CMBS Yield Maintenance vs Defeasance: Cost Guide

For CMBS loans, the cheaper way out usually depends less on what the clause is called than on Treasury yields, time left on the loan, and transaction costs. This comparison shows when yield maintenance leads to a lower total payoff, when defeasance costs less, and which loan terms usually tip the outcome.

On a CMBS loan, the gap between yield maintenance and defeasance can be small or it can blow past several hundred thousand dollars. The result usually turns on Treasury rates, the note spread, and how long the loan stays closed to prepayment. For a borrower weighing a sale or refinance in 2026, CMBS yield maintenance vs defeasance is not a generic prepayment question. It is a loan-document and cash-flow question tied to the note, the servicing structure, and the market for defeasance collateral.

This article breaks down how each option works in the real world, where the total cost usually comes from, and which rate and timing setups tend to favor one over the other. It also points to the loan provisions that often decide the issue before anyone orders a quote.

Key Takeaways

- In CMBS, defeasance usually includes the cost of substitute securities plus legal, servicer, accountant, and successor borrower fees. Yield maintenance is usually a formula-based prepayment charge tied to Treasury rates and the remaining loan term.

- When Treasury yields fall, yield maintenance usually gets more expensive because the lender or trust is being compensated for reinvesting at a lower rate, as standard prepayment formulas in loan documents generally provide.

- Defeasance can be cheaper when the yield-maintenance formula is harsh, the loan still has a long term left, or the Treasury portfolio needed for substitution is relatively efficient to build.

- Open-prepayment windows, lockout expiration, and the exact defeasance language in the note and servicing package usually matter more than general market rules.

- Borrowers should compare draft payoff and defeasance quotes side by side, including third-party fees and timing assumptions, before locking in a sale or refinance timeline.

CMBS yield maintenance vs defeasance: the short answer

In CMBS, yield maintenance is usually cheaper when rates are high relative to the note rate, the remaining term is shorter, and transaction fees make defeasance inefficient. Defeasance gets more competitive when rates have fallen, the loan has a longer remaining term, or the loan documents limit prepayment to defeasance instead of a cash payoff.

The reason is simple: the two structures price different things. According to Cornell Law School Legal Information Institute's explanation of defeasance, defeasance substitutes collateral instead of paying off the debt in the usual way. According to Investopedia's yield maintenance overview, yield maintenance is meant to preserve the lender's expected yield after an early payoff. In CMBS, both concepts sit inside a servicing and trust structure that makes the math and the process more rigid than what you see in many balance-sheet loans.

For broader background on commercial real estate yield maintenance and the non-CMBS comparison between yield maintenance vs defeasance, those pages cover the broader picture. This page stays on securitized loans.

