Yield Maintenance Formula: Audit the Calculation

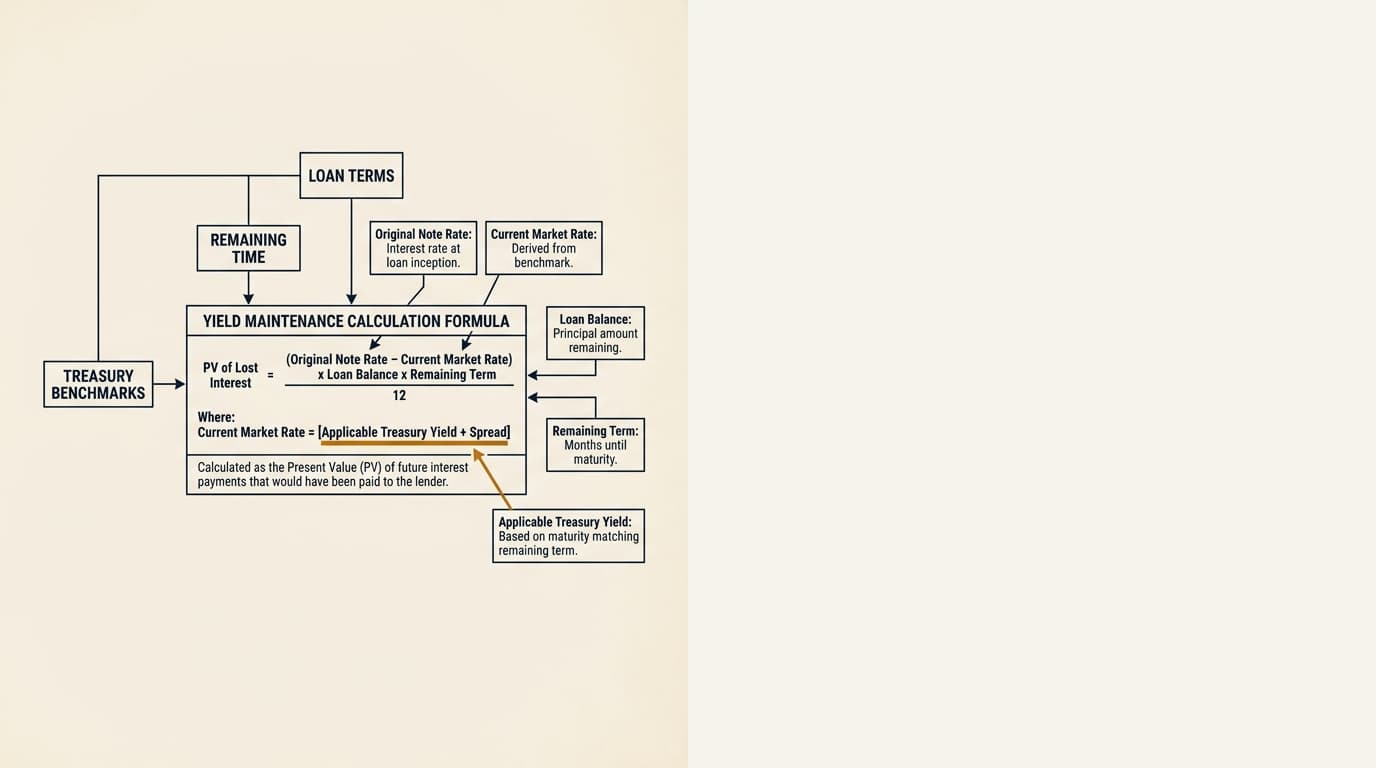

Yield maintenance usually equals the present value of the lender’s lost interest, using the scheduled loan payments discounted at a Treasury-based reinvestment rate, with any contractual spread added or subtracted. In practice, the outcome depends less on what the note calls it than on three things: the remaining amortization schedule, the Treasury benchmark the loan points to, and the discount rate set in the loan documents.

