Yield Maintenance Assumption Sale: Can It Avoid the Penalty?

A sale can avoid yield maintenance through loan assumption only if the loan documents allow it and the lender approves the buyer, the transfer structure, and the credit profile after closing. In practice, assumption usually turns a prepayment issue into an underwriting and consent issue.

Many commercial mortgages with yield maintenance can also be transferred through a loan assumption, but only if the lender signs off and the buyer clears underwriting. So a yield maintenance assumption sale does not magically erase a prepayment charge. It works only when the note, mortgage, and transfer language allow the debt to stay in place through closing.

Here’s the practical question: can the buyer step into the existing loan without tripping the lender’s transfer restrictions? That is what determines whether yield maintenance gets avoided. This article covers when that works, what lenders and servicers usually want to see, and where these deals tend to break down. It also walks through the real trade-offs for owners bringing an encumbered property to market in 2026, especially timing, buyer-pool limitations, and document problems worth catching before a purchase agreement is on the table.

Key Takeaways

- Assumption can avoid a yield maintenance charge because the loan is not being prepaid, but only if the loan documents allow assumption and the lender approves the transfer.

- Lender review usually centers on buyer net worth, liquidity, property cash flow, entity structure, guarantees, and post-transfer debt service coverage.

- Assumption requests often come with assumption fees, lender counsel fees, updated legal opinions, reserve true-ups, and deadlines that can push closing out by several weeks.

- CMBS and balance-sheet loans can both permit assumption, but CMBS transfers usually involve stricter servicing procedures and longer consent timelines.

- The first step is document review: owners should inspect yield maintenance loan documents before marketing the asset, not after signing a purchase agreement.

What a yield maintenance assumption sale usually means

A yield maintenance assumption sale is a property sale where the buyer takes over the seller’s existing loan instead of paying it off at closing. If the debt stays outstanding and the lender consents to the transfer, yield maintenance usually does not apply because there has been no prepayment.

That rule comes from the contract, not market habit. According to Regulation Z under the Consumer Financial Protection Bureau, assumptions are a recognized credit event in mortgage regulation, but commercial loan transfer rights are governed mainly by negotiated loan documents, not by any universal assumption rule. In CRE, the controlling documents are the promissory note, mortgage or deed of trust, loan agreement, guaranty, and any securitization servicing provisions.

