- Yield maintenance is meant to compensate a lender for reinvestment loss when a fixed-rate CRE loan is prepaid before maturity. In many cases, that means discounting the remaining interest shortfall to present value using a Treasury-based rate.

- The biggest drivers of a commercial real estate yield maintenance charge are the loan coupon, the spread over the Treasury benchmark, and the number of months left until open prepayment or maturity.

- The loan documents decide the outcome. The note, prepayment rider, and servicing notices determine whether the provision is yield maintenance, defeasance, step-down, lockout, assumption, or some combination.

- In a falling-rate environment, yield maintenance charges usually rise because the lender’s reinvestment rate falls. In a rising-rate environment, the charge may shrink, subject to any minimum penalty.

- For securitized debt, process matters almost as much as economics. cmbs yield maintenance often comes with servicer timelines, notice periods, and document requirements that affect closing schedules.

Commercial Real Estate Yield Maintenance: What It Means in Practice

Yield maintenance is a contractual prepayment formula meant to leave the lender economically indifferent to an early payoff, or at least close to it. In most CRE loans, that means the borrower pays outstanding principal, accrued interest, and a prepayment amount tied to the gap between the loan rate and a Treasury-based reinvestment rate over the remaining term.

Agency and securitized loan programs regularly use structured prepayment provisions instead of flat fees. Fannie Mae’s guidance on defeasance and yield maintenance concepts explains the core idea: the provision protects the noteholder’s expected yield when rates fall and the borrower wants to refinance or sell before maturity. In the market, you see this most often in fixed-rate permanent loans, especially larger multifamily, office, retail, industrial, hospitality, and CMBS deals.

