Yield Maintenance Borrower Negotiation: Key Clauses

Yield maintenance costs are usually locked in by the loan documents before closing. Borrowers, brokers, and counsel should pay close attention to spread floors, open-period language, Treasury selection, and assumption rights, because those terms often decide whether a future sale or refinance comes with a manageable prepayment cost or a seven-figure bill.

The biggest leverage point in a yield maintenance borrower negotiation usually shows up before the loan ever closes: the draft prepayment language that circulates before rate lock. Once the note, loan agreement, and rider are signed, the payoff math follows the paper, not anyone's memory of the business discussion. This article walks through the yield maintenance provisions borrowers should mark up before closing, with close attention to spread floors, open-period language, Treasury definitions, and assumption rights.

For a broader overview of commercial real estate yield maintenance, including when it applies and how it compares with other exit structures, start with the pillar guide. For document location and clause hierarchy, see this guide to yield maintenance loan documents.

Key Takeaways

- Borrowers need to negotiate the yield maintenance clause before closing, because later payoff calculations turn on the signed note, rider, and Treasury definition.

- A spread floor can push prepayment costs much higher when rates fall by stopping the discount rate from dropping below a set minimum.

- An open period of 90 to 180 days before maturity can preserve refinance or sale flexibility that otherwise disappears until the final payoff window.

- Assumption rights often matter more than the headline spread language, especially in a sale where the buyer may be willing to take the existing debt.

- Small definition changes, including Treasury index selection, reinvestment spread, and notice timing, can move payoff cost by hundreds of thousands of dollars on larger balances.

What to negotiate in a yield maintenance clause before closing

From the borrower's side, the job is to negotiate the variables that control exit cost, not just the note rate. In practice, that means reading the note, prepayment rider, and assumption provisions together instead of marking up one clause in isolation.

According to Freddie Mac seller-servicer guidance on prepayment premium structures, multifamily loan documents may include yield maintenance, defeasance, lockout periods, and open periods, with timing and mechanics set by the governing documents. According to Fannie Mae Multifamily guidance on prepayment premium and yield maintenance concepts, prepayment terms are document-specific and have to be analyzed against the note and rider. That's the real point in negotiation: this is not an abstract market concept. It is a drafted allocation of risk.

The borrower-side priority order

The most useful markup sequence is economic variables first, exit rights second, and administrative mechanics third. Borrowers who spend time on notice periods and consent wording while leaving the benchmark spread untouched may clean up the process and still lose on economics.

- Negotiate the spread floor or remove it.

- Add or widen the open period.

- Preserve assumption rights with objective standards.

- Define the Treasury benchmark precisely.

- Limit lockouts, defeasance conversions, and partial-prepayment prohibitions where possible.

- Require a transparent payoff statement methodology and supporting calculation.