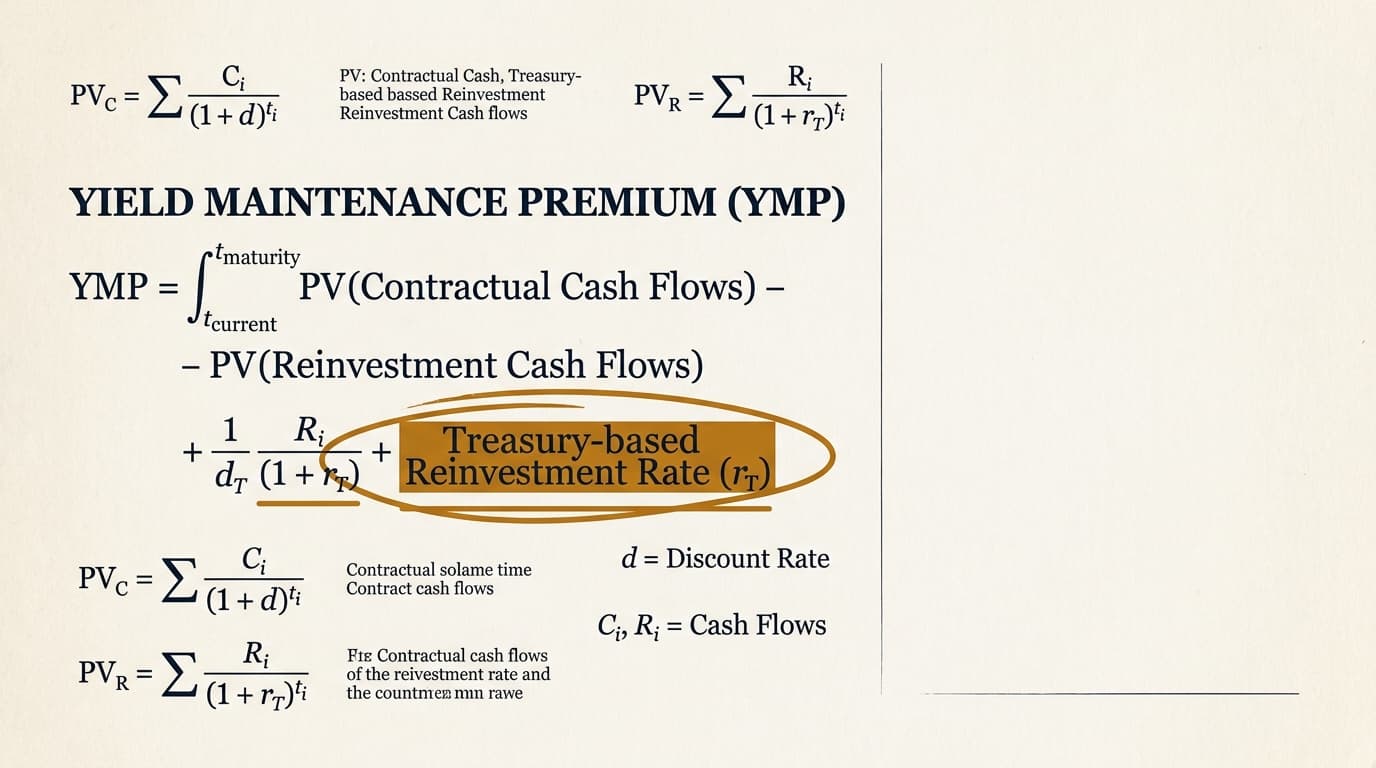

The yield maintenance formula is a present value calculation. Its job is simple: make the lender whole for the gap between the loan’s contract rate and whatever rate the lender could earn after you prepay. In most commercial mortgage notes, that means discounting the lender’s expected lost interest over the remaining term using a U.S. Treasury-based benchmark, then applying any floor, spread, or minimum prepayment amount built into the documents.

This article deals with the math lenders actually use in 2026 payoff statements: present value methodology, benchmark selection, spread assumptions, and the note language that changes the answer. It is for borrowers, asset managers, and analysts who want to check whether a quoted yield maintenance charge matches the note, instead of taking the servicer’s number on faith.

Yield maintenance formula: direct answer

The standard yield maintenance formula usually comes down to the present value of the difference between the loan’s note-rate cash flows and replacement-rate cash flows over the remaining term, subject to the exact note language. In real payoff work, lenders often calculate it as the present value of scheduled remaining debt service or an interest shortfall, discounted at a Treasury-based rate, less outstanding principal, plus any unpaid amounts due at payoff.

