Yield Maintenance vs Defeasance: Cost and Timing

Yield maintenance and defeasance can lead to meaningfully different payoff costs on the same commercial real estate loan. The less expensive option depends on interest rates, time remaining on the loan, servicing requirements, securities costs, and how quickly the deal has to close.

On many commercial mortgage-backed securities loans, the gap between yield maintenance and defeasance is real money. It can swing an exit by tens or hundreds of thousands of dollars, and it can push a closing back by weeks. This comparison walks through how yield maintenance vs defeasance plays out in actual CMBS payoffs, which costs matter, and when one route is cheaper or simply easier to get done.

If you're weighing a refinance, sale, or recapitalization, a definition won't get you very far. You need a practical way to compare prepayment cost, transaction mechanics, legal and servicing requirements, and timing risk in 2026.

Key Takeaways

- Yield maintenance is a prepayment charge based largely on the lender's lost yield, while defeasance replaces the original real estate collateral with government securities and leaves the loan in place.

- Defeasance usually brings extra third-party costs — legal fees, servicer fees, accountant review, securities brokerage, and successor borrower formation — that do not exist in a simple payoff.

- In CMBS loans, the documents often limit or prohibit open prepayment but allow defeasance after a lockout period. The controlling answer is in the note, pooling and servicing structure, and servicer instructions.

- Falling Treasury yields tend to increase yield maintenance costs, while defeasance turns on the cost of the securities portfolio needed to match the remaining debt service.

- A real comparison requires a live quote for both structures, not a rule of thumb. Borrowers should get document-level guidance from the servicer and a current cost estimate before signing a sale contract.

What yield maintenance vs defeasance means in practice

Yield maintenance vs defeasance comes down to two different ways to exit a loan early, or at least neutralize it economically before maturity. Yield maintenance usually means paying off the loan plus a prepayment premium. Defeasance usually means replacing the real estate collateral with a securities portfolio so the loan keeps running on its original schedule.

According to the Legal Information Institute definition of defeasance, defeasance means rendering a bond or contract void or discharged under stated conditions. In commercial real estate finance, the term is narrower and more transactional: the borrower or a successor entity buys qualifying securities, usually U.S. Treasury or other permitted government-backed obligations, in amounts sufficient to make the remaining scheduled loan payments.