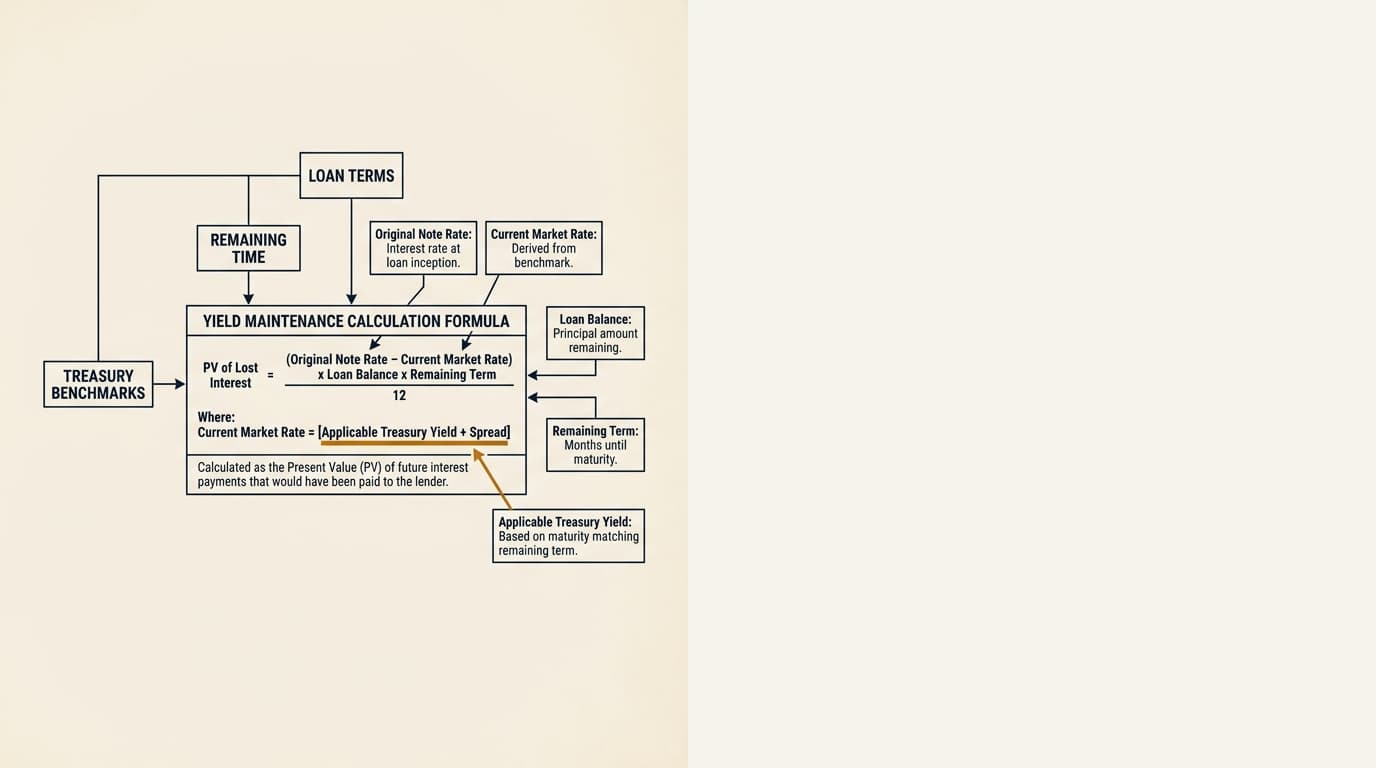

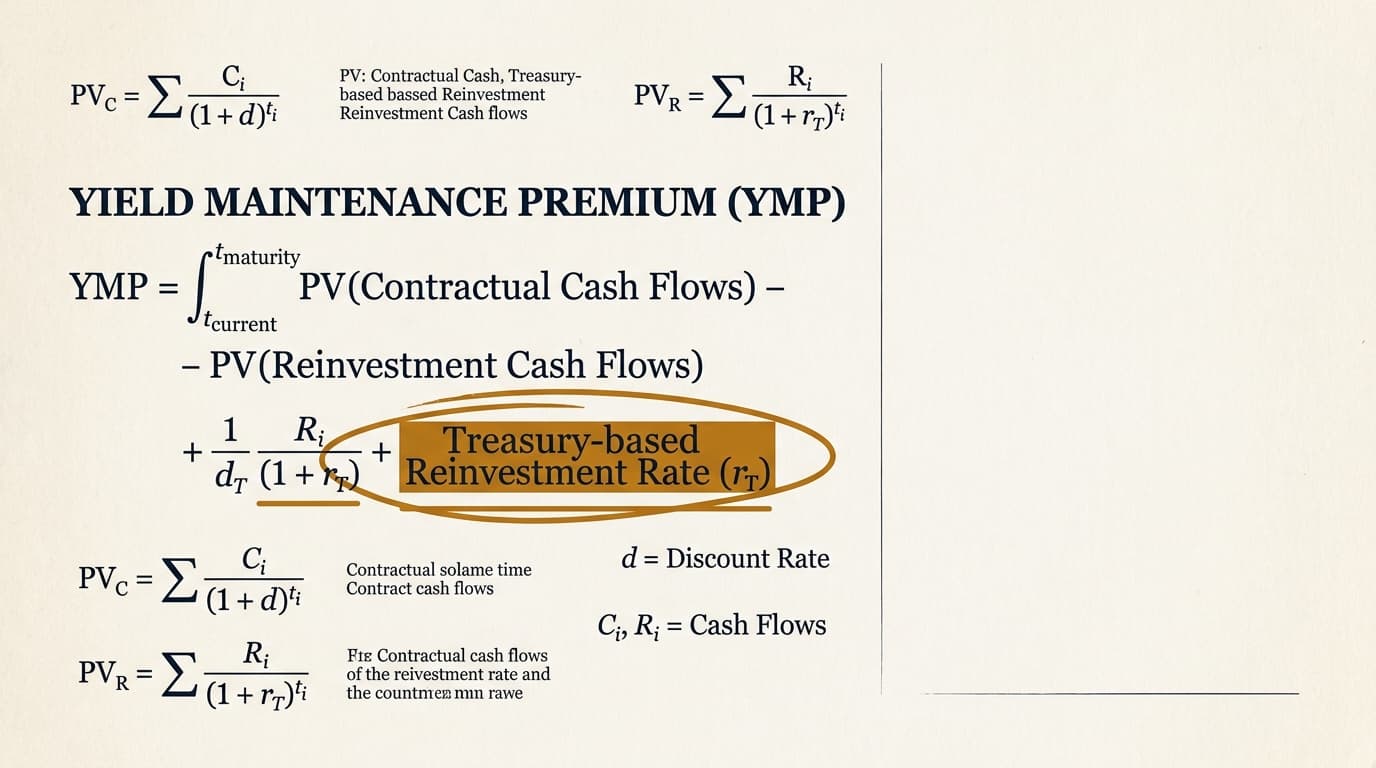

In plain terms, the seller is trying to swap a potentially expensive exit charge for a transfer approval process. Sometimes that trade is worth it. Sometimes it is not. For background on how these penalties work, see commercial real estate yield maintenance. For a more technical breakdown of the payoff math, Graphline readers can compare this issue with the separate yield maintenance formula discussion.

When assumption can avoid yield maintenance

Assumption can avoid yield maintenance when the loan stays in place through closing and the transfer fits the lender’s assumption rules. The legal point is straightforward: yield maintenance is usually a prepayment premium, and an approved assumption avoids prepayment.

According to Freddie Mac servicing guidance on transfers of ownership and loan assumptions, multifamily assumptions require prior written approval and satisfaction of program conditions. According to Fannie Mae Multifamily transfer and assumption guidance, delegated servicers must evaluate borrower qualifications, property performance, and transfer structure before approval. Those agency rules are not identical to private-label bank or debt-fund documents, but the pattern is the same: assumption is allowed only on stated conditions, and lender approval is discretionary.

Typical assumption-friendly scenarios include:

- A fixed-rate loan with several years left to maturity and a below-market coupon that buyers actually want.

- A note that expressly permits assumption with lender consent and payment of fees.

- A buyer with strong liquidity and net worth compared with the outstanding principal balance.

- A single-asset transfer with no messy changes to property management, tenancy profile, or ownership chain.

Common failure points include lockout language, springing recourse issues, prohibited transfers of controlling interests, or a lender view that the replacement borrower is weaker than the current one. In CMBS deals, the path can be even narrower because the pooling and servicing agreement may leave little room for negotiated exceptions. That is why owners often compare assumption with yield maintenance vs defeasance and with more focused analysis of cmbs yield maintenance.

What lenders review before approving an assumption

Lenders usually underwrite an assumption almost like a new borrower request tied to an existing loan. The review is not just about buyer credit. It also asks whether the transfer changes collateral risk, legal enforceability, or servicing complexity.