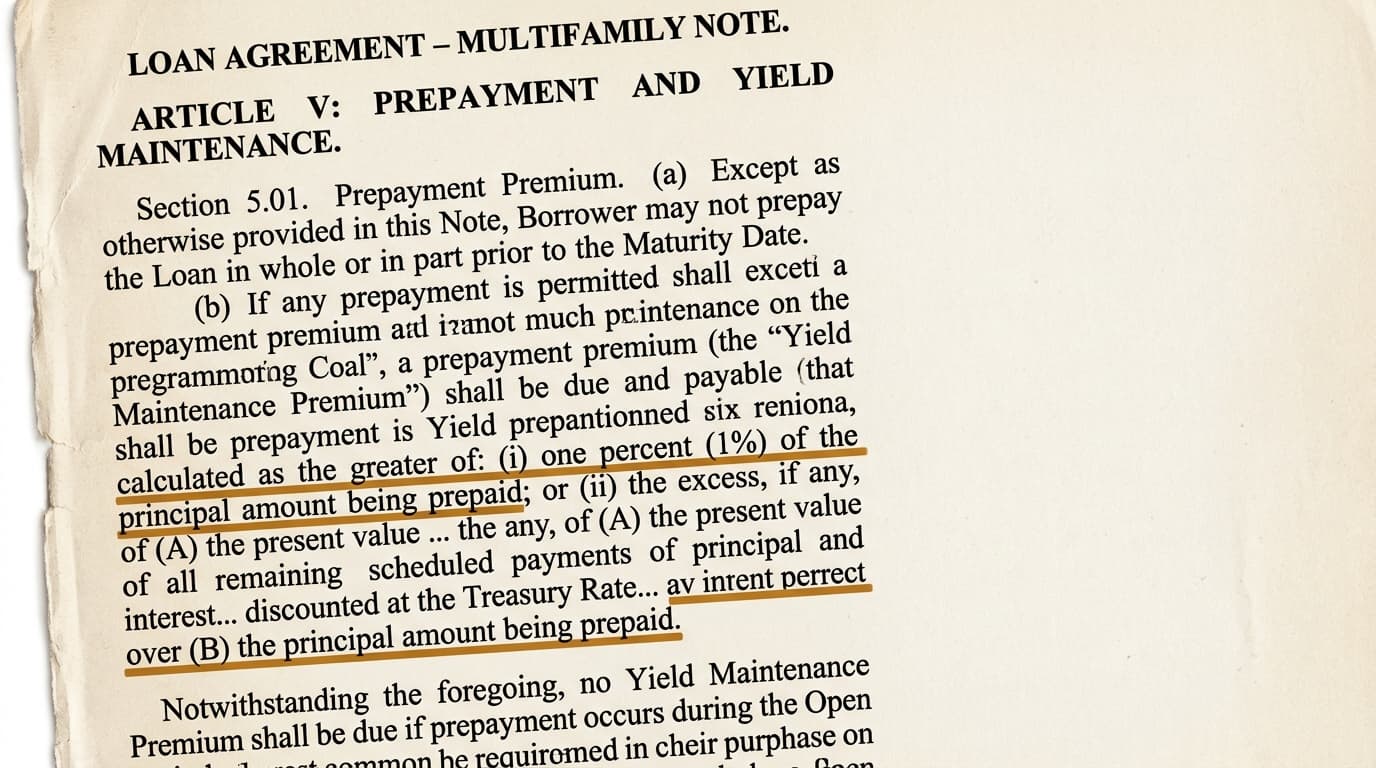

Spread floors: the borrower issue most likely to change payoff economics

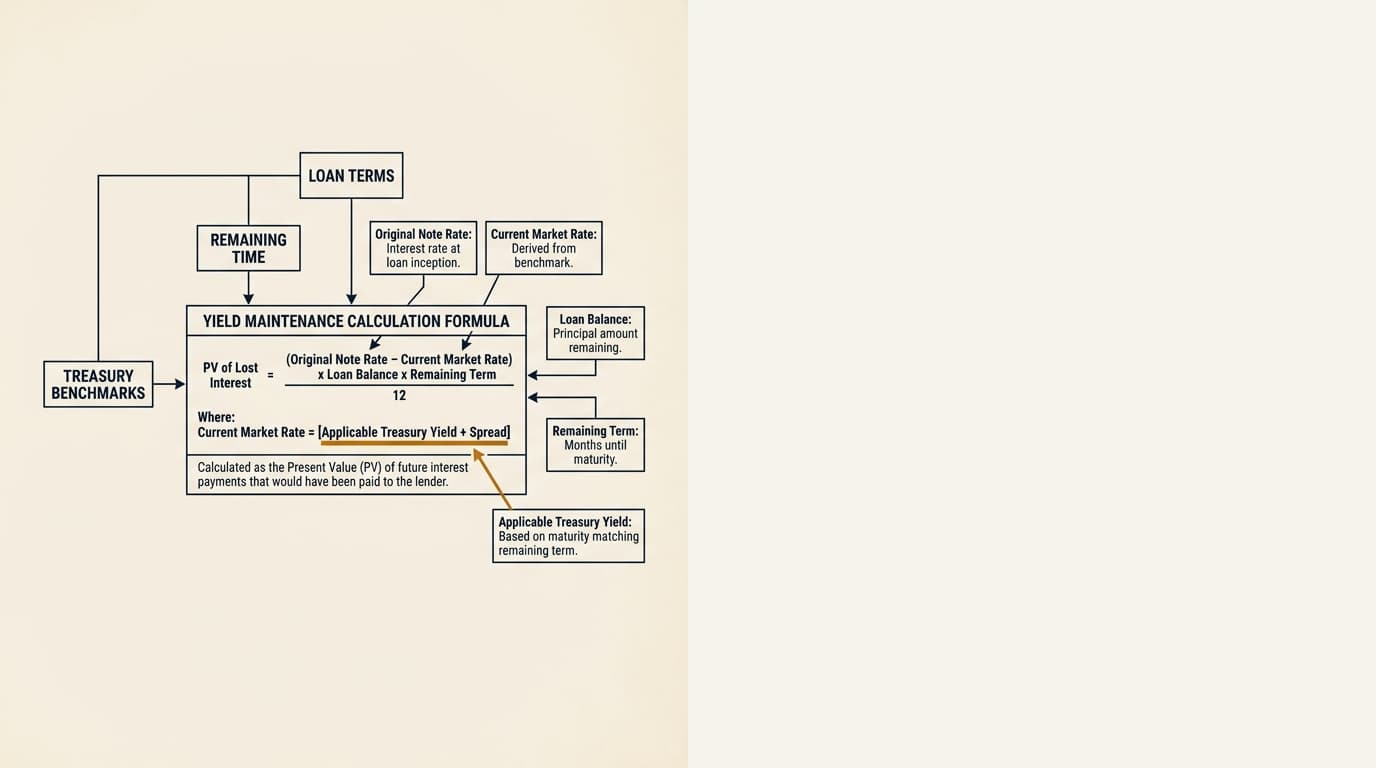