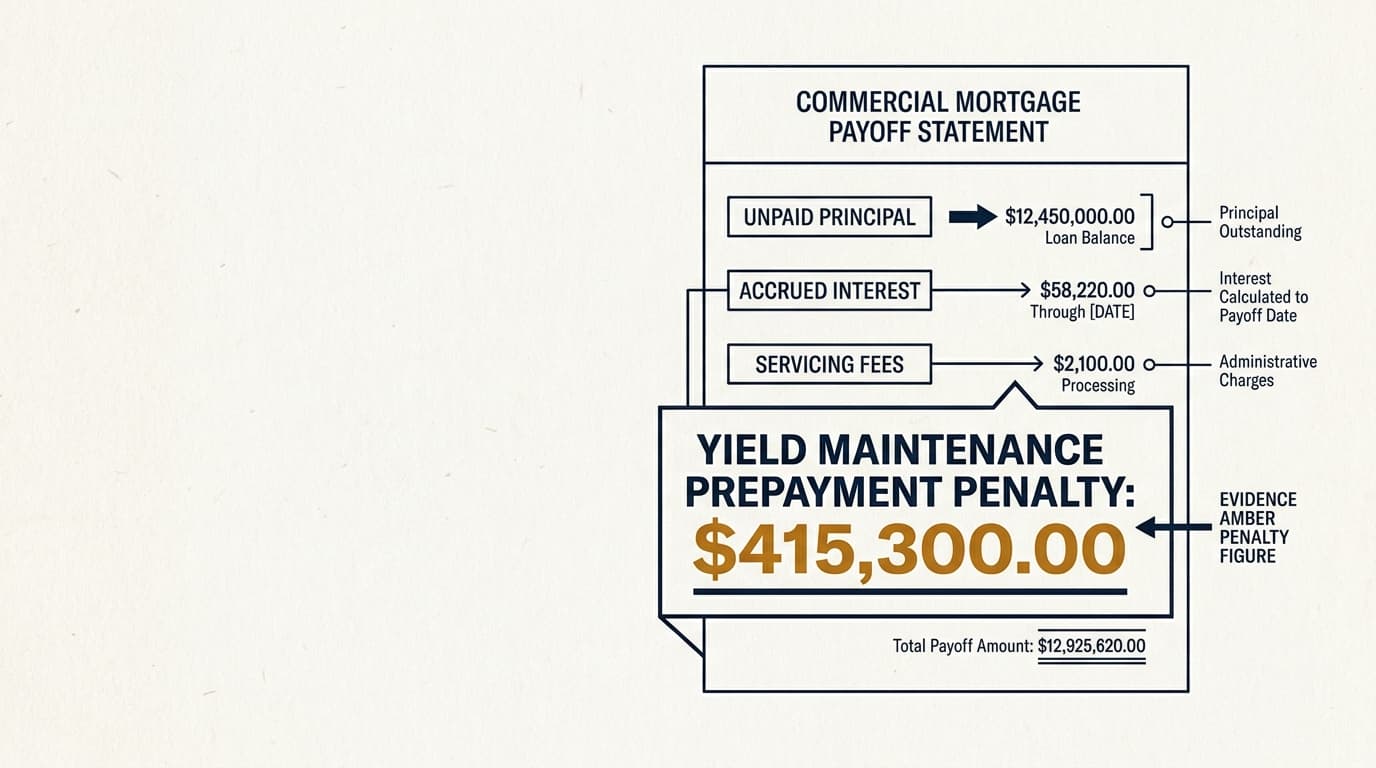

Put plainly: commercial real estate yield maintenance is a prepayment charge on a CRE loan that compensates the lender for losing above-market interest income when the loan is repaid early. The cost usually turns on the unpaid principal balance, the remaining scheduled payments, the contract rate, a Treasury benchmark, and the exact formula in the loan documents.

The logic is simple enough. If a lender expected to receive 5.75% for another 48 months and can now reinvest only at a Treasury-based rate closer to 3.75%, early payoff costs the lender money. Yield maintenance pushes that cost back to the borrower, subject to the formula and any floor.

For a clause-level review, the most useful next page is yield maintenance loan documents, which looks at the defined terms and rider language that usually decide the result.

When Yield Maintenance Applies Before Maturity

Yield maintenance usually applies when a borrower wants to retire a fixed-rate loan before the note allows open prepayment at par. Whether it applies in a refinance, sale, recapitalization, condemnation, casualty, or assumption depends on the loan documents and, sometimes, on how the servicer reads them.

Commercial mortgage documents often split the loan term into separate periods: a lockout, then a yield maintenance or defeasance period, then an open or reduced-penalty period near maturity. Freddie Mac’s Multifamily Seller/Servicer Guide Section 8403.1 says what many borrowers learn late in the process: these loans often are not freely prepayable during the term. They follow the structure in the documents. So if payoff timing matters, confirm the exact burn-off date. Do not assume that “close to maturity” means “cheap to exit.”

Common trigger events

Yield maintenance usually matters when a transaction requires a full or partial payoff before maturity. The trigger is not the market event by itself. It is the contractual prepayment caused by that event.

- Sale of the property where the buyer does not assume the existing debt

- Refinance into lower-rate or higher-leverage debt

- Portfolio recapitalization that requires retiring the debt

- Partial release or condemnation in loans that treat principal curtailment as a prepayment event

- Borrower-requested early payoff after a lockout period

When it may not apply

Yield maintenance does not apply in every early exit. Some loans permit assumption. Some switch to step-down prepayment late in the term. Some CMBS structures move to defeasance instead of yield maintenance.

Borrowers looking at timing should review yield maintenance before maturity for a focused discussion of burn-off dates, open periods, and timing exceptions. Sale transactions should also look at yield maintenance assumption sale, because assumption can change the economics a lot if the buyer qualifies and the servicer consents.