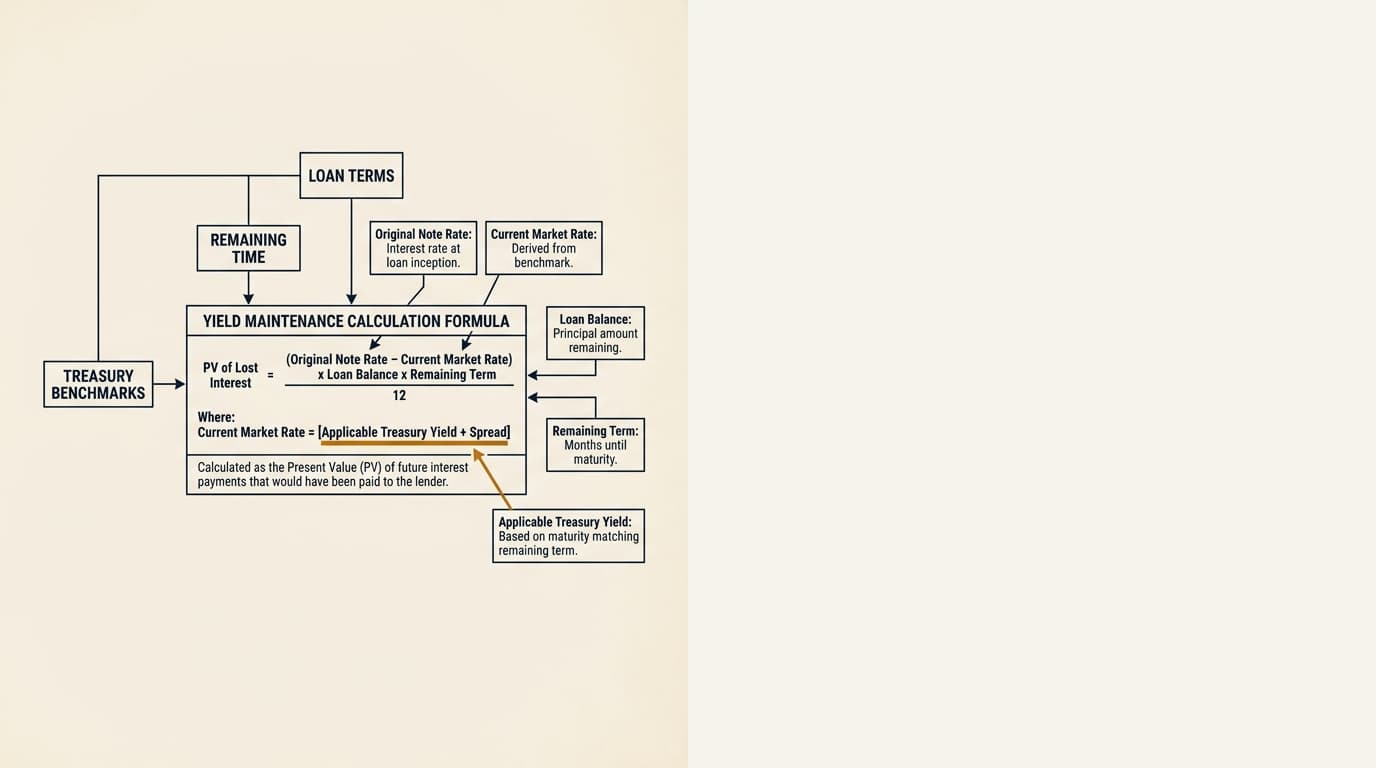

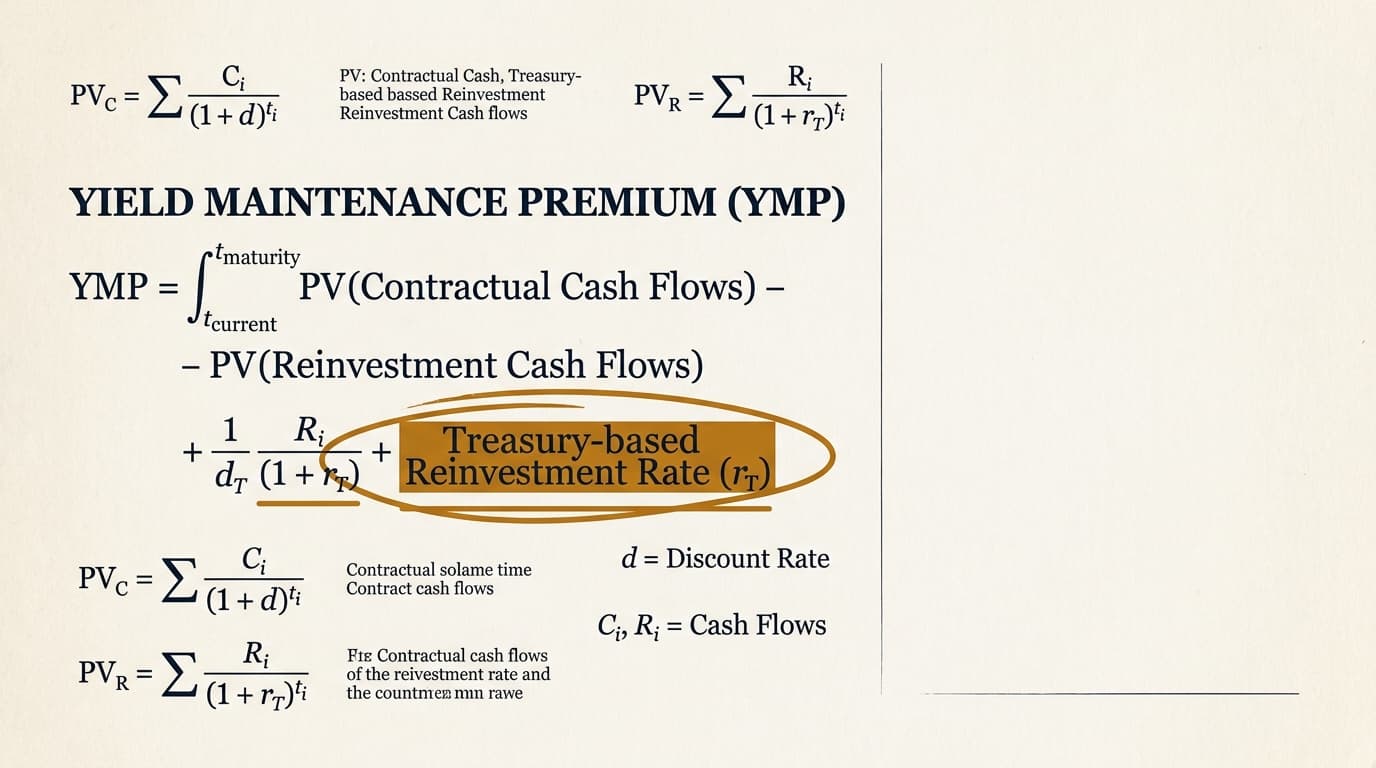

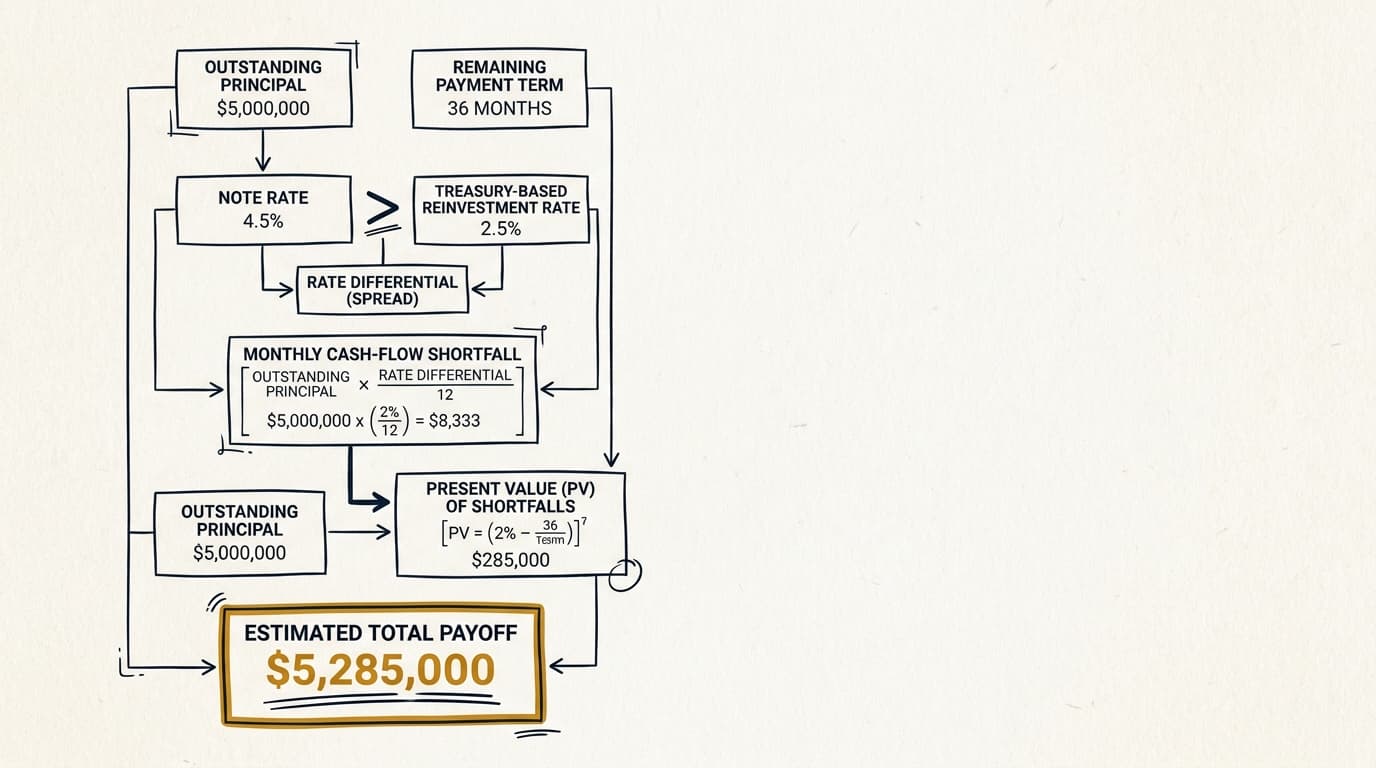

Yield maintenance is simpler. The loan gets prepaid, and the lender or trust receives a charge meant to cover reinvestment loss. For a broader foundation, see this overview of commercial real estate yield maintenance. If you need the math behind the spread and Treasury benchmark, the more detailed explanation of the yield maintenance formula breaks that out separately.

