Yield Maintenance Before Maturity: When It Applies

Yield maintenance before maturity usually applies when a commercial borrower prepays during the protected period set out in the note, but the answer turns on the loan’s lockout language, any open-period provisions, defeasance terms, and any negotiated exceptions.

Most commercial mortgages charge yield maintenance before maturity only if you prepay during the protected period spelled out in the note or loan agreement. That sounds straightforward until you look at the actual documents. In real deals, the payoff result usually comes down to three things: whether the loan is still in a lockout, whether it has moved into an open period near maturity, and whether the documents make room for casualty, condemnation, assumption, or lender-approved release exceptions.

This article shows how to tell whether yield maintenance before maturity will be charged on a planned payoff, sale, or refinance in 2026. The focus is the note language that controls timing, the exceptions that can change the outcome, and the review steps borrowers should take before ordering a payoff statement.

Key Takeaways

- Yield maintenance before maturity is controlled by the note and related loan documents, not by any universal market rule.

- Many commercial loans use a lockout period, then a yield maintenance period, then an open period in the final 60 to 180 days before maturity, but the timing depends on the deal.

- CMBS loans often limit prepayment more heavily; according to Fannie Mae Multifamily guidance on prepayment premiums, structured prepayment protection can include lockouts, yield maintenance, or defeasance depending on the execution.

- Common exceptions include casualty, condemnation, certain assumptions, and lender-approved partial releases, but only when the documents say so.

- Borrowers should compare the note, loan agreement, and any rider against the draft payoff quote before wiring funds.

Yield maintenance before maturity: direct answer

Yield maintenance before maturity usually means a prepayment charge applies if the loan is paid off before the stated maturity date and before any contractual open period starts. The point is simple: if a fixed-rate loan gets taken out early, the lender wants compensation for the lost yield.

Freddie Mac Multifamily Seller/Servicer Guide provisions on prepayment provisions show that multifamily fixed-rate loans may use lockouts, defeasance, or yield maintenance depending on the product. Fannie Mae Multifamily Servicing guidance on prepayments says the same thing in practical terms: prepayment rights depend on the loan documents and may be limited by timing restrictions and premium formulas. Those agency guides are not private-label templates, but they make the core point clearly. Prepayment protection is contractual, and timing usually decides the result.

For borrowers, the real distinction is between legal maturity and the period of economic protection. A loan can be six months from maturity and still carry yield maintenance if the note says the premium runs until a later date. The reverse is also true. A loan can still be outstanding before maturity but freely prepayable if it has already entered an open period.

For broader context on structure and terminology, see commercial real estate yield maintenance.

How lockout periods and open periods change the payoff result

Lockout periods prohibit or sharply limit prepayment for a set period. Open periods do the opposite. They allow payoff near maturity without yield maintenance, sometimes with only notice requirements or a modest administrative fee.

A common sequence in commercial notes looks like this: first, no prepayment during an initial lockout; next, prepayment is allowed with yield maintenance after the lockout ends; finally, free prepayment during the last window before maturity. That last window is often called an open period, although documents may instead say "without premium," "par window," or "open prepayment period."

Lockout period

A lockout period is the hardest prepayment restriction in the loan. During that period, the note may bar voluntary payoff altogether except for narrow exceptions written into the documents.

Consumer Financial Protection Bureau guidance on prepayment penalties notes that prepayment restrictions and charges depend on contract terms. In CRE loans, lockout clauses are often stricter than what borrowers are used to in consumer lending. If a refinance or sale is scheduled during a lockout, the borrower may need to delay the closing, structure the deal as an assumption, or use defeasance if the documents permit it. On CMBS loans, that usually calls for a separate review of cmbs yield maintenance and, where relevant, yield maintenance vs defeasance.