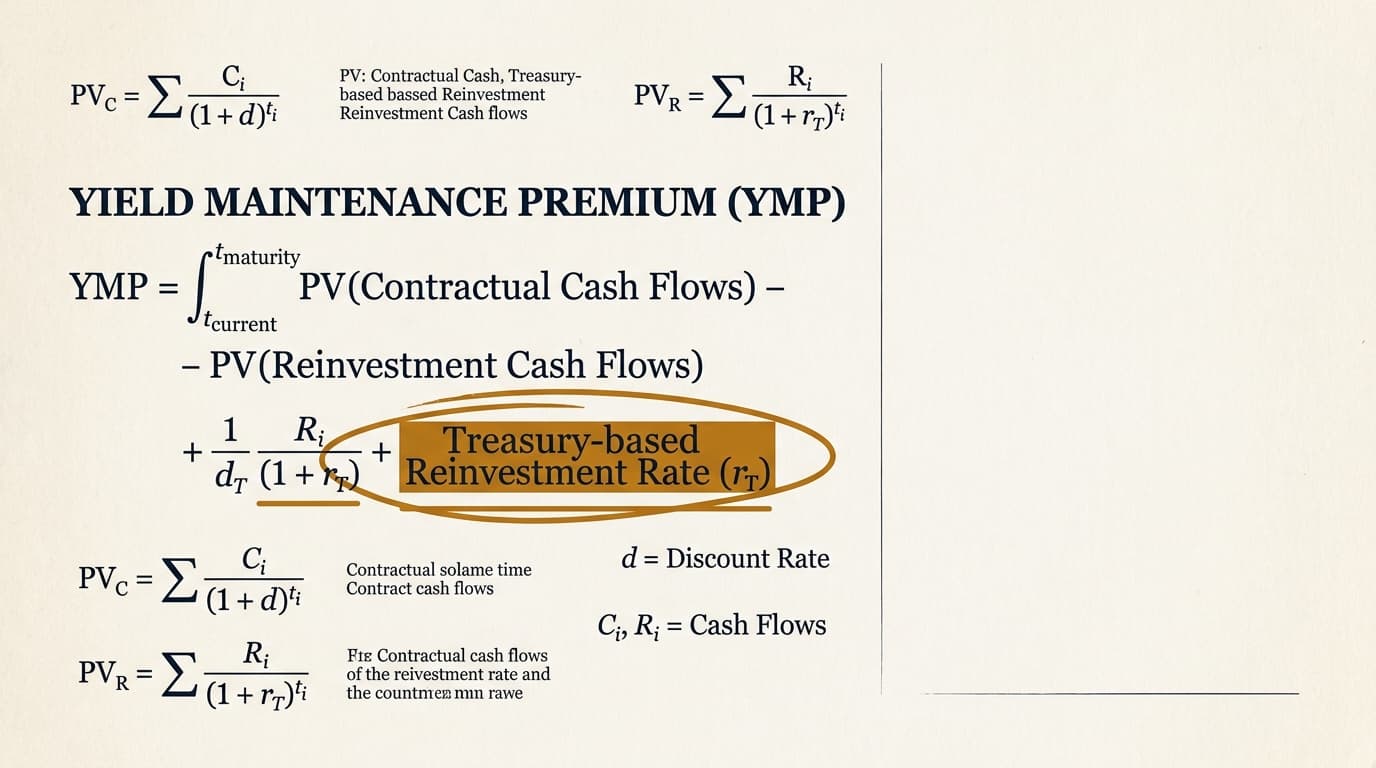

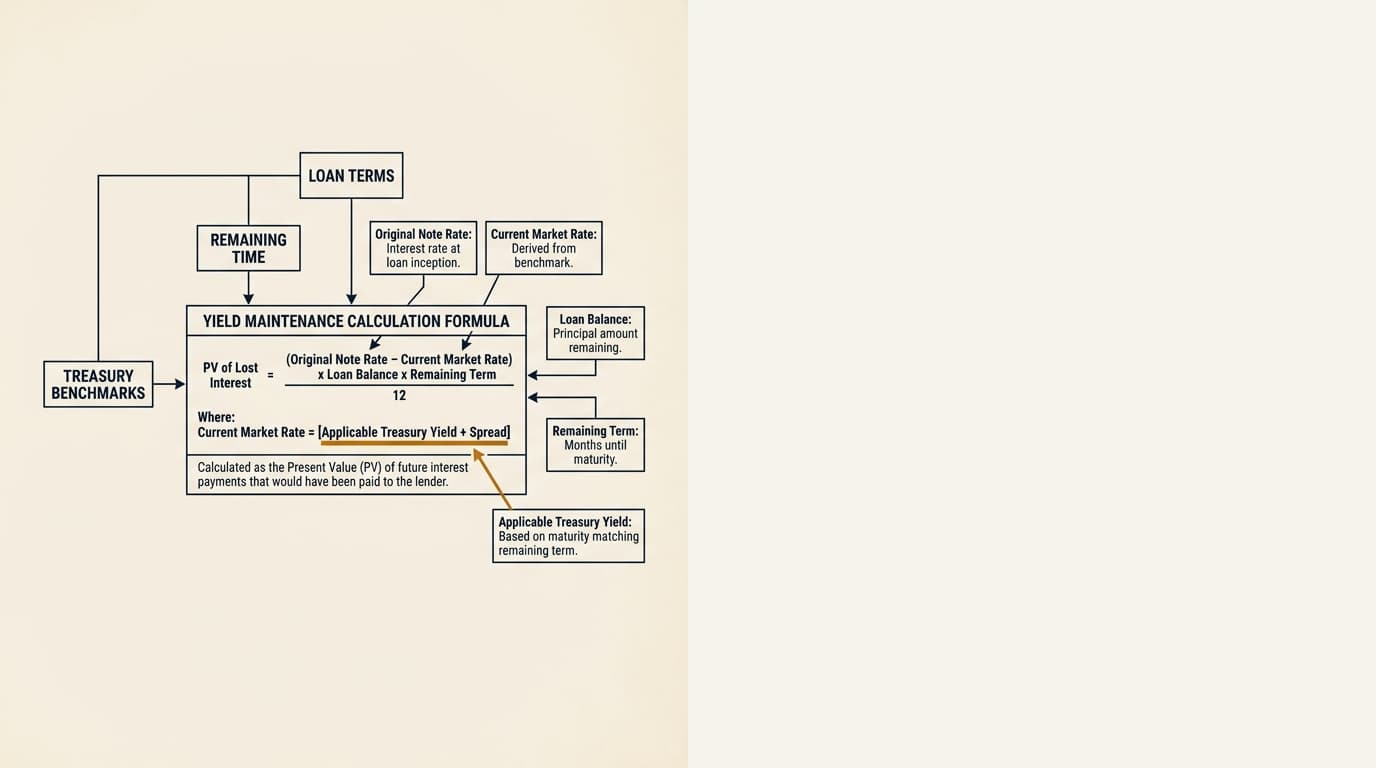

How Commercial Real Estate Yield Maintenance Is Calculated

The standard calculation compares the loan’s remaining scheduled interest stream with a Treasury-based reinvestment rate, then discounts that difference to present value. The exact formula varies by lender and document set, but the economic logic is usually the same.

Published descriptions from agencies and lenders usually come back to three basics: remaining scheduled payments, a Treasury benchmark tied to a similar maturity, and a spread or floor. Freddie Mac’s Optigo prepayment provisions materials explain that multifamily lending may use yield maintenance or defeasance depending on the product and execution, and that the cost is tied to preserving the lender’s or investor’s expected return. Cornell Law School’s Legal Information Institute entry on yield maintenance makes the same point in plainer terms: it compensates a lender for the loss that occurs when prepaid funds have to be reinvested at lower market rates.

At a high level, the calculation usually includes:

- Determine the unpaid principal balance and any accrued interest through the payoff date.

- Identify the remaining scheduled monthly payments through the open prepayment date or maturity, as defined in the note.

- Select the required benchmark Treasury yield and add or compare the contractual spread, if the documents require it.

- Compute the present value of the difference between the note rate cash flow and the reinvestment rate cash flow.

- Apply any minimum prepayment premium stated in the documents.

- Add servicing fees, legal fees, or statement fees if the loan documents allow them.

That sequence stays broad on purpose because the language changes from one document set to another. Some formulas discount each remaining payment separately. Some approximate the result using the unpaid balance and coupon spread. Some include a minimum of 1% of the balance or a greater-of test. Some stop the penalty several months before maturity instead of at maturity itself.

For a line-by-line walkthrough, see yield maintenance formula. For benchmark selection, see yield maintenance treasury rate. For a worked scenario, see yield maintenance calculation example.