In practice, the first question usually is not which method a borrower likes better. It is which method the documents actually allow. Many securitized loans prohibit voluntary prepayment during a lockout period and then allow defeasance instead of open prepayment. According to the SEC-filed CMBS pooling and servicing agreement examples, securitized loan administration runs through detailed servicing standards and document requirements. In some deals, that makes defeasance the only realistic path before open prepayment becomes available.

Yield maintenance vs defeasance: side-by-side comparison

Yield maintenance is usually easier to document. Defeasance is usually harder to execute. Cost is the tricky part. There is no one-way rule here — either structure can come out cheaper depending on rates, loan spread, remaining term, and transaction fees.

| Issue | Yield Maintenance | Defeasance |

|---|---|---|

| Basic structure | Loan is prepaid and lender receives a prepayment premium | Loan stays outstanding and collateral is replaced with permitted securities |

| Main cost driver | Present value of lender's lost yield relative to benchmark rates | Cost of purchasing a defeasance portfolio that replicates scheduled debt service |

| Third-party fees | Usually lower | Usually higher due to legal, servicer, accountant, rating, brokerage, and successor borrower costs |

| Document complexity | Moderate | High |

| Common in CMBS | Sometimes, depending on open prepayment terms | Very common where documents permit defeasance after lockout |

| Closing timeline | Often shorter | Often longer because more parties must review and approve |

| Rate sensitivity | Highly sensitive to Treasury movements and contractual spread | Highly sensitive to securities market pricing and remaining payment schedule |

| Operational risk | Primarily quote accuracy and document interpretation | Includes securities settlement, entity formation, opinion delivery, and servicing coordination |

The cleanest way to compare them is to separate economics from execution. A structure that looks a little cheaper on paper may still be the worse choice if it puts a sale at risk or adds avoidable failure points.

When yield maintenance is usually cheaper

Yield maintenance often wins when open prepayment is allowed, the remaining term is not especially long, and third-party defeasance expenses would eat up too much of the savings. It also tends to make more sense when simplicity matters more than squeezing out a small pricing advantage.

Yield maintenance usually has the edge in a few common situations:

- Short remaining term. If only a limited number of payments remain, the added work and fees of building a defeasance portfolio may not pay off.

- Smaller balance loans. On lower-balance deals, fixed defeasance costs can take up a much larger share of the exit budget.

- Simple refinance timing. If the refinance lender wants a straightforward payoff and the existing documents allow it, yield maintenance cuts down the number of moving parts.

According to the Fannie Mae Multifamily lender resources, prepayment structures in commercial and multifamily lending can include yield maintenance, but the terms vary a lot by program and loan documents. That matters because borrowers sometimes fixate on the quote and miss the more basic issue: they may not even have the right to prepay yet.

A practical example: assume a $12 million fixed-rate loan with 18 months remaining until open prepayment, and defeasance fees projected at $85,000 to $140,000 including counsel, servicer review, securities brokerage, and accounting. If the yield maintenance premium is only modestly above par because benchmark rates have risen since origination, a direct payoff can be cheaper on an all-in basis even if the defeasance portfolio itself prices efficiently.

When defeasance is usually cheaper or more practical

Defeasance is often the practical answer when the loan is securitized, voluntary prepayment is blocked, and the documents specifically allow defeasance after a lockout period. It can also come out cheaper when the securities portfolio costs less than a yield maintenance premium that has grown in a lower-rate environment.

Borrowers usually end up in defeasance for one of four reasons:

- The documents require it. Many CMBS loans allow defeasance but not ordinary prepayment before a defined date.

- The trust wants payment continuity. Defeasance keeps the cash flow to bondholders in place by swapping collateral instead of retiring the debt.

- The sale has to happen before open prepayment is available. Waiting may not be realistic.

- The live quote is better. In some rate environments, the securities basket plus fees still beats yield maintenance.

According to the U.S. Department of the Treasury explanation of marketable Treasury securities, Treasury securities provide fixed payment obligations and active market pricing. That is why they are commonly used to fund defeasance when the documents require government-backed replacement collateral. The exact list of permitted securities depends on the loan documents and the securitization structure.

Defeasance is not just a cost calculation. It is a process, and sometimes an annoyingly detailed one. The borrower usually forms a successor borrower, transfers the defeased loan obligations, delivers legal opinions, funds the securities purchase, and coordinates with the master servicer, special servicer if applicable, trustee, securities intermediary, and counsel. So even if the economic quote looks slightly better, it may still be the wrong answer if the sale contract leaves no room for extra execution time.