Yield maintenance period

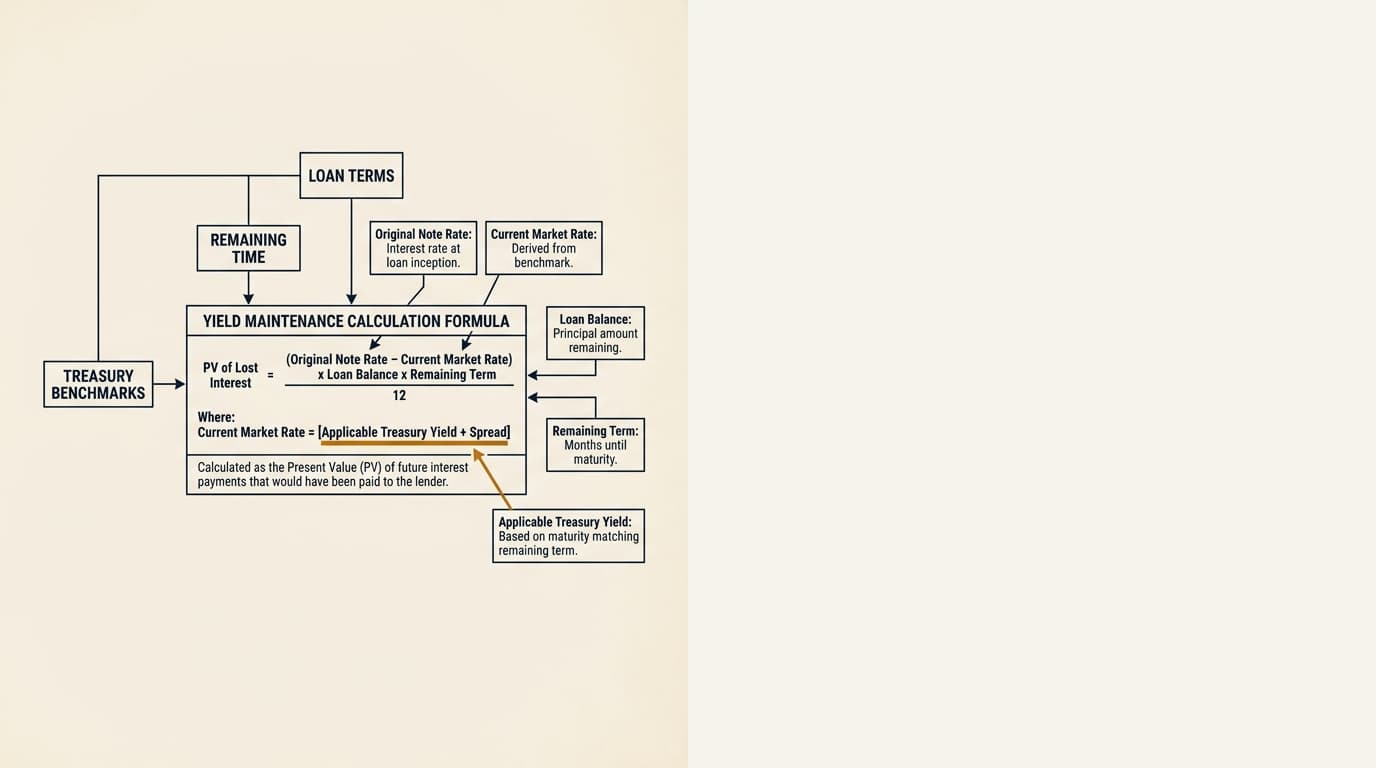

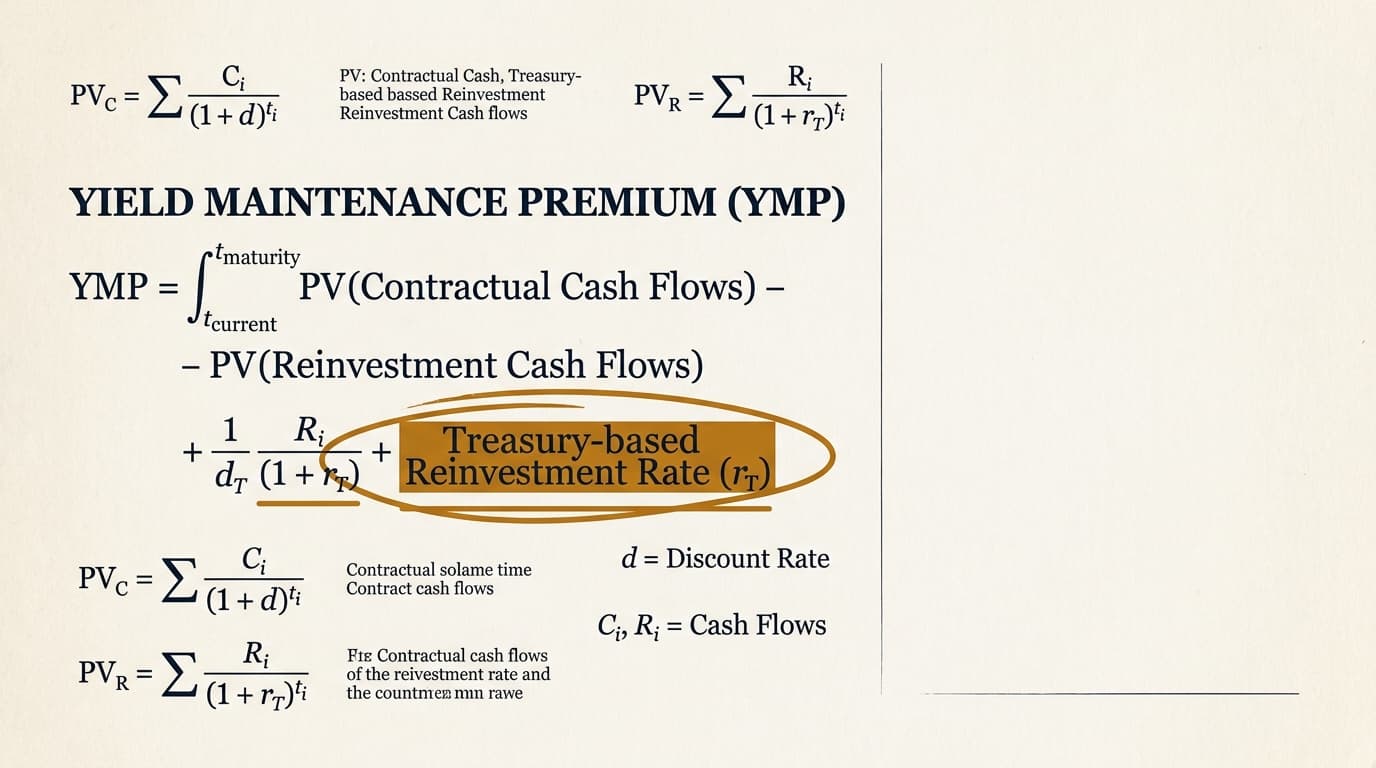

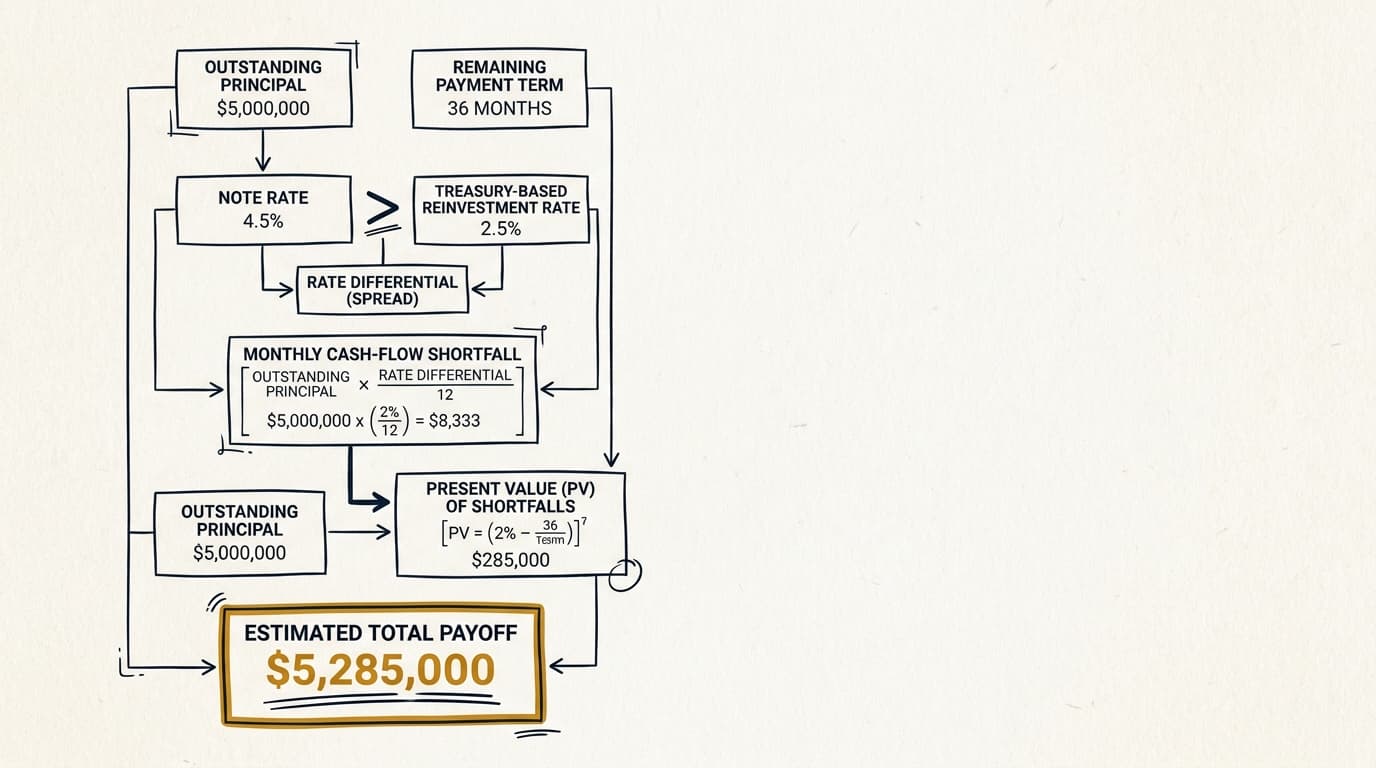

The yield maintenance period is the stretch after any lockout and before any open period when voluntary prepayment is allowed only if the borrower pays a premium. That premium is usually tied to the difference between the note rate and a Treasury-based reinvestment rate.

If the borrower pays off during this period, the payoff statement will usually include outstanding principal, accrued interest, servicing fees if applicable, and the yield maintenance amount. For the calculation mechanics, see the dedicated explanation of the yield maintenance formula and a worked yield maintenance calculation example.

Open period before maturity

An open period is a defined window before maturity when the borrower can prepay without yield maintenance. In many fixed-rate commercial loans, that window is shorter than people expect.

Open periods often appear in the final 90, 120, or 180 days before maturity, but there is no standard rule. Some notes have no open period at all. Others allow prepayment at par only if the borrower gives advance notice, stays current on all obligations, and pays on a scheduled payment date. That is why moving a payoff date by even a week can change the economics in a meaningful way.

| Timing provision | Typical effect before maturity | What to verify |

