Yield Maintenance Multifamily Loans: Lender Differences

Multifamily yield maintenance varies widely by lender. Agency loans, banks, and balance-sheet lenders often set different lockout periods, Treasury spreads, open windows, and defeasance options, and those differences can materially change the cost of a sale or refinance before maturity.

There is no single market standard for prepayment on multifamily yield maintenance loans. In apartment financing, Fannie Mae and Freddie Mac loans, bank loans, and balance-sheet lender loans all handle prepayment differently, using their own mix of lockouts, yield maintenance periods, step-down schedules, defeasance rights, and open-prepay windows.

This article breaks down how multifamily yield maintenance loans are usually structured, where lender types tend to diverge, and what apartment owners should compare before they close. The practical issue is simple: two loans with the same note rate can produce very different payoff costs because the documents use different formulas, benchmarks, and timing rules.

Yield maintenance multifamily loans: direct answer

Yield maintenance multifamily loans require the borrower to make the lender whole for lost interest if the loan is paid off before maturity. The calculation usually ties to a Treasury-based reinvestment rate and the remaining scheduled payments. In practice, agency lenders often work from standardized servicing frameworks, while banks and balance-sheet lenders show more variation in lockouts, minimum penalties, and open periods.

For a broader overview of commercial real estate yield maintenance, see the cluster pillar. If you need the math itself, Graphline's separate guide to the yield maintenance formula walks through the calculation in more detail.

Key Takeaways

- Agency multifamily loans often pair longer fixed-rate terms with tightly defined prepayment rules administered through standardized servicing processes.

- Bank multifamily loans may use yield maintenance, step-down, or hybrid structures, and the real outcome depends on the note and rider language, not the lender label alone.

- Balance-sheet lenders often give borrowers more room to negotiate open periods, floors, or alternative prepayment schedules, but that flexibility usually costs something in pricing or leverage.

- The same apartment refinance or sale can lead to very different exit costs depending on the Treasury benchmark, spread, minimum penalty, and whether assumption is allowed.

- Owners should review the note, loan agreement, and rider before closing, not at payoff, because that is where the prepayment language is set.