According to Fannie Mae Multifamily guidance for assumptions and transfers, servicers review borrower financial capacity, property operations, organizational documents, and replacement guarantor strength where relevant. According to Freddie Mac’s transfer approval standards, assumption packages may require updated financial statements, organizational charts, legal opinions, and proof of acceptable management and property condition.

Buyer credit and liquidity

Most lenders require the assuming borrower and its principals to meet minimum net worth and liquidity thresholds. A common market convention is net worth at or above the loan amount and liquidity equal to a set percentage of the outstanding balance, although exact thresholds vary by lender and often are not published.

That matters because assumption can shrink the buyer pool fast. A buyer may have enough equity to buy the asset and still fail assumption underwriting because post-closing liquidity is thin or guarantor support falls short of the lender’s standards.

Property performance and DSCR

The property usually still has to support the debt under current underwriting metrics. If occupancy has dropped, a major tenant rolled, or trailing net operating income no longer supports the loan, the lender may reject the assumption even if the buyer looks strong on paper.

According to the Federal Deposit Insurance Corporation’s 2023 statement on prudent CRE loan accommodations and workouts, lenders are expected to evaluate repayment capacity, collateral protection, and borrower performance using updated, well-supported analysis. That approach affects bank-held loan transfers even when the documents technically permit assumption.

Legal structure and transfer chain

Entity structure is where a lot of these deals get bogged down. Lenders typically want formation documents, certificates of good standing, beneficial ownership information, organizational charts, non-consolidation opinions in some structured finance deals, and confirmation that no prohibited transfer has already happened.

One recurring problem is a sale built around upstream equity transfers instead of a deed transfer. Loan documents often define “transfer” broadly enough to capture changes in direct or indirect control, so parties should not assume that selling membership interests gets around consent requirements.

