Yield Maintenance Accounting Tax Treatment Guide

Yield maintenance payments usually count as debt extinguishment costs for book purposes, but the tax treatment depends on the borrower’s facts, deal structure, and reason for paying off the loan early. This article explains how finance teams typically classify the charge, what U.S. GAAP says, and what CFOs should confirm with auditors and tax advisors before close.

When a borrower prepays a fixed-rate commercial mortgage, yield maintenance usually gets booked in the payoff period with the rest of the debt retirement costs. For finance teams, the accounting under U.S. GAAP is usually pretty clean. The tax treatment is where things get messy. It turns on the loan documents, the deal structure, and why the debt came off the books in the first place. This article covers yield maintenance accounting tax treatment for CFOs, controllers, and asset managers who need a close file they can defend and a short list of smart questions for advisors.

Key Takeaways

- Yield maintenance is usually analyzed as a debt extinguishment cost for book purposes, not as an asset tied to new financing.

- Under FASB ASC 470-50 on debt modifications and extinguishments, amounts paid to repurchase or retire debt generally hit current earnings when extinguishment accounting applies.

- Tax treatment is more fact-specific. Borrowers usually want to know whether the payment is currently deductible, must be capitalized, or should be treated as interest, and the answer can change with the transaction.

- IRS Notice 2008-27 makes the point plainly: federal tax treatment of certain debt prepayment penalties depends on the facts and the Code provisions in play.

- A solid quarter-end file should include the note, payoff statement, treasury screen support if relevant, legal settlement statement, and a memo that ties the accounting conclusion to the actual transaction facts.

Yield maintenance accounting tax: the short answer

Yield maintenance is usually a lender charge for retiring debt before maturity, and borrowers generally evaluate it as part of debt extinguishment accounting for financial reporting. For tax, the payment is often tested under rules for interest, debt retirement costs, or transaction costs. The answer depends on whether the payoff happened in a refinancing, sale, exchange, assumption, or broader restructuring.

That matters because book and tax often part ways. A controller may book the amount immediately as extinguishment loss under U.S. GAAP, while the tax team still has to decide whether that same payment is deductible now, deferred, or allocated somewhere else.

How yield maintenance is commonly classified in financial reporting

In practice, many borrowers record yield maintenance as a loss on extinguishment of debt when the original loan is legally repaid and removed from the balance sheet. The accounting file usually groups the charge with write-offs of unamortized deferred financing costs, legal fees tied to the retirement, and any lender exit fees listed in the payoff letter.

FASB ASC 470-50 says an extinguishment occurs when a debtor is legally released as the primary obligor under the liability. And under FASB ASC 405-20 on extinguishments of liabilities, the gain or loss is measured by comparing the reacquisition price of the debt with its net carrying amount.

For a typical CRE payoff, the net carrying amount may include:

- Outstanding principal

- Unamortized deferred financing costs

- Unamortized original issue discount or premium, if applicable

- Accrued interest through payoff date

The reacquisition price usually includes the cash paid to retire the debt. That is where yield maintenance normally enters the analysis. If the payoff is final and the old debt is gone, borrowers usually recognize the charge in current-period earnings instead of carrying it as an asset.

That is different from a debt modification that does not qualify as an extinguishment. Under FASB guidance on the 10 percent cash flow test in ASC 470-50, a refinancing with the same lender may require modification analysis rather than extinguishment accounting. Finance teams should not assume yield maintenance or similar fees automatically go through extinguishment loss without checking the legal form and the cash flow test result.

If you need the broader mechanics, Graphline’s overview of commercial real estate yield maintenance explains when the charge shows up in a CRE payoff. The page on yield maintenance loan documents shows where the controlling clause usually sits in the note and mortgage package.

Where U.S. GAAP points on debt extinguishment costs

U.S. GAAP does not have a special model just for yield maintenance. It drops the charge into the existing debt extinguishment framework. The real question is simple: is this payment part of what the borrower paid to retire the debt?

PwC’s financing guide discussion of debt extinguishments and Deloitte’s roadmap on debt extinguishments both point in the same direction: in an extinguishment, fees paid to the existing lender are typically part of the extinguishment gain or loss calculation, while costs tied to new debt are treated separately.

| Item | Common book treatment in a full payoff | Why finance teams treat it that way |

|---|---|---|

| Yield maintenance payment | Current-period extinguishment loss | It is part of the amount paid to retire old debt |

| Unamortized deferred financing costs on old loan | Write off to extinguishment loss | Old borrowing no longer exists |

| Legal fees for payoff | Usually current expense or part of extinguishment analysis based on facts | Directly tied to the retirement transaction |

| Fees on new replacement debt | Capitalize and amortize under debt issuance cost guidance | They relate to the new borrowing, not the retired one |

This split matters in refinance transactions. If the borrower pays yield maintenance to exit the old loan and also pays fees to close replacement debt, those amounts usually end up in different places in the close package. The first usually goes through extinguishment loss. The second is usually deferred and amortized over the new term.