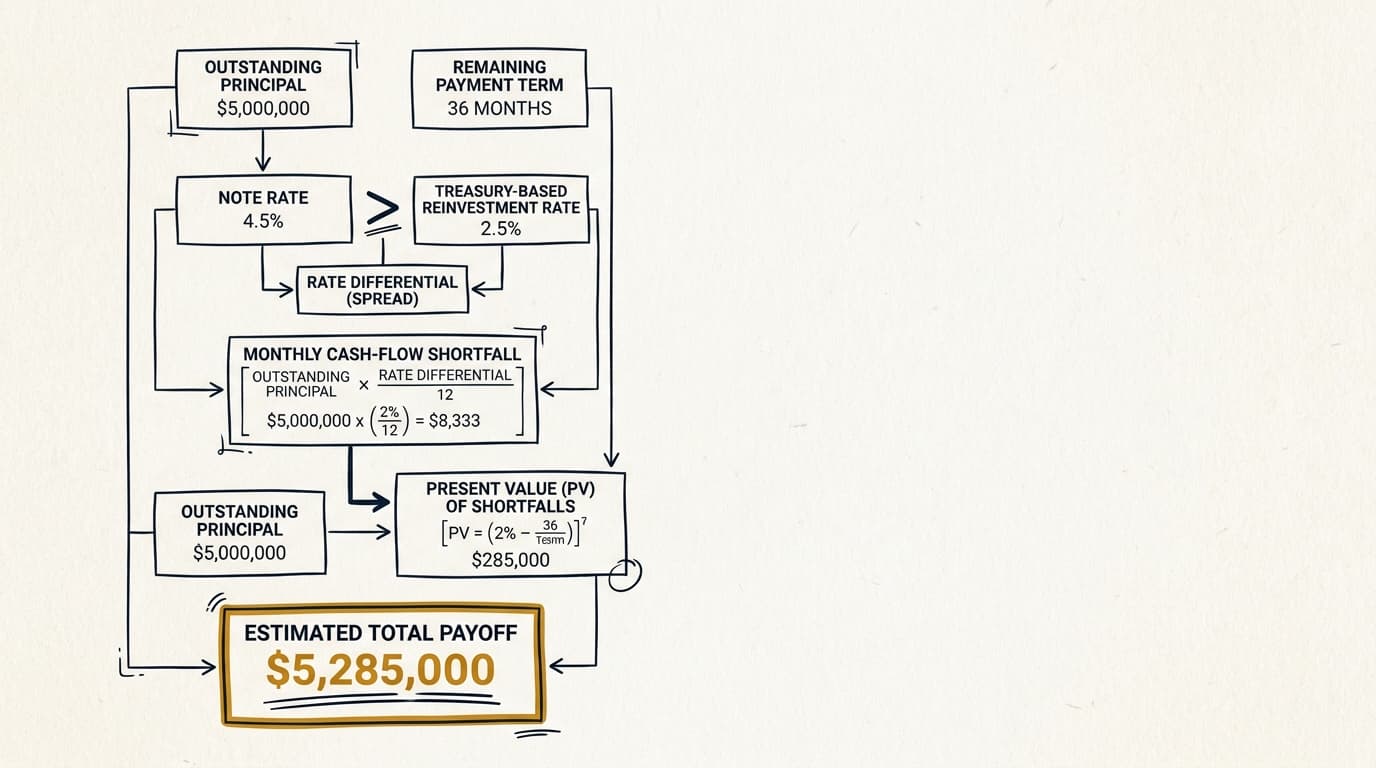

Simplified example using market-rate logic

A simple illustration shows why the charge can still be large even when the borrower is only a few years from maturity. Assume a $12 million fixed-rate loan at 6.00%, with 48 months remaining, monthly debt service based on a 30-year amortization schedule, and a contractual reinvestment benchmark of 3.75%.

| Input | Illustrative amount |

|---|---|

| Unpaid principal balance | $12,000,000 |

| Note rate | 6.00% |

| Months remaining | 48 |

| Reinvestment rate | 3.75% |

| Rate spread | 2.25% |

If the documents require a present-value calculation of the forgone interest differential, the premium can easily reach several hundred thousand dollars and, in a lower-rate market, more than $1 million. The exact figure depends on amortization, benchmark selection, discount method, and floors. This is why a rough coupon spread estimate is not enough. Get a formal payoff quote.

What Drives the Size of a Commercial Real Estate Yield Maintenance Charge

The biggest drivers are time remaining and rate differential. More time left on the loan, and a wider spread between the note coupon and the Treasury-based reinvestment rate, usually mean a larger charge.

In practice, the drivers fall into five buckets.

1. Remaining term

More months remaining means more above-market interest the lender expected to earn. A loan prepaid with 84 months left will usually produce a larger premium than the same loan prepaid with 18 months left, assuming the other inputs stay the same.

2. Interest-rate environment

Falling Treasury yields usually increase yield maintenance because the lender’s reinvestment alternative gets worse. Rising yields usually reduce it. This is the main reason payoff analysis should use live market rates, not stale assumptions. For a closer look, see yield maintenance in a falling rate environment.

3. Loan coupon and amortization

A higher note coupon can increase the lender’s forgone yield. Amortization matters too because it changes the timing and size of future scheduled payments. Two loans with the same balance and note rate can produce different premiums if one amortizes over 25 years and the other over 30.

4. Benchmark spread and minimum premium

Many clauses use a Treasury rate plus a spread, a Treasury rate minus a spread, or a floor. A minimum premium can keep the charge from dropping to zero even if market rates rise above the note rate. This is one more reason to check the payoff statement against the actual clause, not a generic market template.