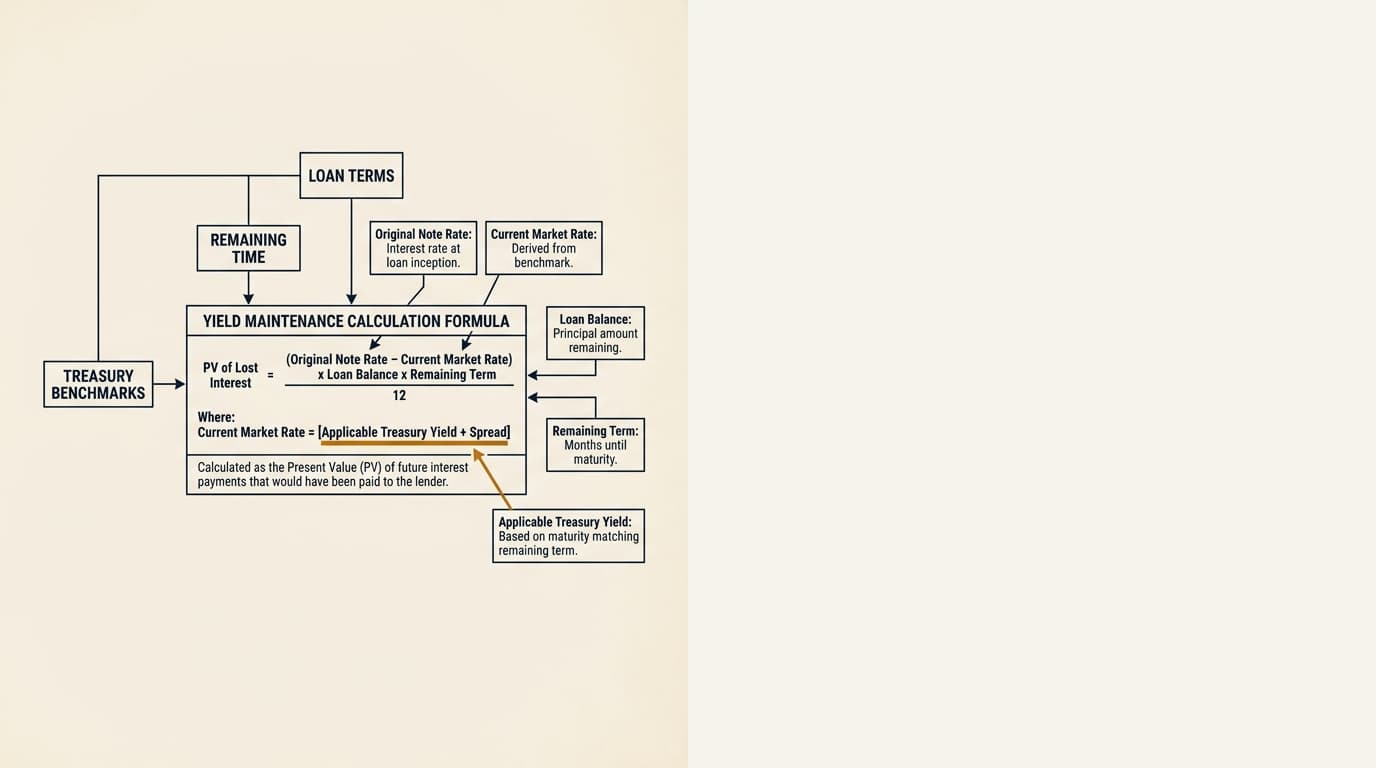

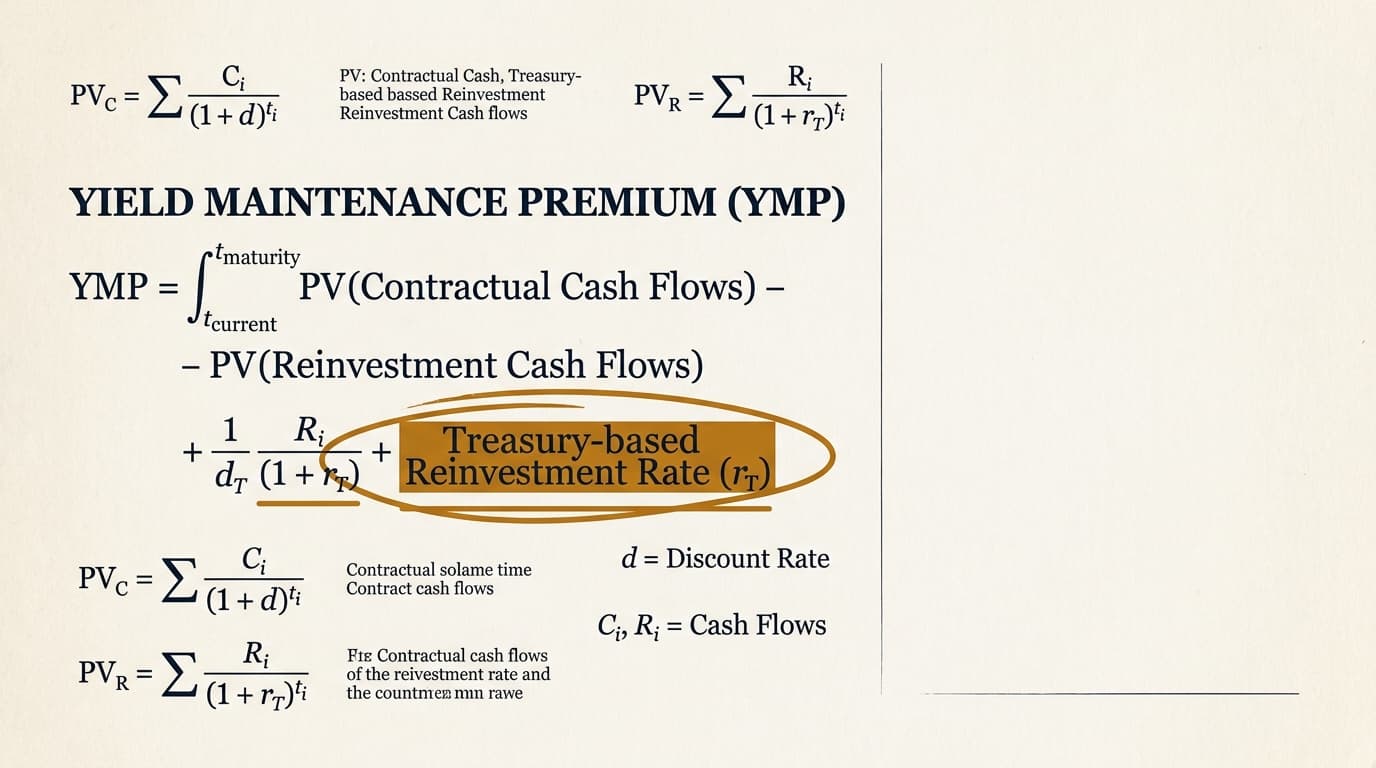

How yield maintenance works in multifamily financing

In multifamily lending, yield maintenance protects the lender's expected yield if a fixed-rate loan pays off early. According to the Fannie Mae Multifamily Selling and Servicing Guide section on yield maintenance, the prepayment premium on many Fannie Mae multifamily mortgage loans is tied to the spread between the note rate and the applicable Treasury security, subject to the governing loan documents.

The Freddie Mac Optigo Seller/Servicer Guide glossary and prepayment provisions show that Freddie Mac multifamily loans may also use yield maintenance or defeasance, depending on the product and loan terms. That distinction matters. Owners sometimes treat "agency" as one bucket, but the servicing standards and payoff options can differ quite a bit by program.

At a high level, most multifamily yield maintenance structures turn on four variables:

- Remaining scheduled term to maturity

- Contract interest rate on the note

- Current Treasury or comparable reinvestment benchmark defined in the documents

- Any floor, spread, minimum premium, or open-prepayment window

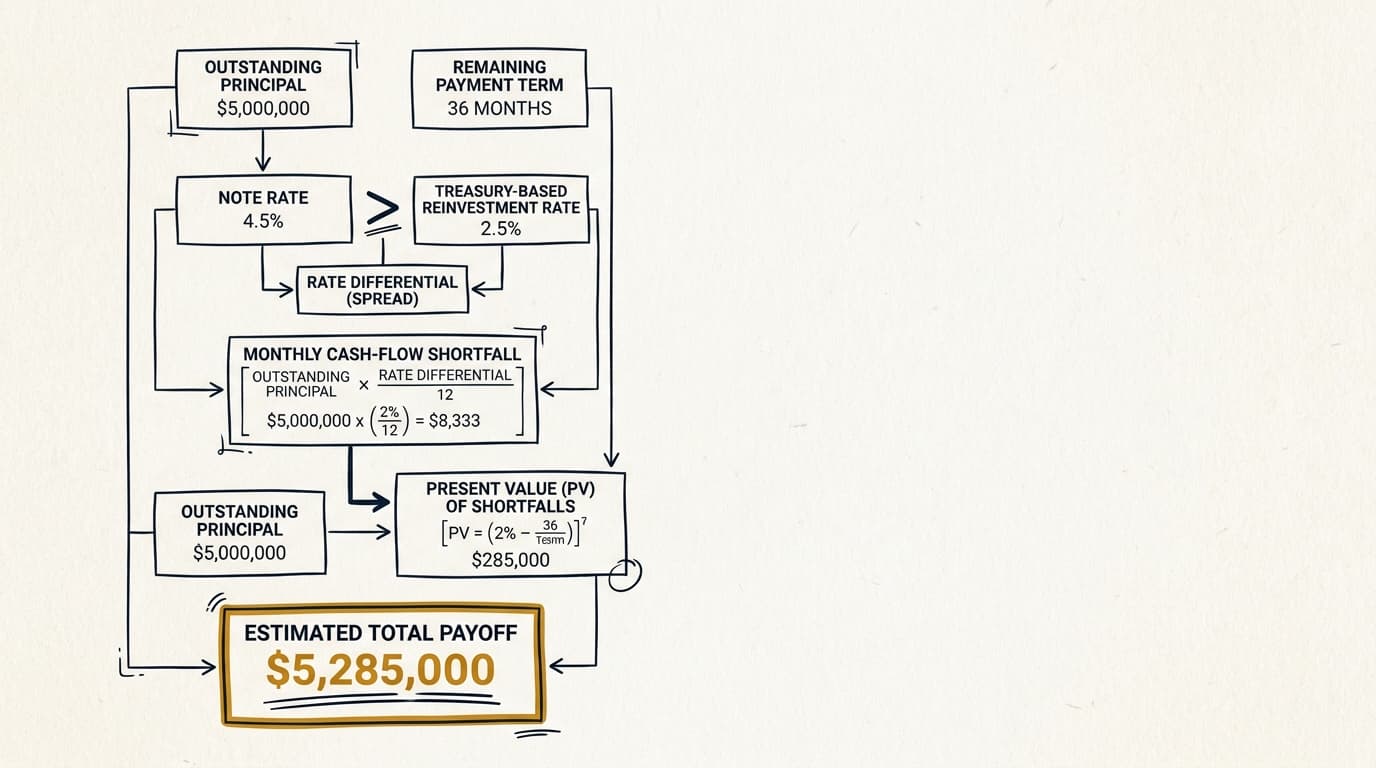

The effect is straightforward. If Treasury yields are well below the note rate, the premium usually gets larger because the lender's reinvestment rate is lower. If maturity is close, the premium usually drops because fewer scheduled payments remain. For a worked example, see this yield maintenance calculation example.

Agency multifamily loans: Fannie Mae and Freddie Mac structures

Agency multifamily loans usually have the most standardized prepayment structure in the apartment market. According to the Fannie Mae Multifamily conventional financing overview and the Fannie Mae Multifamily Selling and Servicing Guide, fixed-rate loans are often set up with either yield maintenance or declining prepayment premiums, depending on the product and term.

Freddie Mac Optigo conventional loan product materials show a similar pattern. Freddie Mac conventional multifamily loans can use yield maintenance or defeasance, with the controlling terms set by the commitment and final loan documents. In both agency channels, servicing is usually more formalized than it is in many bank portfolios.

What agency borrowers should expect

Agency borrowers should expect less discretion after closing. Once the loan is securitized or moved into the agency servicing framework, payoff timing, notice requirements, and quote procedures are generally controlled by standardized servicing rules, not relationship-based negotiation.

That usually matters in three places:

- Open windows near maturity: some agency loans allow prepayment without a premium during a defined period before maturity, but the exact window varies by product and documents.

- Assumption rights: assumption may be available, subject to agency approval and underwriting. In an apartment sale, that can be an alternative to paying the premium. See yield maintenance assumption sale.

- Defeasance alternatives: some Freddie Mac executions and securitized structures may push borrowers toward defeasance instead of cash prepayment. See yield maintenance vs defeasance and cmbs yield maintenance for that comparison.

The main point: agency loans can look predictable on paper, but owners still need the exact note language. A small change in the Treasury selection rule or spread can change the payoff statement by a meaningful amount.

Bank multifamily loans: more variation in prepayment language

Bank multifamily loans show the widest range of yield maintenance drafting among mainstream apartment lenders. Unlike agency executions, which rely on published servicing guides and more standardized templates, bank loans are often portfolio documents with lender-specific riders, custom floors, and negotiated open-prepay periods.