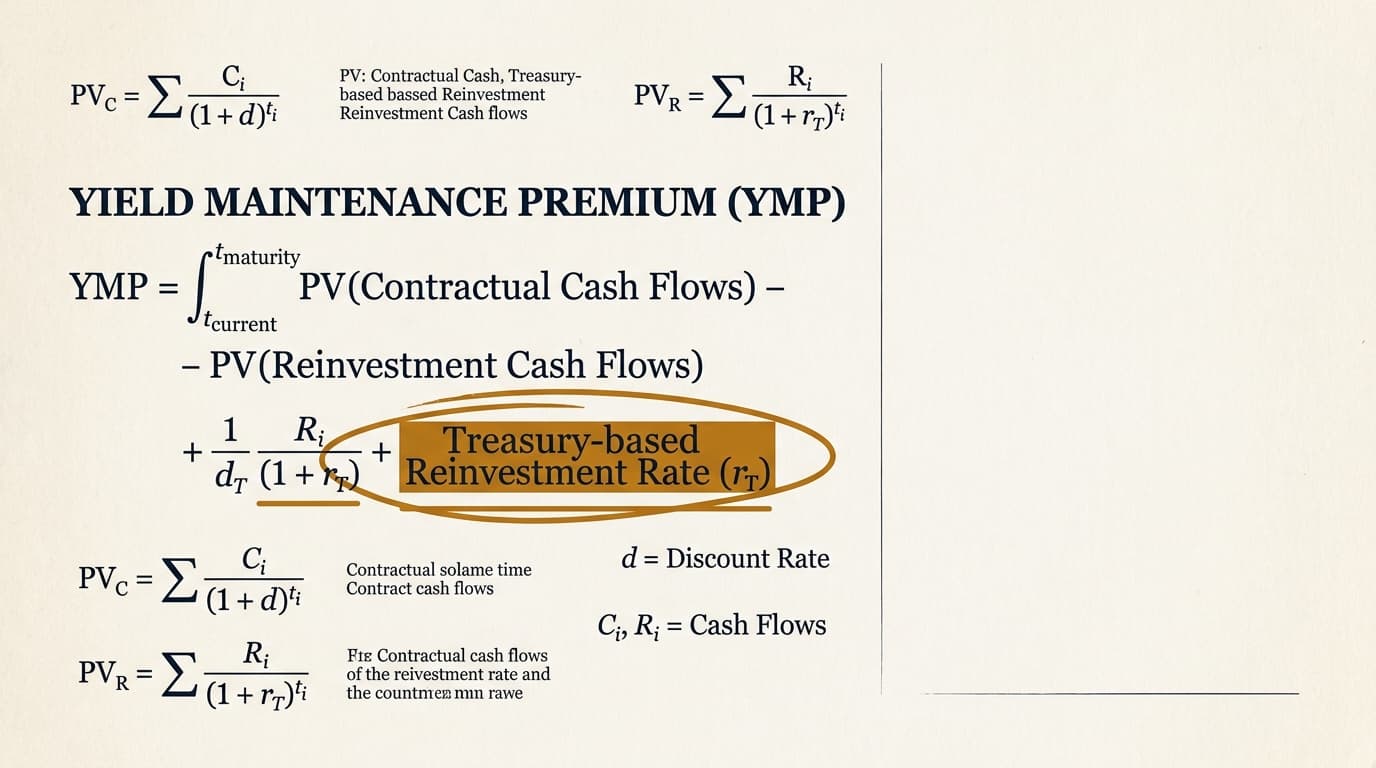

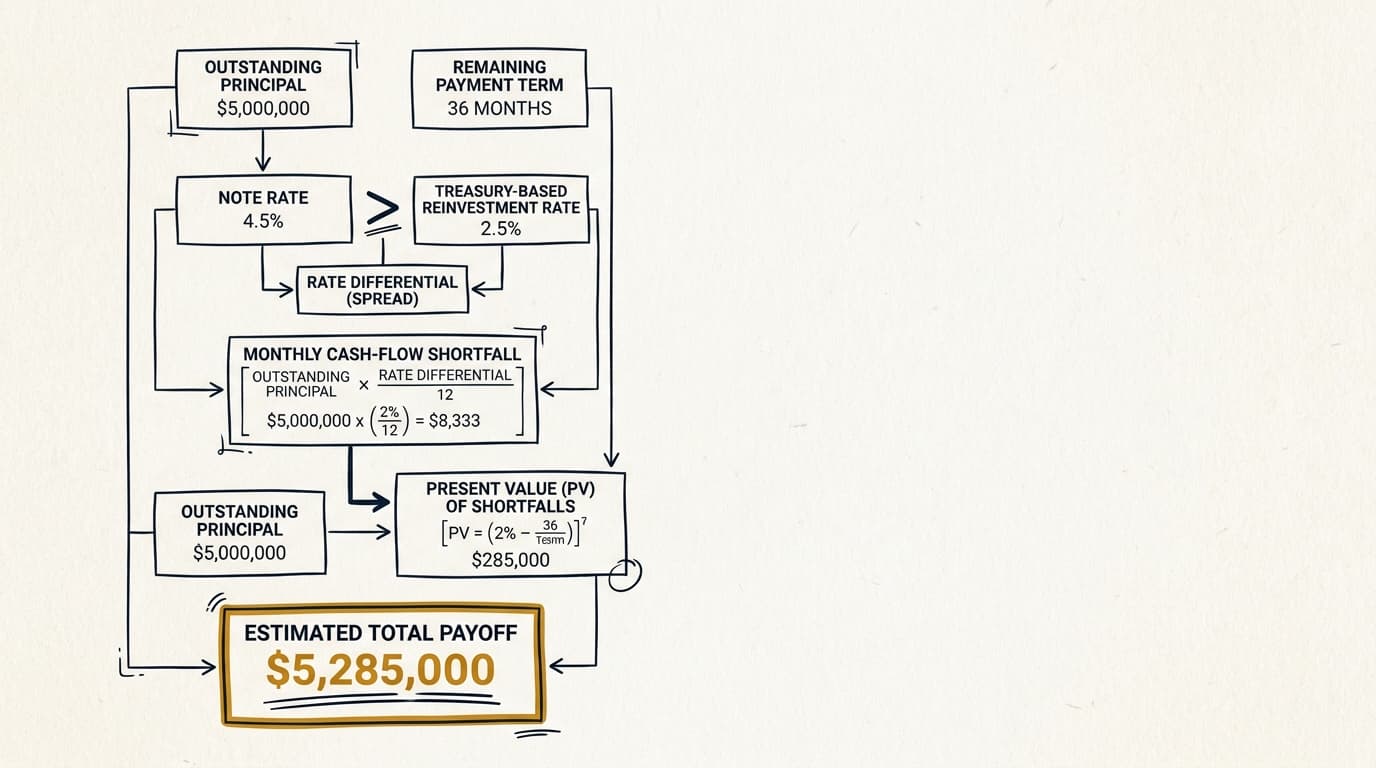

A spread floor sets a minimum reinvestment spread or discount-rate component in the yield maintenance formula. If Treasury yields fall, the floor can stop the lender's assumed reinvestment rate from moving with the market. That usually means a larger premium.