A simplified version looks like this:

Yield Maintenance Premium = PV of Remaining Scheduled Payments discounted at Treasury-based rate - Outstanding Principal Balance

Some notes instead use:

Yield Maintenance Premium = PV of [(Loan Rate - Reinvestment Rate) x Scheduled Principal Balance over Remaining Term]

That wording is not cosmetic. Two formulas that sound close can produce meaningfully different numbers, especially when amortization, balloon payments, or discounting conventions differ. According to the Cornell Law School Legal Information Institute explanation of present value, present value converts future cash flows into a current amount using a specified discount rate. In commercial payoff practice, that discount rate is usually tied to a U.S. Treasury yield named in the note.

Key Takeaways

These are the variables that usually decide whether a lender’s yield maintenance number is right or wrong.

- The biggest drivers are the remaining payment schedule, the Treasury benchmark the note calls for, and any spread added to or subtracted from that benchmark.

- A 25-basis-point change in the discount rate can move present value a lot, especially when more than five years remain before maturity.

- Loan documents vary on whether the calculation uses remaining debt service, interest-only shortfall, or a spread-to-Treasury present value method.

- Most benchmark disputes come from constant maturity versus comparable-term Treasuries, and from the date used to pull the rate.

- A proper audit starts with the note and prepayment clause, then rebuilds the amortization schedule and discounts each remaining payment using the exact convention in the documents.

The standard yield maintenance formula and what each term means

The note usually defines yield maintenance more clearly than the payoff statement does. If you are reviewing a quote, start there. Every defined term in the prepayment clause should map to a line in the calculation.

Most commercial mortgage notes use some mix of these variables:

| Formula component | What it means in practice | Why it matters |

|---|---|---|

| Outstanding principal balance | Unpaid principal as of the payoff date | Sets the base amount being retired |

| Remaining scheduled payments | Contractual monthly debt service through maturity, often excluding default interest | Determines the future cash flows used in present value |

| Note rate | Stated interest rate on the loan | Higher note rates usually increase yield maintenance when market rates fall below the loan rate |

| Reinvestment rate | Treasury benchmark, sometimes with a spread adjustment | Lower discount rates increase present value and therefore the premium |

| Spread or floor | Contractual addition, subtraction, or minimum rate/premium | Keeps the calculation from dropping below a specified level |

| Remaining term | Time from payoff date to maturity or open-prepay date | Longer remaining terms increase the premium |

According to the Federal Reserve H.15 Selected Interest Rates release, Treasury yields are published across multiple maturities and are widely used as reference rates in commercial finance. But notes do not all point to the same series. Some refer to the U.S. Treasury constant maturity closest to the loan’s remaining average life. Others use the maturity closest to the remaining term to maturity. Others call for a securities dealer quote if there is no direct match.

That is why the same loan can produce two different payoff numbers depending on who rebuilds the formula.

How present value methodology works in lender payoff calculations

Present value is the center of the yield maintenance formula. The lender asks a straightforward question: what is the future payment stream worth today, compared with the principal it gets back now and can reinvest?

The mechanics usually work like this:

- Project each remaining scheduled payment from the payoff date through maturity or the first open-prepayment date.

- Determine the periodic discount rate from the Treasury benchmark named in the note, plus or minus any spread adjustment.

- Discount each projected payment back to the payoff date.

- Add the discounted payments to get total present value.

- Subtract the outstanding principal balance, then apply any contractual floor, minimum premium, or exclusion.

According to the U.S. Securities and Exchange Commission Investor.gov explanation of present value, lower discount rates produce higher present values for future cash flows. That is why yield maintenance charges usually increase when Treasury yields fall below the loan coupon.

Monthly discounting vs. annual discounting

Most commercial mortgage calculations discount monthly because debt service is paid monthly. Some notes say little or nothing about compounding, and that is where small but real differences creep in.

Take a loan with 72 monthly payments left. If the note defines the reinvestment rate as 3.80% annually but says nothing about compounding, one analyst may discount at 3.80% divided by 12. Another may convert it to an effective monthly rate. On a big balance, that difference may not change the decision to prepay, but it can absolutely matter in an audit or settlement discussion.

Scheduled payments vs. interest shortfall

Not every note discounts the same cash flow stream. Some formulas use the present value of all remaining principal and interest payments, then subtract principal. Others discount only the excess interest stream above the Treasury reinvestment rate.