The Office of the Comptroller of the Currency Commercial Real Estate Lending handbook makes the broader point that banks structure CRE loans around portfolio strategy, interest-rate risk, and asset-liability management. On the ground, that means one regional bank may insist on full yield maintenance through most of the term, while another may use a yield maintenance vs step-down structure or a simple declining percentage schedule.

Common bank structure differences

Bank multifamily documents often differ in the details that end up controlling the payoff quote. The biggest differences usually show up in the note and prepayment rider, not in the term sheet summary.

- Benchmark selection: some banks define the comparison rate using a Treasury matched to the remaining average life. Others use a Treasury closest to maturity.

- Spread or floor: the formula may add a spread to the Treasury, or apply a minimum return floor that keeps the premium from falling below a stated amount.

- Lockout periods: a bank may bar prepayment entirely for 12 to 24 months before yield maintenance even begins.

- Minimum premium: some documents require at least 1% of the outstanding principal even if the formula produces a lower number.

- Open periods: a common negotiation point is whether the loan becomes open in the last 90 days, 180 days, or 12 months.

That is why apartment owners should review yield maintenance loan documents line by line. The label "yield maintenance" alone tells you very little about the actual economics.

Balance-sheet and debt-fund multifamily loans: negotiated structures

Balance-sheet lenders and debt funds often have more room to negotiate prepayment economics than agencies, but borrowers pay for that flexibility one way or another. In multifamily loans, you might get a shorter lockout, a lighter step-down, or partial open prepayment in exchange for a higher spread, lower leverage, tighter reserves, or stricter extension conditions.

According to the Federal Reserve discussion of commercial real estate lending and banking-sector exposures, lender behavior in CRE shifts with funding costs and balance-sheet pressure. As of 2026, that means many non-agency lenders facing higher capital and funding costs are less inclined to relax prepayment protection on stabilized multifamily assets unless they get compensated elsewhere in the structure.

Where balance-sheet lenders can be more flexible

Balance-sheet lenders can sometimes offer better prepayment flexibility for apartment owners with short hold periods or redevelopment plans. The negotiation points are fairly specific, and they all live in the documents.

- Shorter hard lockout: for example, no prepay in year one, then a declining premium.

- Hybrid schedules: yield maintenance for an initial period, followed by 3%, 2%, 1%, then open.

- Partial release or partial prepayment rights: more common in portfolio contexts than in agency executions.

- Refinance carve-outs: occasional lender discretion if the same institution is replacing the debt.

These structures can make sense for multifamily owners planning to refinance after lease-up, renovation, or rate stabilization. They are less common in heavily commoditized fixed-rate executions where the lender wants bond-like cash flow.

Multifamily prepayment comparison table by lender type

The best way to compare yield maintenance multifamily loans is to isolate the variables that affect a real payoff. The table below summarizes common patterns, not fixed rules. In every case, the signed documents control.

| Lender type | Typical prepayment approach | Where variation shows up | Borrower implication |

|---|---|---|---|

| Agency fixed-rate | Yield maintenance or product-specific declining premium; some executions may allow defeasance | Program type, servicing rules, open window, assumption rights | Predictable administration, limited post-closing flexibility |

| Bank portfolio | Yield maintenance, step-down, or hybrid | Treasury benchmark, floors, minimum premium, lockout length | Most document-level variation among traditional lenders |

| Life company / balance-sheet | Yield maintenance or negotiated hybrid schedule | Open periods, negotiated prepay rights, spread trade-offs | Can offer flexibility if addressed before closing |

| Debt fund | Often step-down or negotiated exit fee rather than classic yield maintenance | Extension options, minimum interest, exit fees, recap rights | May fit short business plans but usually at higher coupon |

A simple way to think about it: if the apartment business plan assumes a sale or refinance within three to five years, prepayment flexibility belongs in the total cost analysis. It is not a legal footnote. A lower note rate can easily be offset by a larger exit premium if rates fall or the project performs ahead of schedule.

How apartment owners should compare prepayment flexibility before closing

Apartment owners should compare multifamily prepayment flexibility before closing by turning each lender's clause into an actual exit scenario: refinance in year three, sale in year five, and payoff during the final open period. That tells you far more than note rate alone.