Transfer conditions that often block assumption

Most denied assumptions fail because of document conditions, timing problems, or economics, not because assumption is inherently unavailable. Sellers should expect the lender’s consent rights to be detailed and procedural.

| Condition | What it usually means in practice | Effect on sale timeline |

|---|---|---|

| Prior written consent | No transfer can close until formal lender or servicer approval is issued | Often adds several weeks |

| Assumption fee | Borrower pays a stated fee, often plus third-party review costs | Increases closing costs |

| Lender counsel fees | Seller or buyer reimburses document drafting and review | Can be material in CMBS and large-balance loans |

| Reserve funding true-up | Tax, insurance, TI/LC, or replacement reserves may need adjustment | May require additional cash at closing |

| No default condition | Any monetary or non-monetary default can suspend approval | Can stop the transaction entirely |

| Replacement guaranty requirements | Bad-boy or carveout guarantors may need to be replaced or supplemented | Requires principal-level diligence |

According to Fannie Mae Multifamily’s assumption requirements, lenders may require outstanding issues to be cured before approving a transfer. According to Freddie Mac’s transfer procedures, assumptions require complete submissions and satisfaction of all stated conditions before consent is granted.

This is where owners need to separate assumption from other exit options. If the deal cannot absorb a longer consent process, the real comparison is not just payoff economics. It is certainty of execution. That trade-off comes up in yield maintenance refinance or sale and, for other prepayment structures, yield maintenance vs step-down.

Assumption vs paying off the loan: a decision framework

Assumption makes the most sense when the prepayment cost you avoid is larger than the extra friction, fees, and buyer constraints created by lender approval. The analysis should combine economics, timing, and buyer-qualification risk. Looking only at the headline penalty is where people get sloppy.

That broader view is often missing from lender summaries. A useful framework looks like this:

| Scenario | Assumption usually makes more sense when | Payoff usually makes more sense when |

|---|---|---|

| Below-market loan coupon | The loan is attractive financing for buyers and supports pricing | Buyer has cheaper debt available elsewhere |

| Large expected prepayment charge | Estimated yield maintenance would materially reduce seller proceeds | Penalty is modest or near open/prepay window |

| Short closing deadline | Buyer and lender are already familiar and package can be submitted quickly | The sale requires certainty within 30 days or less |

| Complex buyer structure | Ownership is simple and guarantors are strong | Fund, JV, or foreign ownership requires extended diligence |

| Property performance volatility | NOI and occupancy are stable and support current debt | Recent leasing loss may trigger lender concerns |

Example: a seller with a $12 million fixed-rate loan at 4.10% and three years left may find assumption attractive if current market debt for the same buyer prices above that rate and the expected payoff charge is large. But if the property has a pending anchor rollover or the buyer is using a layered joint-venture structure, assumption can become much less reliable even if the savings look good at first glance.