That difference changes how amortization shows up in the result. On an amortizing loan, a full-payment present value method tracks the timing of principal return more accurately. On an interest-only loan with a balloon, the premium is often much more sensitive to the final balloon date and the benchmark term selected.

Treasury benchmark selection: where disputes usually start

Benchmark selection is often the most contestable input in the lender’s calculation. A payoff quote can move a lot depending on whether the note uses a Treasury constant maturity, a Treasury security with a comparable term, or an interpolated rate between published maturities.

According to the U.S. Department of the Treasury daily Treasury par yield curve rates, the Treasury publishes daily par yields at standard maturities such as 1, 2, 3, 5, 7, 10, 20, and 30 years. Many notes point to that curve indirectly but do not say what happens when the remaining loan term is something awkward like 6 years and 4 months.

Closest maturity vs. interpolated rate

A note that says the lender should use the Treasury rate "most nearly equal" to the remaining term may allow a simple closest-point approach. A note that refers to a rate for a "comparable remaining term" may support interpolation between two published Treasury points.

Example:

- Remaining term to maturity: 6.33 years

- Published Treasury par yields: 5-year at 3.70%, 7-year at 3.95%

Using the 7-year point gives you a discount rate 25 basis points higher than using the 5-year point. Interpolating between the two gives about 3.87%, which lands between them. On a large loan with a long remaining term, that gap can change the premium by tens of thousands of dollars.

Rate observation date

The observation date matters too. Some documents use the Treasury yield on the prepayment date. Others use the yield a stated number of business days before payoff. Some servicing practices tie the date to when the quote was issued.

According to the U.S. Treasury marketable securities regulations in 31 CFR Part 356, Treasury securities trade in an active market with daily yield movement. In a volatile rate environment, using the wrong observation date can change the result even if the benchmark maturity itself is right.

For a more detailed discussion of benchmark mechanics, see yield maintenance treasury rate. This article stays focused on how the benchmark feeds into the formula, not the full benchmark taxonomy.

Spread assumptions and discount rate conventions

Many notes do not use the raw Treasury yield as the discount rate. They add a spread, usually stated in basis points above the benchmark, though some forms use a floor or a separate minimum return test.

A common structure is: Discount Rate = Treasury Yield + X basis points. The effect is straightforward. A higher discount rate lowers the present value of the remaining payments and reduces the yield maintenance premium.

Spreads show up for a few practical reasons:

- To reflect the lender’s assumed reinvestment spread above the risk-free curve.

- To keep the premium from getting overstated when Treasuries sit far below commercial mortgage rates.

- To standardize calculations across servicing platforms and loan programs.

According to the Federal Reserve Bank of New York reference rates and market data resources, spread conventions are market choices, not one fixed regulatory standard. So two lenders can both call a premium yield maintenance while using different discount-rate constructions.