5. Servicing and timing mechanics

Notice deadlines, remittance cycles, and quote validity periods can change the effective payoff date. In CMBS, the economics of a quote can shift if a transaction misses a monthly servicing cutoff and rolls into the next cycle. Borrowers dealing with securitized debt should review cmbs yield maintenance before locking in closing dates.

Refinance and Sale Scenarios: What the Numbers Mean in Practice

A prepayment premium only matters in context. The real question is not whether yield maintenance looks expensive in the abstract. The question is whether the refinance or sale still works after you include the premium, the new debt terms, rate savings, and transaction timing.

The table below gives a practical decision framework using stylized scenarios.

| Scenario | Likely issue | What to test | Common result |

|---|---|---|---|

| Sale with buyer requiring free and clear title | Existing fixed-rate loan must be retired | Yield maintenance cost versus assumption option | Assumption may preserve value if buyer can qualify and the rate is attractive |

| Refinance to lower coupon | Rate savings may not offset premium | Net present value of savings after premium and closing costs | Refi often works only if the rate drop is meaningful or leverage changes |

| Cash-out refinance | Borrower wants proceeds despite premium | Incremental proceeds versus penalty and reserve requirements | Works when the capital need is large enough to justify the all-in cost |

| Late-term exit with open period approaching | Waiting may eliminate penalty | Cost of carry during the wait period versus avoided premium | Waiting can be cheaper if market and transaction conditions hold |

| CMBS sale process | Servicer timelines may control the closing calendar | Notice periods, quote validity, legal review, defeasance triggers | Execution timing often matters as much as headline economics |

This is usually where borrower and broker analysis gets sharper. Instead of asking whether the clause is good or bad in general, look at the actual alternatives available on the actual transaction date. A seller with a 4.10% assumable loan in a 6.25% financing market may preserve pricing by marketing the debt as part of the asset. A sponsor refinancing from 6.35% to 5.85% may find the rate savings do not justify a seven-figure premium unless the new loan also extends term, releases reserves, or increases proceeds.

For a transaction-specific framework, see yield maintenance refinance or sale.

Commercial Real Estate Yield Maintenance vs Defeasance

Yield maintenance and defeasance both protect noteholders against early retirement risk, but they work differently. Yield maintenance produces a payoff premium tied to a formula. Defeasance usually substitutes collateral, which allows the original loan to stay outstanding instead of being paid off directly.

Fannie Mae’s educational guidance on defeasance and yield maintenance notes that the economic objective is similar even though the mechanics differ. In securitized executions, defeasance often brings extra third-party costs, securities purchase logistics, and closing coordination that sit on top of the base interest-rate economics.

| Issue | Yield maintenance | Defeasance |

|---|---|---|

| Basic structure | Borrower pays off loan plus premium | Borrower replaces collateral and leaves note outstanding |

| Main cost driver | Present value of forgone yield | Cost of defeasance collateral plus fees |

| Process complexity | Moderate, document-dependent | Higher, often involves consultants, securities dealers, counsel, and servicer approval |

| Timing sensitivity | Sensitive to Treasury rates and quote date | Sensitive to securities pricing, servicer cutoffs, and settlement timing |

| Typical use case | Portfolio and balance-sheet loans, some agency and permanent loans | Common in CMBS and some agency structures |

The practical distinction is straightforward: yield maintenance is usually easier to explain, but not always cheaper. Defeasance may produce a better or worse result depending on rates, fees, and timing. Borrowers comparing the two should use transaction-specific quotes, not rules of thumb.

For a detailed side-by-side analysis, use yield maintenance vs defeasance. For securitized loans specifically, see cmbs yield maintenance vs defeasance.

Commercial Real Estate Yield Maintenance vs Step-Down

Step-down prepayment uses a declining schedule of fixed percentage penalties. Yield maintenance uses a market-sensitive formula tied to reinvestment rates. Step-down structures are easier to model in advance. Yield maintenance is less predictable because Treasury yields move every day.

A typical step-down might read 5%, 4%, 3%, 2%, 1% over successive years, while yield maintenance could land much lower or much higher depending on the rate environment and time remaining. In a lower-rate market with years left to maturity, yield maintenance can exceed a step-down by a wide margin. In a higher-rate market late in the term, the opposite can happen.

| Issue | Yield maintenance | Step-down |

|---|---|---|

| Predictability | Lower | Higher |

| Sensitivity to Treasury rates | High | None |

| Ease of borrower modeling | Moderate to difficult | Easy |

| Potential cost late in term | Can still be meaningful | Usually declines mechanically |

| Negotiation focus | Benchmark, spread, floor, open period | Penalty schedule and burn-off timing |

Borrowers negotiating new debt often focus too much on coupon and leverage and not enough on exit terms. That is a real mistake in short-hold or refinance-driven strategies. A slightly higher coupon with a simpler step-down may create better optionality than a lower coupon paired with strict yield maintenance.