|---|---|---|

| Lockout | Voluntary prepayment prohibited or heavily restricted | Exact end date, permitted exceptions, assumption rights |

| Yield maintenance period | Payoff allowed only with premium | Formula source, Treasury benchmark, notice rules |

| Open period | Payoff allowed at par or near par | Start date, notice period, payment-date limitations |

Where to confirm whether yield maintenance applies before maturity

You almost never get the answer from a single clause. Whether yield maintenance applies before maturity usually depends on reading the note together with the loan agreement, rider, mortgage or deed of trust, and any servicing transfer or securitization provisions.

The best starting point is the prepayment section of the promissory note. That section often defines prohibited periods, premium periods, benchmark rates, minimum spread floors, and any final open window. But the important carve-outs may sit elsewhere. Assumption language may be in the loan agreement. Casualty and condemnation rules may be in the security instrument. Securitized loans may add servicer consent requirements or timing conventions in servicing documents.

Borrowers looking at this issue should start with the full set of yield maintenance loan documents. Cornell Law School Legal Information Institute guidance on promissory notes explains the general principle: repayment rights and obligations are defined by the documents. In CRE practice, that usually means the note comes first, but related loan documents can still change how an apparent right works in the real payoff process.

Common exceptions that can eliminate or reduce the charge

Exceptions are common enough to matter, but they are never implied. The safer assumption is that yield maintenance applies before maturity unless the documents clearly create an exception.

Casualty and condemnation

Casualty and condemnation proceeds are often treated differently from voluntary prepayment. Some notes waive yield maintenance if insurance or condemnation proceeds are applied after a total loss or a taking that requires payoff.

Freddie Mac Multifamily servicing guidance on condemnation and casualty events shows that special servicing treatment can apply when collateral is materially affected. Private-label loans vary, but many follow the same basic logic: involuntary events may bypass some voluntary prepayment restrictions. Partial takings and partial casualty restorations are trickier. The lender may allow restoration, require a partial principal curtailment, or keep the right to apply proceeds without opening a full prepayment option.

Assumption

Assumption can avoid an early payoff altogether. If a buyer takes over the existing loan with lender approval, yield maintenance may never be triggered because the debt is not being prepaid.