CMBS loan scenarios where the decision changes

In CMBS loans, the answer can flip based on lockout terms, servicing instructions, and the remaining amortization schedule. Two loans with the same balance can produce very different results if one allows open prepayment in 90 days and the other forces defeasance for another 24 months.

Sale during lockout

A sale during lockout usually points to defeasance because voluntary payoff may be prohibited. According to Freddie Mac Multifamily Seller/Servicer Guide resources, prepayment and defeasance rights are document-driven and program-specific. You have to confirm the actual loan terms, not assume market practice will save you.

If the buyer will not assume the debt and the seller must deliver the property free and clear, defeasance may be the only route to closing before the lockout expires.

Refinance near the open prepayment window

A refinance close to the first open prepayment date may favor waiting and using yield maintenance, or possibly no premium at all, depending on the documents. The economics turn on carry costs, extension risk, and whether the new lender will hold pricing long enough.

This is where borrowers often get the analysis wrong. Waiting 60 to 90 days for a better prepayment window can save money, but only if the new loan spread, rate-lock extension fees, and property-level operating changes do not erase the savings.

Large-balance institutional asset sale

On a large loan, defeasance fees may matter less as a percentage of proceeds, which makes the securities economics the main variable. A $75 million office, industrial, or multifamily loan can absorb six-figure third-party costs more easily than a $4 million balance. In that situation, the all-in comparison often turns on rates rather than fixed transaction expense.

Cost drivers borrowers often underestimate

The biggest pricing mistakes usually come from second-order costs, not the headline premium. Borrowers fixate on the quoted penalty and miss servicing, legal, tax, and timing costs that can materially change net proceeds.

| Cost driver | Why it matters | More relevant to |

|---|---|---|

| Treasury or benchmark movements before lock | Quotes can move between underwriting and closing | Both |

| Master servicer and trustee fees | Administrative fees may be fixed or document-based | Defeasance |

| Borrower and lender counsel | Opinion letters, transfer documents, and review time add cost | Defeasance |

| Securities brokerage spread | The portfolio purchase includes execution costs and market pricing risk | Defeasance |

| Rate lock extension or sale delay | A slower exit can affect the replacement financing economics | Both |

| Spread maintenance language | Contract wording can materially affect the payoff amount | Yield maintenance |

| Accounting and tax treatment | Expense characterization may affect closing statement and reporting | Both |

One issue borrowers often miss is quote decay. A defeasance model can look cheaper based on a securities screen from last week, then flip the other way by the time documents are circulating.

Another is legal scope. According to the U.S. Securities and Exchange Commission explanation of asset-backed securities, securitized structures rely on pooled cash flows and trustee-administered payment mechanics. That is why CMBS exits tend to involve more institutional parties and more review than a balance-sheet loan payoff.

Closing timeline and transaction complexity

Yield maintenance closings are usually faster because the borrower is paying off the debt, not reworking collateral mechanics inside a securitized trust. Defeasance closings usually need more lead time because they depend on securities settlement, entity formation, servicer approval, and coordinated document delivery.

A useful working rule is to start a defeasance process several weeks before the target closing date, then confirm the actual lead time with counsel and the servicer. Timelines vary by document set, but the sequence is generally more involved than a standard payoff.

- Review the note, loan agreement, and servicing notices for defeasance conditions and timing limits.

- Request current instructions and a fee schedule from the master servicer.

- Engage defeasance counsel, securities professionals, and an accountant if the documents require one.

- Model both structures using current rates, remaining debt service, and all third-party costs.

- Align the sale or refinance closing date with the securities purchase and legal opinion timeline.

- Reconfirm final economics shortly before closing because market moves can change the result.

That procedural burden is one reason experienced borrowers usually start with a document abstraction and payoff workflow instead of jumping straight to quotes. On loans with fuzzy language, a clause-by-clause review may tell you whether there is even a real choice to compare.

How to compare yield maintenance vs defeasance before a sale or refinance

The right comparison is a transaction model, not a label. Borrowers should compare total dollars out, time to close, and failure risk under their actual loan documents and target closing date.