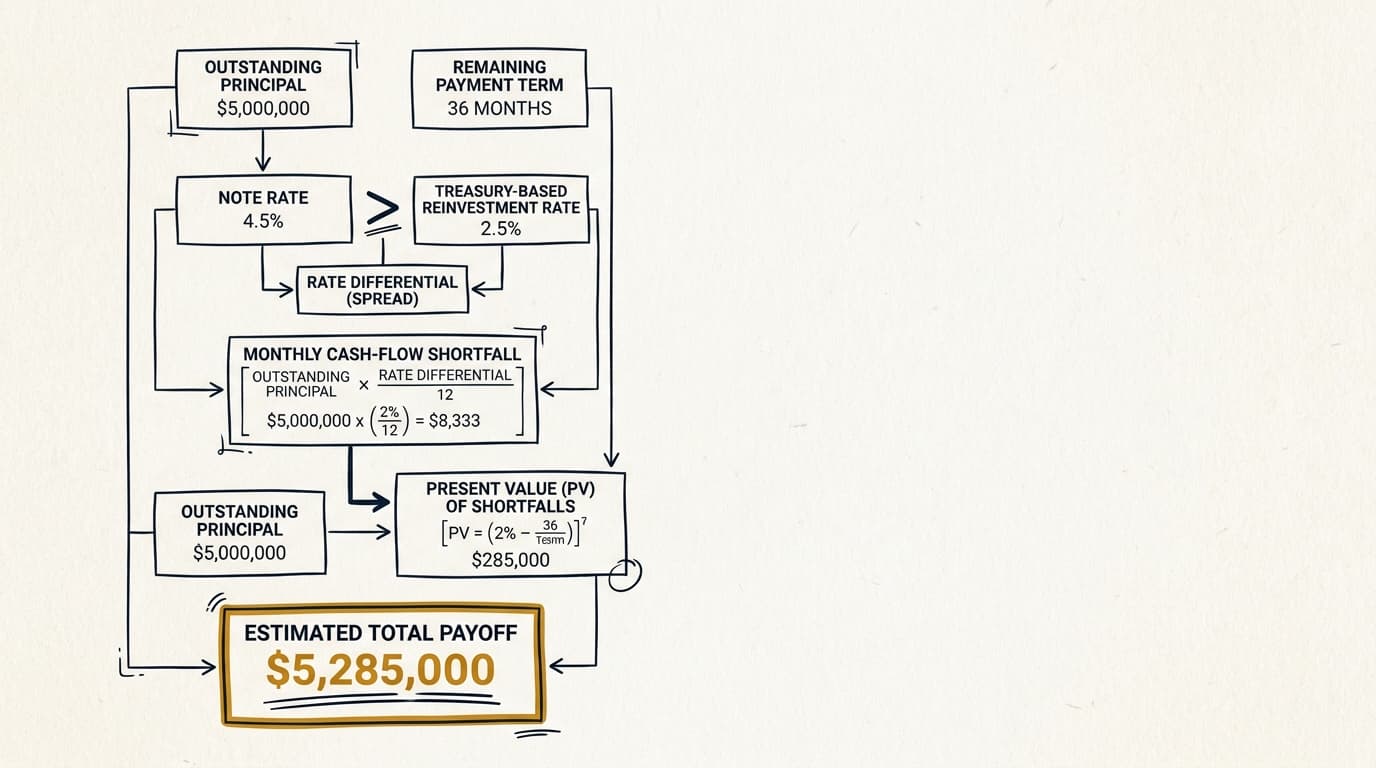

Why 25 basis points matters

A 25-basis-point difference sounds minor until you run it through every remaining payment. Take a simplified case: a $12 million balance, 84 months remaining, and fixed monthly debt service. If the discount rate moves from 4.00% to 4.25%, the present value of that payment stream falls. The exact amount depends on amortization and coupon, but it is often large enough that a serious borrower should check the math rather than shrug and move on.

This is one of the easiest places for a payoff quote to drift away from the note language.

Step-by-step: how to audit a yield maintenance formula

A reliable audit rebuilds the calculation from the loan documents up, not from the payoff quote backward. The point is to test each variable on its own and find where the lender’s method departs from the contract.

- Read the note and prepayment clause. Identify the exact defined terms for Treasury benchmark, spread, remaining term, and any floor or minimum premium.

- Confirm the payoff date and observation date. Check whether the benchmark rate should be taken from the payoff date, quote date, or a specified earlier date.

- Rebuild the amortization schedule. Verify the outstanding principal balance, remaining payment dates, and whether the loan is amortizing, interest-only, or balloon.

- Select the benchmark Treasury exactly as drafted. Use the correct published source and maturity convention, and document whether interpolation is required.

- Apply the contractual spread and compounding method. Convert the annual discount rate into the periodic rate the note requires.

- Discount each remaining payment. Calculate present value payment by payment unless the note clearly allows a shortcut.