This is highly fact-specific. Assumptions usually require underwriting, legal review, assumption fees, replacement guaranties, and a timeline that can run longer than a standard sale closing. Some notes prohibit assumption during lockout or after securitization. Others allow it only on specific conditions. A borrower looking at a sale should compare the net economics of payoff versus assumption in a separate review of yield maintenance refinance or sale.

Lender-consented release or modification

A lender may agree to a partial release, collateral substitution, or modification that changes the payoff result. But that relief has to be negotiated. It is not automatic.

In practice, portfolio lenders often have more flexibility than securitized lenders. CMBS structures usually route decisions through servicing standards and investor protections, which narrows the room for waivers. Typical pooling and servicing agreement provisions filed with the U.S. Securities and Exchange Commission show why: servicers are bound by deal documents and certificateholder standards. That is a big reason exceptions are harder to get in securitized loans.

Timing scenarios: refinance, sale, casualty, condemnation, and assumption

The same loan can produce different answers depending on why the payoff happens and exactly when it is scheduled. The practical question is not just whether the loan is before maturity. It is whether the loan is before maturity and still inside a protected period.

| Scenario | Will yield maintenance before maturity usually apply? | Main issue |

|---|---|---|

| Refinance during yield maintenance period | Usually yes | Premium amount may offset refinance savings |

| Sale during lockout | Often no voluntary payoff right | Delay closing, seek assumption, or pursue permitted alternative |

| Sale during open period | Often no premium | Confirm notice and payment-date conditions |

| Total casualty requiring payoff | Sometimes exempt | Check involuntary-prepayment carve-out |

| Condemnation with partial taking | Mixed outcome | Documents may require curtailment rather than full payoff |

| Buyer assumption | Potentially no payoff premium | Lender approval and timing risk |

Rate conditions matter here too. If the note allows prepayment with yield maintenance and Treasury rates have fallen since origination, the premium may be much higher because the lender's reinvestment shortfall is larger. The benchmark issue is covered separately in yield maintenance treasury rate.

A practical review framework for planned payoffs before maturity

Borrowers can usually get a good read on the likely payoff result before ordering a formal statement if they review the timing provisions in order. The goal is to confirm whether the planned closing date falls inside a lockout, a yield maintenance period, or an open period, and then test for exceptions.

- Locate the prepayment clause in the note and identify the exact maturity date.

- Mark any lockout expiration date and any open-period start date stated in the documents.

- Confirm whether prepayment is allowed only on scheduled payment dates or only after advance notice.

- Review stated exceptions for casualty, condemnation, assumption, defeasance, or lender-approved releases.

- Check whether the loan is portfolio, agency, or securitized because servicing rules may affect execution timing.

- Request a draft payoff statement and compare the quoted charge to the contractual language.

- Re-run the economics if the closing can be pushed into an open period or restructured as an assumption.

This framework does not replace counsel or servicer confirmation, but it usually surfaces the decisive issue early: not just whether the loan is before maturity, but whether the planned payoff date falls inside the premium window. For transaction teams, that timing point often decides whether a refinance closes this quarter or waits for the open period. For payoff math examples, see yield maintenance prepayment penalty.

Frequently Asked Questions

Does yield maintenance always apply if I pay off a loan before maturity?

No. Yield maintenance before maturity applies only if the loan documents impose it for the planned payoff date and transaction type. Some loans are in lockout, some allow prepayment only with a premium, and some enter an open period shortly before maturity when the premium no longer applies.

How close to maturity does an open period usually start?

There is no universal standard. In commercial practice, open periods often begin 60, 90, 120, or 180 days before maturity, but some notes have no open period at all. The promissory note and related loan documents control the answer.

Can casualty or condemnation proceeds avoid yield maintenance?

Sometimes. Many commercial notes treat involuntary prepayments differently from voluntary ones, especially after a total casualty or a condemnation that requires payoff. Partial takings and partial casualty events are less predictable and often lead to curtailment or lender-controlled application of proceeds instead of a full waiver.

Is the answer different for CMBS loans?

Often yes. CMBS loans usually have tighter timing rules, less waiver flexibility, and servicing requirements that make a pre-maturity payoff harder to execute. In some deals, defeasance becomes the main exit route after lockout instead of a simple cash prepayment.

Does location change whether yield maintenance applies before maturity?

Usually less than borrowers expect. The main driver is the contract language, not the property location. State law can affect enforcement, remedies, and foreclosure-related issues, but whether a planned payoff triggers yield maintenance is usually determined first by the note, loan agreement, and any securitization servicing framework.