For the fuller comparison, see yield maintenance vs step-down.

Loan Documents Control the Result

The enforceable answer is in the documents, not in market shorthand. The promissory note, loan agreement, prepayment rider, guaranty carveout language, servicing transfer notices, and payoff statement instructions decide how commercial real estate yield maintenance is actually applied.

Borrowers should not assume the phrase “yield maintenance” means the same thing from one lender to the next. The key variables usually include the benchmark index, the spread, the discount rate, the minimum premium, the protected period, the treatment of partial prepayments, the open period before maturity, and whether assumption is allowed. The Consumer Financial Protection Bureau explanation of prepayment penalties makes the underlying contract point clearly, even though the page is not CRE-specific: these provisions vary by loan terms, and the wording matters.

Document checklist for review

A reliable review starts with the defined terms and payment provisions. Miss one definition and the quote can change.

- Read the note definition of “Prepayment Consideration,” “Yield Maintenance Premium,” or a similar term.

- Confirm the date through which the premium applies and whether there is an open period before maturity.

- Identify the Treasury benchmark and how the comparable maturity is selected.

- Check for a floor, minimum premium, or greater-of test.

- Confirm whether assumption, supplemental debt, or partial release provisions change the analysis.

- Review servicing notices for lead times, quote validity, and wire instructions.

For document language and clause-level analysis, see yield maintenance loan documents. For negotiation points before closing a new loan, see yield maintenance borrower negotiation.

Property Type and Loan Type Variation

Yield maintenance is a broad CRE concept, but loan programs and property types can change how it is underwritten, administered, and negotiated. Multifamily agency executions, life company loans, bank portfolio loans, and CMBS loans do not use identical structures.

Freddie Mac’s Multifamily servicing guidance says the key point directly: prepayment rights depend on the product and the documents. That matters because an owner of stabilized multifamily with agency debt may face a very different path from an office borrower in a balance-sheet or CMBS execution.

- Multifamily loans: agency programs often have standardized servicing procedures and specific prepayment options. See yield maintenance multifamily loans.

- Office and retail loans: asset-level leasing risk can affect refinance timing and buyer demand, which then changes the practical cost of a prepayment clause. See yield maintenance office retail.

- CMBS loans: servicer process, remittance cycles, and defeasance alternatives often matter more than borrowers expect. See cmbs yield maintenance.

Decision Framework for Borrowers, Investors, and Brokers

The useful question is whether paying the premium improves net value after you compare all realistic alternatives. A sound framework tests four options: prepay now, wait for a lower-cost window, pursue assumption, or keep the loan in place.

This is where many articles stop too early. The official sources explain the provision itself, which is useful, but the real-world choice is transactional. The right answer depends on total economics, not just the formula.

For borrowers considering refinance

Refinancing through yield maintenance only works if the new loan creates value after all costs. That means looking at rate savings, proceeds, reserves, extension value, and the chance that rates or property performance change if you wait.

- If the main goal is lower debt service, compare the present value of monthly savings against the full premium and refinancing costs.

- If the goal is cash-out, compare net proceeds after payoff, reserves, escrows, and fees.

- If the loan reaches an open period within months, test whether waiting produces a better result than refinancing immediately.

For sellers and brokers evaluating a sale

Sale economics can move a lot depending on whether the debt is assumable. A below-market coupon can support a higher sale price if the buyer can assume the loan. A large yield maintenance premium can do the opposite and cut seller proceeds if assumption is not available.

- Market the debt terms early, not after the purchase agreement is signed.

- Ask the servicer whether assumption is allowed and how long approval usually takes.

- Model both paths: a free-and-clear sale with payoff and an assumption-based sale.

For investors and asset managers

Yield maintenance should be treated as an exit cost built into the capital stack. It affects hold-period strategy, refinance flexibility, and when returns can actually be realized.

- In acquisition underwriting, map the burn-off date and test multiple exit windows.

- In portfolio management, track whether rate moves change the economics of refinancing.