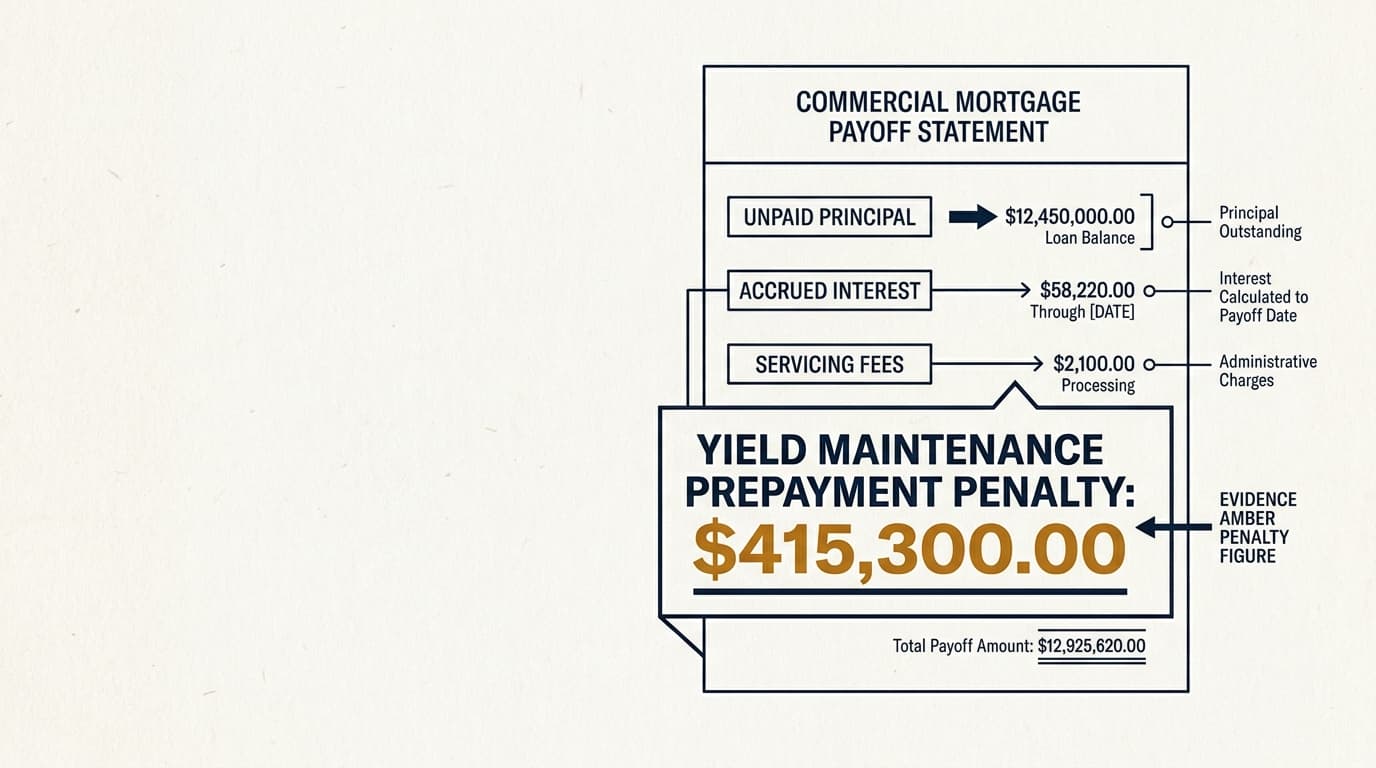

- Subtract principal and add other payoff amounts separately. Keep yield maintenance separate from unpaid interest, late charges, legal fees, or defeasance-related costs.

- Test alternative assumptions. Run sensitivity checks on benchmark date, maturity point, and spread to see whether the quoted result falls outside a reasonable range.

Borrowers dealing with a broader payoff question may also want the framework in commercial real estate yield maintenance, which covers timing, loan types, and alternatives at the portfolio level. If the issue is the lender’s premium rather than the underlying formula, yield maintenance prepayment penalty covers how payoff charges are presented and where they often depart from expectations.

Common formula variations in loan documents

There is no universal yield maintenance formula. The note, rider, or securitization form controls, and small drafting differences can change the result in a real way.

| Variation | Typical language pattern | Practical effect |

|---|---|---|

| PV of remaining debt service less principal | Present value of all remaining scheduled payments discounted at Treasury plus spread | Common in portfolio loans; captures payment timing precisely |

| Interest differential method | Discounted value of excess interest over reinvestment rate | Often easier to model, but sensitive to principal schedule assumptions |

| Treasury plus spread floor | Benchmark cannot be less than a stated minimum | Keeps very low benchmark rates from pushing the premium beyond the drafted limit |

| Minimum prepayment premium | Greater of yield maintenance or a set percentage of principal | Creates a floor even when rates rise |

| Open period carveout | No premium in the final 60-180 days before maturity | Shortens the modeled term and can reduce the premium a lot |

According to the Consumer Financial Protection Bureau Regulation Z resources, disclosure requirements differ by loan type and transaction scope. Commercial mortgage notes usually rely on negotiated contract language, not consumer-style standardized prepayment disclosures. That is why formula review is so document-heavy.