A practical decision framework looks like this:

| If this is true | Usually focus on | Why |

|---|---|---|

| Loan is CMBS and still in lockout | Defeasance feasibility first | Open prepayment may not be available |

| Loan can be prepaid now | Live all-in comparison | Either route may be cheaper |

| Closing must occur in less than 30 days | Execution risk and timeline | Operational simplicity may outweigh minor cost differences |

| Loan balance is relatively small | Fixed fee burden | Defeasance fees may represent a larger percentage of proceeds |

| Rates have fallen sharply since origination | Detailed quote analysis | Yield maintenance may become expensive |

| Open prepayment date is near | Wait-versus-close analysis | Short delay may reduce total exit cost |

This is where the analysis gets more useful than a standard servicer memo. The right answer is not always the lowest quoted premium. If a sale contract has hard outside dates, if a buyer wants certainty, or if replacement financing expires, the option with lower execution risk can produce better net proceeds even when its quoted premium is slightly higher.

Example: a borrower estimates defeasance at $410,000 and yield maintenance at $455,000. On paper, defeasance wins by $45,000. But if defeasance adds three weeks and the refinance lender charges a 25-basis-point extension fee on a $20 million replacement loan, that advantage may vanish. Add legal overages or a delayed tenant rollover, and the cheaper quote may stop being the better deal.

Common edge cases that change the analysis

Some edge cases can upend what otherwise looks like a straightforward comparison. They do not show up much in basic explainers, but they matter in live transactions.

Partial release or portfolio sale

A partial collateral release can complicate both structures because release provisions, allocated loan amounts, and servicer consent standards may not fit neatly with defeasance mechanics or payoff language. Borrowers selling one asset out of a portfolio should review release tests before modeling any prepayment strategy.

Assumption is available

If the buyer can assume the debt, neither yield maintenance nor defeasance may be the best answer. Assumption can preserve in-place financing economics, although lender and servicer approval, assumption fees, and buyer qualifications still matter.

Special servicing or default issues

A loan in default or transferred to special servicing may not follow the standard path. Extra approvals, workout discussions, or reserve issues can delay the exit or change the structure entirely.

Documents use unusual security eligibility rules

Not all defeasance clauses allow the same collateral basket. If the documents limit eligible securities more tightly than current market practice, the portfolio may cost more or require more customization than an initial quote suggests.

Conclusion

Yield maintenance vs defeasance is not a generic prepayment question. In commercial real estate, and especially in CMBS, the answer turns on document permissions, rate conditions, remaining term, fixed transaction fees, and how much time you have to close. Borrowers should compare live all-in costs for both structures, confirm which options the note and servicing regime actually permit, and treat timing risk as part of the economics, not as a separate legal footnote.

For broader context on prepayment structures, start with commercial real estate yield maintenance. If the open question is how the premium itself is calculated, review the dedicated guide to the yield maintenance formula. Those pages cover the underlying mechanics. This comparison becomes most useful once an actual sale or refinance date is on the table.

Frequently Asked Questions

Is defeasance always used instead of yield maintenance in CMBS loans?

No. Some CMBS loans permit open prepayment after a lockout or during a specified window, while others rely mainly on defeasance before maturity. The controlling source is the loan documents and servicer instructions, not a general market rule.

Which is usually cheaper: yield maintenance or defeasance?

Either can be cheaper. Yield maintenance may cost less when the loan can be prepaid directly and fixed defeasance fees are high relative to the balance. Defeasance may cost less when the securities portfolio required to replicate debt service is cheaper than the prepayment premium. You need a current side-by-side quote because rates and fees move.

How long does a defeasance closing usually take compared with yield maintenance?

Yield maintenance payoffs are usually faster because they involve a direct loan payoff. Defeasance often takes longer because it requires securities purchases, legal opinions, successor borrower formation, and servicer coordination. Exact timing depends on the servicer, document set, and transaction complexity.

Do regional factors change yield maintenance vs defeasance costs?

Yes, but usually through transaction expenses rather than the core prepayment economics. Legal fees, local counsel needs, state transfer or entity filing costs, and closing practice differences can affect all-in defeasance expense in markets such as New York, California, Texas, or Florida. The benchmark-rate component of yield maintenance is generally driven by the loan documents and Treasury-based pricing, not the property's location.

Can a borrower decide between yield maintenance and defeasance without reading the loan documents?

No. The note, loan agreement, and servicing provisions determine whether prepayment is allowed, when defeasance is permitted, what fees apply, and what securities qualify. A preliminary quote without document review can send you in the wrong direction.