- In disposition planning, coordinate debt review with buyer outreach and title timing.

For accounting and reporting treatment, see yield maintenance accounting tax.

Common Edge Cases and Exceptions

Several less obvious issues can change the result even when the clause looks straightforward. This is also where payoff disputes and closing delays tend to show up.

Partial prepayments and releases

Some loans treat principal curtailments, parcel releases, or condemnation proceeds as partial prepayments subject to the same premium logic. Others use separate release-price schedules. The note controls.

Misreading the open period

Borrowers often assume the premium ends at maturity. Many documents cut off yield maintenance several months before maturity, while others carry it almost to the end. A 90-day difference can materially change a refinance decision.

Payoff statement validity periods

A quote may only be valid through a limited date and may change if Treasury rates move or closing gets delayed. In active rate markets, a stale quote can create a real mismatch between modeled proceeds and actual proceeds.

Assumption versus payoff

A buyer assumption can avoid or reduce a prepayment premium, but only if the documents allow it and the transferee meets underwriting and servicing requirements. This is not just a legal footnote. It is a deal-structure issue.

CMBS procedural risk

In securitized loans, missing a servicer deadline can delay closing even if the economics work. That risk is procedural, but it still affects deal certainty and needs to be built into the timeline.

How to Analyze a Potential Payoff

A useful payoff analysis starts with the existing note and ends with a quote tied to a specific closing date. The goal is to compare real alternatives, not rough rules of thumb.

- Collect the note, loan agreement, prepayment rider, amortization schedule, and latest servicing correspondence.

- Confirm the unpaid principal balance, coupon, amortization, maturity date, and any open-prepayment window.

- Request a payoff statement or preliminary premium quote tied to a proposed closing date.

- Verify which Treasury benchmark and spread the servicer is using under the documents.

- Model at least three paths: prepay now, wait until the next lower-cost window, and pursue assumption if allowed.

- Include all ancillary costs, including defeasance fees, legal costs, servicing charges, and new loan closing costs where relevant.

- Stress-test the result for rate movement and closing delays.

- Reconfirm the quote shortly before execution because daily market changes can move the premium.

Borrowers who need a clause-level explanation of the premium itself should review yield maintenance prepayment penalty. Those comparing transaction timing choices should review yield maintenance refinance or sale.

Commercial Real Estate Yield Maintenance and Transaction Planning

Commercial real estate yield maintenance is not a generic fee attached to early payoff. It is a rate-sensitive exit cost defined by the note and applied through servicing procedure. For borrowers, investors, and brokers, the job is to identify the controlling clause, quantify the premium for the intended closing date, and compare that cost against the real alternatives, whether that means waiting, assumption, defeasance, or a different transaction structure.

This is why the review needs to happen early: at acquisition, before a refinance process starts, and before a sale goes to market. Once payoff instructions are already circulating, most of the leverage from earlier document review is gone.

Frequently Asked Questions

What is commercial real estate yield maintenance?

Commercial real estate yield maintenance is a prepayment provision that charges a borrower for paying off a CRE loan before the protected date in the loan documents. The charge is meant to compensate the lender or noteholder for lost expected interest income if market reinvestment rates are lower than the loan coupon.

How is a yield maintenance charge calculated on a CRE loan?

The exact formula depends on the note, but most CRE yield maintenance provisions look at the remaining scheduled payments, compare the loan coupon to a Treasury-based reinvestment rate, discount the difference to present value, and then apply any floor or minimum premium. The final payoff usually also includes unpaid principal, accrued interest, and any permitted servicing or legal charges.

When does yield maintenance apply before maturity?

Yield maintenance usually applies when a borrower prepays a fixed-rate loan before the date the documents allow open prepayment without penalty. In many loans, that means it applies after any lockout period but before a final open window near maturity. The exact start and end dates vary by note and servicing guidance.

Is yield maintenance the same as defeasance?

No. Yield maintenance is usually a formula-based prepayment premium paid at payoff, while defeasance usually replaces the real estate collateral with government securities and allows the original loan to remain outstanding. The economic objective is similar, but the process, fees, and timing are different.

Does yield maintenance vary by market or property location?

The core formula usually does not change just because of property location, but transaction outcomes can vary by market because refinance options, buyer demand for assumption, and lender appetite differ. A multifamily asset in a deep agency market, for example, may have more assumption or refinance options than a smaller single-tenant property in a thin tertiary market. That can change whether paying the premium makes economic sense.