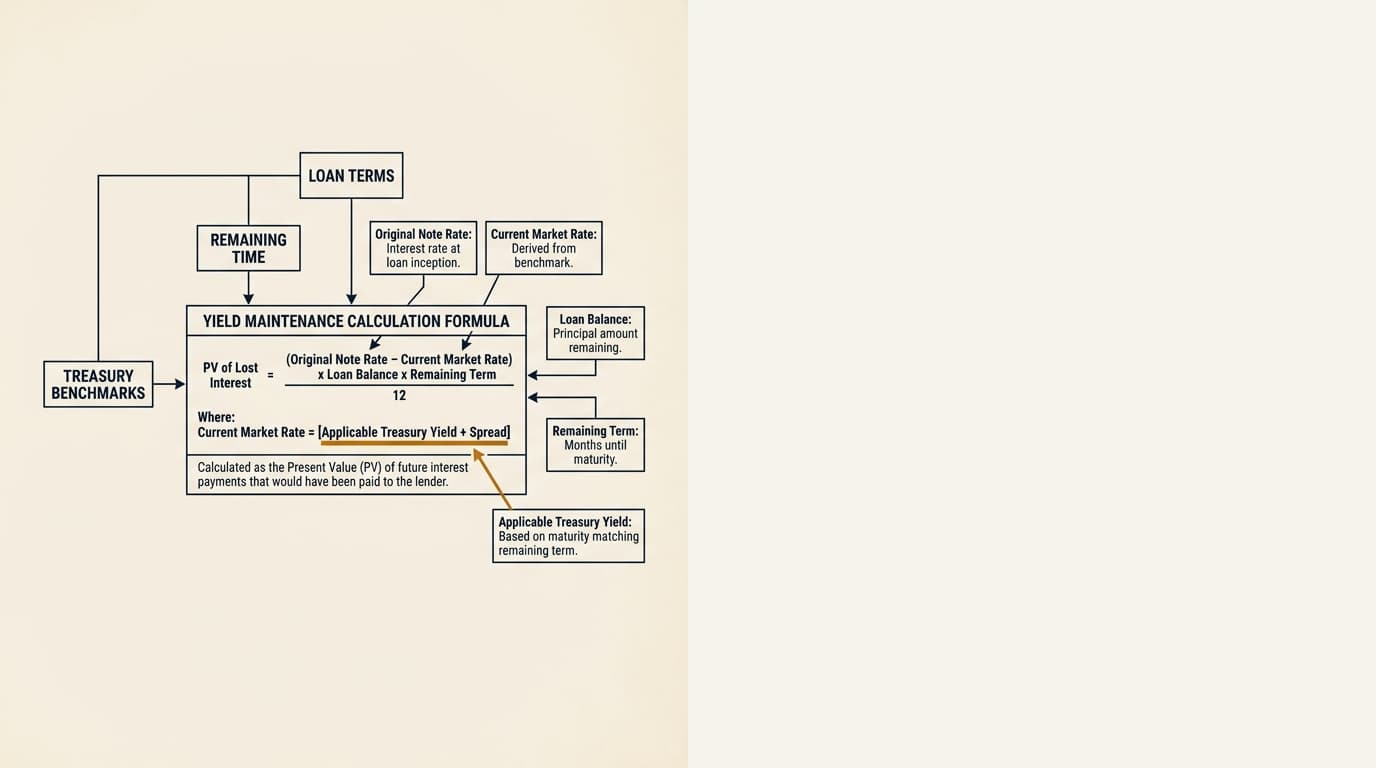

One practical point: keep the accounting memo separate from the payoff math. The supporting pages on yield maintenance formula and yield maintenance calculation example are useful for checking the lender’s numbers, but they do not answer the classification question on their own.

Yield maintenance tax treatment: common borrower positions and open questions

Federal income tax treatment of yield maintenance is more fact-driven than the book entry. Borrowers usually ask whether the payment is deductible as interest or a borrowing cost, whether it has to be capitalized into a sale or new financing, and whether related-party or REMIC structures change the answer.

IRS Notice 2008-27 regarding prepayment penalties and interest characterization says some prepayment penalties may count as interest for federal income tax purposes, but that conclusion depends on the legal rights and economics of the payment. Internal Revenue Code Section 163 governs interest deductions and their limits. Treasury Regulation Section 1.263(a)-5 on facilitative transaction costs may require capitalization for amounts paid to facilitate certain acquisitions, restructurings, and financings.