- Request the draft note, rider, and commitment language covering prepayment, assumption, and open periods.

- Identify whether the structure is hard lockout, yield maintenance, step-down, defeasance, or a hybrid.

- Confirm the benchmark index, spread, floor, and any minimum premium stated in the documents.

- Model at least three exit dates against the business plan: early sale, expected refinance, and near-maturity payoff.

- Check whether assumption is allowed and whether it is realistic for the likely buyer pool.

- Ask the lender how payoff quotes are issued, how much notice is required, and which servicer controls the process.

This is where the specialized articles can save time. If the issue is timing, see yield maintenance before maturity. If the issue is a refinance or sale decision, see yield maintenance refinance or sale. If the issue is revising the clause before closing, see yield maintenance borrower negotiation.

Edge cases that change the payoff result

Some multifamily edge cases change the payoff result even when the headline prepayment structure looks straightforward. These issues are often missing from lender summaries and only show up in the legal documents or servicer instructions.

Supplemental and restructured agency debt

Supplemental loans, modifications, and restructured agency debt can create layered prepayment outcomes. According to the Fannie Mae Multifamily Selling and Servicing Guide, supplemental and modified obligations have their own approval and servicing requirements, and those can affect payoff logistics and timing.

Assumption can outperform cash payoff

On an apartment sale, assumption can preserve value better than paying a premium in cash, especially when the in-place note rate looks attractive against current market debt. It is not automatic. The buyer still has to qualify, and the lender or agency still has to approve the transfer. But in the right deal, it can materially improve proceeds.

Falling rates can expand the penalty

If Treasury rates fall after origination, a yield maintenance payoff can rise at exactly the moment refinancing becomes more attractive. For more on that benchmark effect, see yield maintenance treasury rate and the deeper discussion in yield maintenance prepayment penalty.

The core point is easy to miss: multifamily yield maintenance is not just a formula problem. It is also a document, servicing, and timing problem. Owners comparing apartment lenders should underwrite the exit as carefully as they underwrite the closing.

Frequently Asked Questions

Do multifamily agency loans always use yield maintenance?

No. According to the Fannie Mae Multifamily Selling and Servicing Guide and Freddie Mac Optigo Seller/Servicer Guide, multifamily agency loans may use different prepayment structures depending on the product, term, and securitization context. Some fixed-rate loans use yield maintenance, while others use declining premiums or defeasance-based structures.

Are bank multifamily loans more flexible than agency loans on prepayment?

Often, yes, but not always. Bank portfolio lenders usually have more freedom to negotiate lockouts, open periods, and hybrid schedules before closing. After closing, flexibility depends on the signed documents. A bank loan with a long hard lockout and a minimum premium may be less flexible than an agency loan with an assumption option or a defined open window.

What documents control yield maintenance on an apartment loan?

The controlling language is usually in the promissory note, loan agreement, prepayment rider, and any modification or assumption documents. Term sheets and marketing summaries are not enough. That is why owners and counsel should review the actual yield maintenance loan documents before execution.

Can a buyer assume a multifamily loan to avoid a yield maintenance premium?

Sometimes. Agency and some balance-sheet multifamily loans may allow assumption, subject to lender approval, underwriting, fees, and document conditions. Whether assumption is the better economic choice depends on the note rate, buyer qualifications, and transaction timing. For a deeper discussion, see yield maintenance assumption sale.

Does multifamily yield maintenance vary by market or region?

The legal structure usually depends more on the lender program and the loan documents than on geography, but local market conditions still matter. In liquid apartment markets such as Dallas, Atlanta, or Phoenix, owners may place more value on assumption rights or shorter open periods because sale and refinance opportunities can appear quickly. In less liquid markets, borrowers may care more about rate and leverage than exit flexibility. State law can also affect enforcement and workout dynamics, so counsel should review jurisdiction-specific issues in the loan documents.