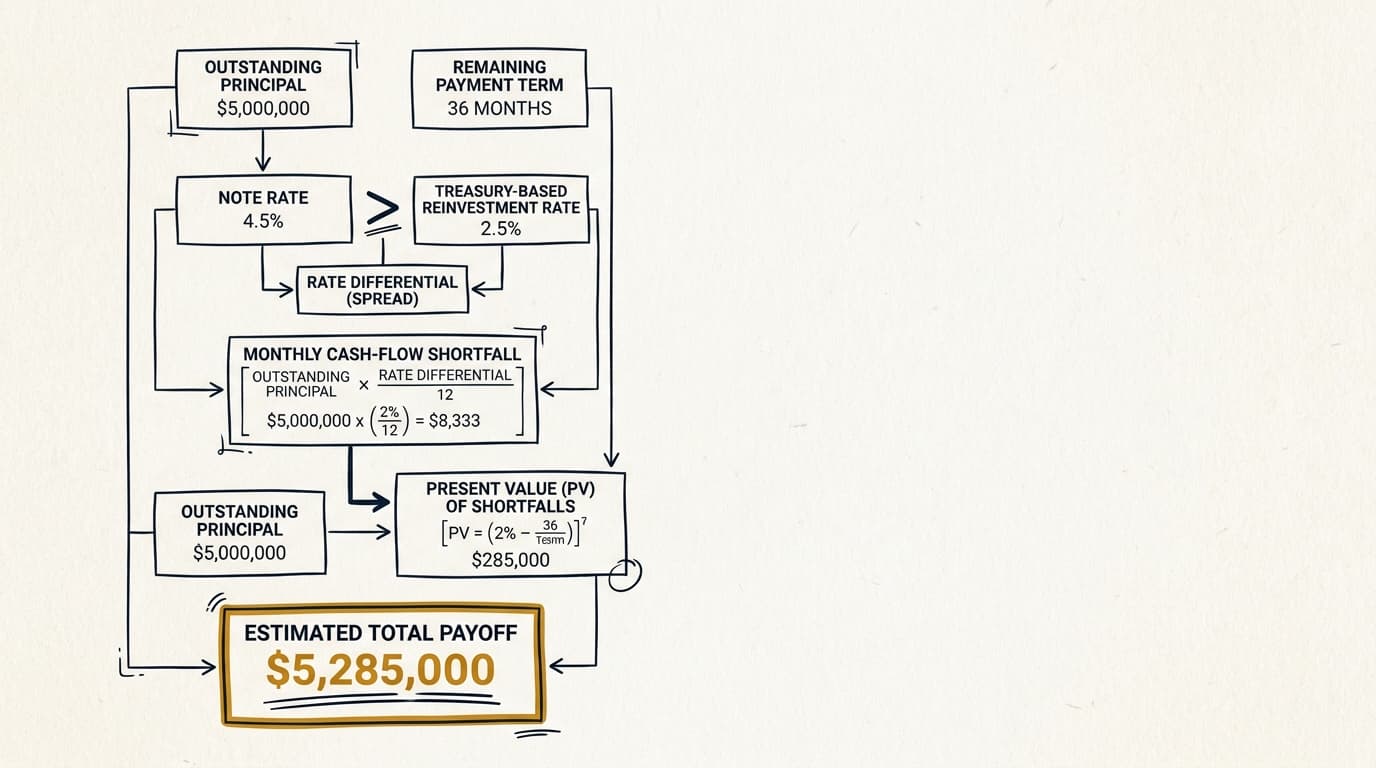

Owners evaluating the payoff side should review an actual yield maintenance prepayment penalty analysis and a numerical yield maintenance calculation example. Treasury moves matter too, because lower benchmarks can increase the charge. That piece is covered separately in the yield maintenance treasury rate discussion.

How to evaluate an assumption sale before going to market

The right time to test assumption is before the listing goes live. Waiting until the contract stage often means there is not enough time to assemble lender materials, negotiate buyer structure, and fix document problems.

- Review the note, mortgage, loan agreement, guaranty, and transfer provisions for assumption rights, prohibited transfers, lockouts, and fee language.

- Get a preliminary read from counsel or the servicer on whether the proposed sale structure fits the assumption clause.

- Estimate the alternative payoff cost so the deal can compare assumption savings against timing and approval risk.

- Screen likely buyers for liquidity, net worth, and organizational complexity before marketing assumption as a selling point.

- Build extra time into the purchase agreement for lender consent, third-party reports, and legal documentation.

- Confirm who pays assumption fees, lender counsel fees, reserve adjustments, and transfer taxes before signing the PSA.

For owners dealing with timing close to maturity, check the related analysis on yield maintenance before maturity. Many loans loosen up as the penalty period gets close to ending, and that can change the answer.

Frequently Asked Questions

Can a property sale avoid yield maintenance by having the buyer assume the loan?

Yes, often. If the buyer assumes the existing loan and the lender or servicer approves the transfer, the debt usually is not being prepaid, so yield maintenance generally does not apply. The answer depends on the exact transfer and prepayment language in the loan documents.

Does a lender have to approve a commercial loan assumption?

Usually yes. Commercial mortgage assumptions typically require prior written lender or servicer consent. Agency and securitized loans commonly require a full application package, underwriting review, legal review, and payment of assumption-related fees before approval is issued.

How long does a commercial real estate loan assumption take?

The timeline varies by lender and deal complexity, but assumption usually takes longer than a simple payoff because it requires buyer underwriting and legal documentation. Balance-sheet lenders may move faster than CMBS or agency executions, while complex ownership structures or unresolved property issues can drag the process out further.

Are CMBS loan assumptions harder than bank loan assumptions?

Often yes. CMBS assumptions usually run through servicer procedures, counsel review, and securitization constraints that leave less room to speed things up. In many bank portfolio loans, the lender still has broad consent rights, but the path to approval can be more direct than in a securitized transfer.

Do assumption rules vary by property type or market?

Yes. Multifamily agency loans follow program-specific transfer standards, while office, retail, industrial, and hospitality loans may be governed by lender-specific documents and different views of cash-flow stability. Market conditions matter too. In weaker leasing markets, lenders may look much harder at tenant rollover, occupancy, and debt service coverage before approving a transfer.