So the tax file should answer at least four questions:

- Is the payment really additional interest on the retired debt, or is it better treated as a retirement cost or transaction cost?

- Did the payoff happen as part of a taxable asset sale, a like-kind exchange analysis that later changed, a refinance, or an internal restructuring?

- Does any part of the payment belong with the new financing rather than the retired financing?

- Do interest limitation rules, including Section 163(j), limit a current deduction even if the payment is characterized as interest?

For CMBS borrowers, servicing structure can make the tax analysis harder because the payoff package may break out yield maintenance, special servicing, legal review, and remittance timing as separate line items. Those should not be lumped together just because they all appear on the same statement. The article on cmbs yield maintenance explains why the tax team should sort those items before assigning treatment.

Decision framework: expense now, capitalize, or analyze further

Most close files benefit from a basic screening framework before auditors and tax advisors get involved. The point is not to replace technical advice. It is to get the transaction into the right workstream early, before the team posts the wrong entry and has to unwind it later.

Scenario 1: Full third-party payoff and new loan

A borrower repays Lender A in full, pays yield maintenance, and closes a separate loan with Lender B. Book accounting usually points to extinguishment loss on the old debt and capitalization of issuance costs on the new debt.

Tax teams then look at whether the yield maintenance payment is deductible now and whether that deduction is limited or deferred by the surrounding facts.

Scenario 2: Refinance with same lender

A same-lender refinancing may require modification-versus-extinguishment analysis before the accounting is settled. If the transaction is not a legal extinguishment, the treatment of fees can change in a meaningful way.

This is where teams get sloppy. Controllers should review the legal release, note cancellation, and cash flow test support before posting a clean extinguishment entry.

Scenario 3: Property sale with debt payoff

When a property sale triggers the payoff, the book entry may still treat yield maintenance as a debt extinguishment cost. Tax may go a different direction. The team may need to consider whether the amount affects amount realized, deductible financing cost treatment, or transaction-cost capitalization. The sales agreement and settlement statement usually decide more than people expect.

Where assumption is allowed, the economics can shift. The page on yield maintenance assumption sale explains when a buyer’s assumption may avoid the payoff charge entirely.

Scenario 4: Exit structure alternatives

Some borrowers compare yield maintenance with other exit structures before deciding whether to refinance or sell. That starts as an economics question, but accounting and tax belong in the model too. Two options can have similar cash costs and very different income statement and tax results.

For side-by-side exit analysis, see yield maintenance vs defeasance, yield maintenance vs step-down, and yield maintenance refinance or sale.