This is also where people make avoidable mistakes by importing assumptions from other loan types. A formula in one bank’s life-company style note may not match a balance-sheet lender’s form or a securitized loan document.

Edge cases that change the math

Some edge cases can change what looks like a straightforward formula. These issues rarely make it into short summaries, but they often decide whether a payoff quote holds up under review.

Partial-month interest and irregular payoff dates

Many quotes are issued for dates that do not line up with scheduled payment dates. The lender may add per diem interest through the payoff date while the yield maintenance model still assumes monthly payment intervals. If the note does not say how stub periods should be handled, small mismatches can show up between the amortization schedule and the premium calculation.

Open prepayment window before maturity

Some notes allow prepayment without a premium during the final 90 or 180 days before maturity. In those cases, the remaining term for discounting may end at the start of that open window, not at maturity. If the lender runs the model all the way to maturity anyway, the premium is overstated.

Default rate periods

Yield maintenance usually refers to scheduled payments under the original note, not accelerated debt or default-rate interest, unless the documents clearly say otherwise. If the loan is in default, payoff statements often bundle several components together. That is exactly when you need to separate them and test each one on its own.

Assumption or defeasance rights

If the loan can be assumed or defeased, that comparison may affect the borrower’s exit decision even if it does not change the formula itself. Those alternatives are covered in separate analyses, including yield maintenance vs defeasance, but they matter here for a simple reason: a formula can be mathematically correct and still be the wrong commercial outcome.

Decision framework: when a formula result deserves a second look

A payoff quote deserves a closer look when the premium does not fit the remaining term, the current Treasury curve, or the loan structure. The quickest test is to compare the shape of the result to what the note actually says the formula should do.

Use this framework:

| Scenario | What the formula should generally show | Why it may require review |

|---|---|---|

| Rates far below note rate, long term remaining | Higher premium | If the quote is low, the lender may have used the wrong Treasury or left out payments |

| Rates near or above note rate | Lower premium, sometimes subject to a minimum | If the quote stays high, check for a floor or minimum premium clause |

| Loan in final open-prepay period | No premium or sharply reduced premium | If the quote still runs to maturity, the end date may be wrong |

| Interest-only balloon structure | Sensitivity to benchmark term and final balloon date | Small errors in remaining term can move the result a lot |

| Quote issued on volatile rate day | Sensitivity to observation date | Check whether the benchmark was pulled on the correct contractual date |

This is where generic source pages usually stop being useful. Two quotes can both look mathematically coherent, and only one may be contractually correct. The real job is not just recalculating. It is matching the lender’s method to the note’s defined terms and the market data source the clause actually references.

Frequently Asked Questions

What is the basic yield maintenance formula for a commercial loan?

The basic yield maintenance formula is usually the present value of the lender’s remaining scheduled loan payments, discounted at a Treasury-based reinvestment rate defined in the note, minus the outstanding principal balance. Some documents instead calculate the present value of the interest-rate differential over the remaining term. The promissory note controls.

Which Treasury rate should be used in a yield maintenance formula?

The right Treasury rate is the one named in the loan documents, not whichever publicly quoted rate a servicer happens to prefer. Depending on the note, that may be a U.S. Treasury constant maturity yield, a rate for a comparable remaining term, or an interpolated rate between two published maturities from the U.S. Department of the Treasury daily par yield curve.

Why does a small change in the discount rate affect yield maintenance so much?

Because the discount rate affects every remaining payment in the present value calculation. On a loan with several years left before maturity, moving the benchmark or spread by 10 to 25 basis points changes the discounted value of dozens of future cash flows. The longer the remaining term, the bigger the effect.

Can yield maintenance calculations differ by lender or region?

Yes. Commercial mortgage practice is contract-driven, so differences usually come from lender forms, loan programs, and servicing platforms more than from state law alone. Regional market practice can influence drafting, but the note and mortgage documents control the formula. In New York and other large commercial lending markets, heavily negotiated notes often define benchmark selection and observation dates with much more precision than smaller-balance regional loan forms do.

How can a borrower verify a lender’s payoff statement?

A borrower can verify a payoff statement by rebuilding the amortization schedule, identifying the exact benchmark Treasury and spread from the note, discounting each remaining payment back to the payoff date, and separating yield maintenance from other payoff charges. If the quote combines fees, default interest, or legal costs with the premium, those amounts should be tested separately.