According to Fannie Mae Multifamily's yield maintenance calculation overview, yield maintenance generally compares scheduled loan cash flows to a reinvestment rate based on a Treasury yield plus a spread defined in the documents. For borrowers, the negotiation issue is straightforward: does that spread move with the benchmark, or does a floor keep the lender's economics artificially favorable when rates drop?

| Provision | Borrower-favorable language | Borrower risk if omitted |

|---|---|---|

| Reinvestment spread floor | No floor, or a low stated floor tied to actual benchmark mechanics | Premium may stay high even when Treasury yields move in the borrower's favor |

| Minimum prepayment premium | Cap at a fixed percentage or limited months of interest | Loan may require the greater of the formula amount or a high fixed minimum |

| Benchmark selection | Use the Treasury closest to average life or remaining term, stated precisely | Lender may choose a lower benchmark that increases the premium |

In real underwriting, a 25 to 50 basis point drafting change matters. On a $20 million loan with several years left, a lower assumed reinvestment rate can widen the present-value gap between note-rate cash flows and replacement Treasury yields by a lot. Borrowers reviewing the economics should also look at a separate breakdown of the yield maintenance formula and a worked yield maintenance calculation example.

Open-period language: the clause that can preserve refinance and sale flexibility

An open period allows prepayment without yield maintenance during a stated window before maturity, often 90, 120, or 180 days. Without it, a borrower can stay trapped in a premium almost until payoff, even when the business plan calls for an ordinary refinance near maturity.

According to Fannie Mae Multifamily servicing guidance, open periods and prepayment windows are dictated by the loan's contractual prepayment structure. According to Freddie Mac servicing references on prepayment structures, lockout and open-period treatment depends on product and document terms. So borrowers should ask for express language. Do not assume that a prepayment close to maturity will be exempt.

What open-period language should say

The clause should state the exact duration, whether notice is required, and whether the premium disappears entirely or drops to a nominal administrative fee. Vague wording around "final months" or language "subject to lender requirements" leaves room for a fight later.

For sponsors planning a sale or refinance, this provision can be worth more than a small note-rate concession. A transaction delayed by 60 days may slip from a free prepayment window back into a premium-bearing period if the clause is drafted badly. For timing issues tied to payoff date, see this analysis of yield maintenance before maturity and this comparison of yield maintenance refinance or sale.

Assumption rights: the most practical exit right borrowers often under-negotiate

An assumption right can be the cleanest way to avoid a prepayment premium on a sale. If the buyer can assume the loan under objective standards, the seller may preserve value even when rates have fallen and a cash payoff is expensive.

According to Regulation Z assumptions guidance under 12 CFR 1026.36, assumption treatment depends on creditor review and contractual rights, though commercial loans sit outside the consumer mortgage framework. For CRE drafting, the useful lesson is procedural: assumption rights should be written through objective approval tests, transfer fees, response deadlines, and release language, not left to broad lender discretion.

The markup points that matter most

Borrowers should ask for standards the lender can apply consistently. A clause that permits assumption only with lender consent "in its sole discretion" does not give much real protection.

- Objective net worth and liquidity thresholds for the transferee

- Fixed review periods, such as 15 to 30 business days after a complete package

- Specified transfer or assumption fees rather than open-ended reimbursement language

- Clear standards for release of the original borrower and guarantor

- Permission for common SPE ownership transfers that do not change control

Assumption rights matter even more when the alternative is a yield maintenance vs defeasance analysis or a sale structure constrained by servicing rules in cmbs yield maintenance. For sale-specific structuring, see yield maintenance assumption sale.

Treasury benchmark and calculation definitions: small drafting changes with large pricing effects

The benchmark definition decides which Treasury yield goes into the formula and when that yield is measured. Borrowers should insist on precision here because a vague benchmark clause gives the administrative party room to choose among inputs that all sound plausible but produce different economics.