Journal entry example for a CRE payoff with yield maintenance

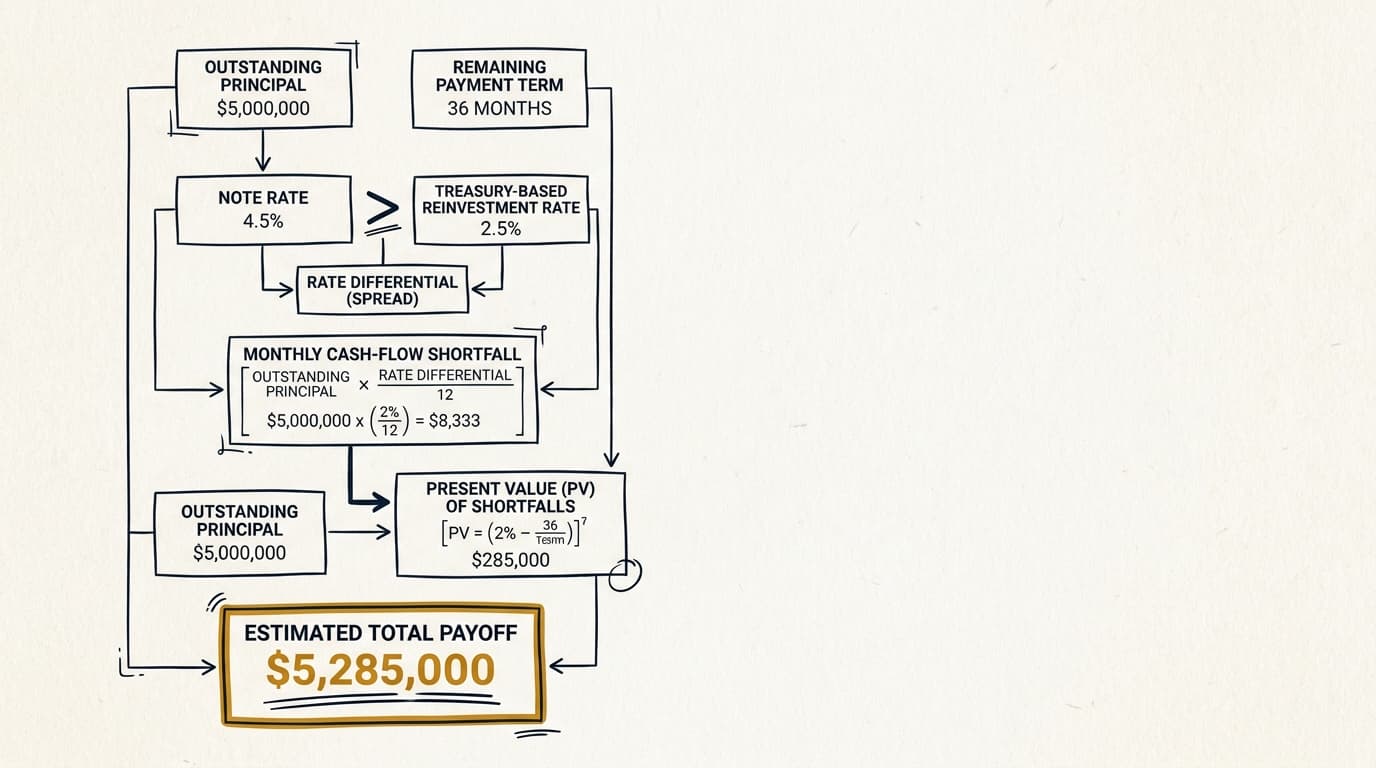

A simple example shows why the charge usually hits current earnings for book purposes. Assume a borrower pays off a mortgage with $10,000,000 principal outstanding, $120,000 of unamortized deferred financing costs, and a $640,000 yield maintenance charge.

| Account | Debit | Credit |

|---|---|---|

| Mortgage payable | $10,000,000 | |

| Loss on extinguishment of debt | $760,000 | |

| Deferred financing costs | $120,000 | |

| Cash | $10,640,000 |

This example is simplified. Accrued interest, escrow adjustments, lender legal fees, and cutoff dates may require separate entries. If the borrower closes replacement financing at the same time, new debt issuance costs are usually recorded separately from the extinguishment entry.

What to collect before quarter-end close

Controllers can cut down the audit back-and-forth by building the support package before posting the entry. In a lot of files, the missing piece is not the payoff quote. It is the memo that explains why the quote was treated that way.

- Obtain the executed note, all amendments, and the payoff statement showing each fee line.

- Separate principal, accrued interest, yield maintenance, legal fees, servicer fees, and escrow refunds into distinct workpaper lines.

- Determine whether the transaction is a legal extinguishment or requires modification analysis under ASC 470-50.

- Write off or defer financing-related balances based on whether they attach to the old or new debt.

- Prepare a tax memo identifying the proposed characterization of the payment and the authorities reviewed.

- Confirm whether sale accounting, assumption rights, or related-party issues change the analysis.

- Retain treasury rate support and lender correspondence if the payoff formula references Treasury inputs.

If payoff figures keep getting disputed, compare the lender’s statement against the governing clause in the yield maintenance loan documents and any benchmark details in the yield maintenance treasury rate provision. That sounds obvious, but teams often skip it until the numbers stop tying out.

Frequently Asked Questions

Is yield maintenance an expense or a balance sheet asset for book accounting?

In a full payoff that qualifies as debt extinguishment, borrowers usually record yield maintenance in current-period earnings as part of loss on extinguishment of debt. Fees on the new loan are usually analyzed separately and deferred over the term of the replacement financing.

Is yield maintenance tax deductible?

Sometimes, but not by default. Tax advisors usually analyze whether the payment is interest, a debt retirement cost, or another transaction cost, and whether rules such as Section 163 or the capitalization regulations affect timing. The answer depends on the transaction facts and the entity structure.

Does the accounting change if the borrower refinances with the same lender?

It can. A same-lender refinance may require modification-versus-extinguishment analysis under U.S. GAAP, including the 10 percent cash flow test and a review of the legal release terms. If the old debt is not extinguished, lender fees may be treated differently than they would in a third-party payoff.

How should CMBS borrowers treat separate servicer and legal line items on the payoff statement?

Analyze them separately. A CMBS payoff may include yield maintenance, special servicing charges, counsel fees, and remittance-related items, and those categories do not necessarily get the same accounting or tax treatment.

Does state location matter for yield maintenance tax treatment?

Yes, potentially. Federal income tax rules drive the main characterization issues, but state conformity varies, and apportionment rules can change the cash tax result. Multistate owners should confirm whether the property state and the filing state conform to the relevant federal provisions as of 2026.