According to the U.S. Department of the Treasury daily treasury par yield curve rates, Treasury rates are published by tenor and change daily. A note that references the Treasury "closest to the remaining average life" may produce a different result from one that references the Treasury "closest to the remaining term to maturity." That distinction gets missed all the time in negotiations and usually becomes visible only when the payoff statement shows up. For more on benchmark selection, see yield maintenance treasury rate.

Drafting questions counsel should answer before signing

These questions should be settled in the markup, not after closing.

- Which Treasury series is referenced, and from which publication source?

- Is the relevant date the quote date, notice date, or payoff date?

- Does the formula assume monthly or semiannual discounting?

- Are unpaid default-rate amounts or protective advances included in the premium base?

- Is there a minimum premium regardless of market conditions?

Lockouts, defeasance triggers, and partial prepayment limits

Some loan structures restrict negotiation not through the formula itself but through the surrounding prepayment regime. A lockout may prohibit any voluntary prepayment for a fixed period, while CMBS documents may shift the exit path from yield maintenance to defeasance during the securitized phase.

According to sample securitized mortgage loan pooling and servicing language filed with the U.S. Securities and Exchange Commission, servicing standards and REMIC-related constraints can narrow prepayment flexibility and shape defeasance procedures in securitized deals. In other words, there is no point negotiating the premium clause if the broader structure overrides it later.

Borrowers should also test whether partial prepayments are allowed, whether casualty or condemnation proceeds trigger mandatory applications, and whether those applications reduce future yield maintenance exposure. A useful comparison point is yield maintenance vs step-down, since step-down structures usually give borrowers a clearer view of declining exit cost.

A practical markup checklist for sponsors, brokers, and counsel

The best borrower review is a line-by-line checklist tied to actual transaction scenarios: refinance in year three, sale in year five, partner buyout, and a failed near-maturity extension. Those scenarios quickly show which provisions are cosmetic and which ones change proceeds.

- Identify the exact documents that control prepayment, assumption, lockout, and transfer rights.

- Strike or narrow any spread floor that distorts the reinvestment spread below market logic.

- Add an open period with a defined duration and a nominal fee instead of formula-based yield maintenance.

- Revise assumption provisions to use objective approval standards and stated review deadlines.

- Define the Treasury benchmark, observation date, and discounting convention precisely.

- Check whether lockout language, securitization provisions, or defeasance triggers override the negotiated clause.

- Require a payoff statement that itemizes principal, accrued interest, premium, fees, and source inputs.

- Model at least two exit scenarios before closing using current rates and a lower-rate case.

This is often where sponsors discover that a supposedly minor drafting issue changes the sale outcome in a very real way. For a narrower discussion of how payoff economics appear in practice, see yield maintenance prepayment penalty.

Frequently Asked Questions

What is the most important point in a yield maintenance borrower negotiation?

The highest-value issue is usually the combination of spread language and benchmark definition. A spread floor, minimum premium, or borrower-unfriendly Treasury definition can increase prepayment cost substantially, especially if rates fall after closing.

How long should an open period be in a CRE loan?

Many borrowers ask for 90 to 180 days before maturity, but market terms vary by lender, asset type, leverage, and securitization expectations. The real drafting issue is not the label. It is whether the clause clearly removes the premium during that period and states any required notice.

Can assumption rights eliminate a yield maintenance charge on a sale?

They can, if the loan permits assumption and the buyer meets the lender's approval standards. In practice, the value of the assumption right depends on whether the documents use objective financial tests, fixed review timelines, and a clear release structure for the seller and guarantor.

Do CMBS loans give borrowers the same negotiation room on yield maintenance terms?

Usually less. CMBS structures often include servicing standards, transfer restrictions, and defeasance mechanics that leave less document flexibility than balance-sheet executions. Borrowers should review both the premium clause and the broader securitization language before closing.

Does yield maintenance negotiation vary by market or region?

Yes, but usually because lenders behave differently, not because state-by-state statutes control the issue. Life companies, debt funds, banks, and CMBS lenders may offer different assumption rights, open periods, and benchmark definitions in the same market. Counsel should check the actual loan form and servicing framework for the transaction jurisdiction and lender type rather than assume local custom controls.