How CMBS yield maintenance works in securitized loans

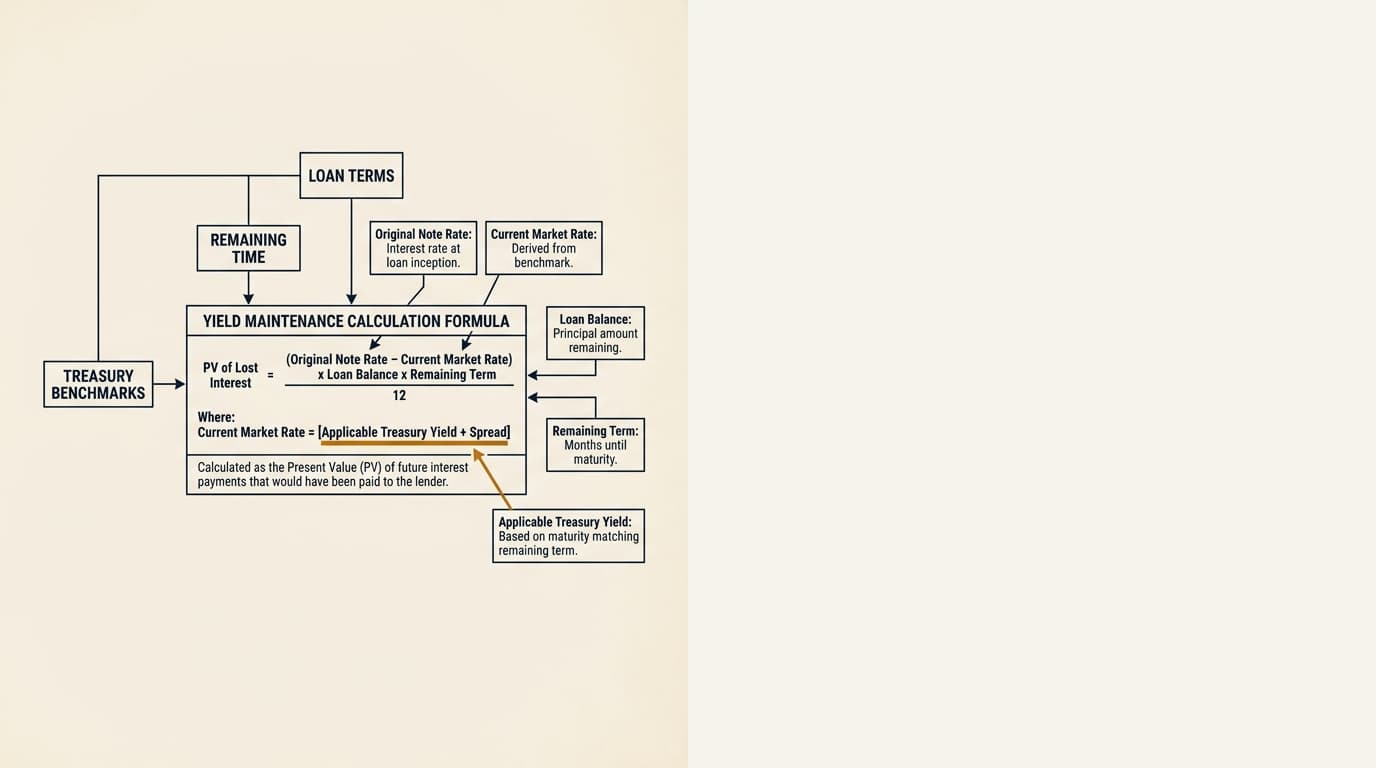

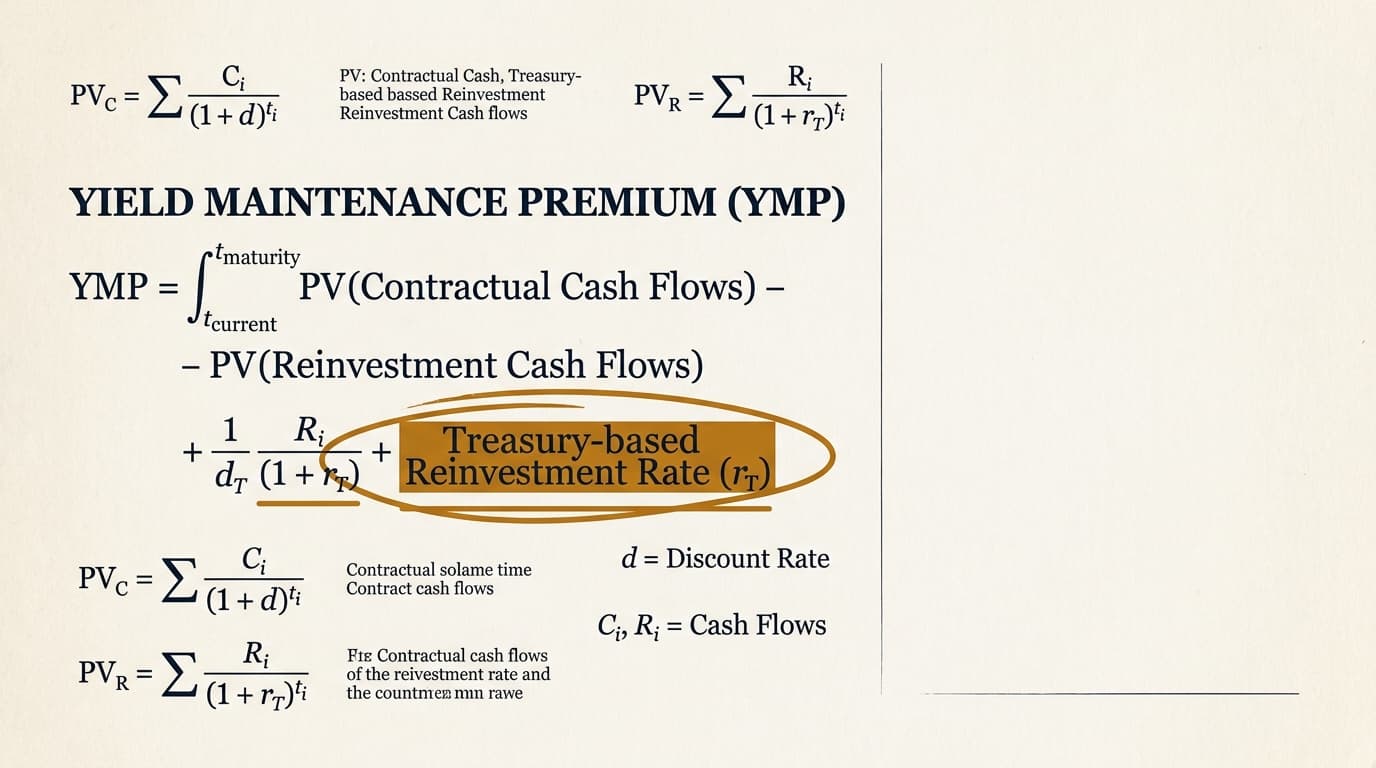

CMBS yield maintenance is a contractual prepayment premium meant to leave the trust in roughly the same economic position it expected if the loan had stayed in place. The formula usually discounts the difference between the note rate and a specified Treasury-based reinvestment rate over the remaining scheduled term, and some documents impose a minimum premium floor.

The details come from the loan documents, not from some universal industry standard. According to CMBS Loans' explanation of CMBS prepayment structures, securitized loans commonly use lockouts, defeasance, or yield maintenance depending on the note terms. According to Freddie Mac's comparison of defeasance and yield maintenance, yield maintenance generally gets larger as replacement rates fall because the investor has worse reinvestment options.

In practice, borrowers looking at a payoff should isolate four inputs:

- Outstanding principal balance.

- Remaining scheduled term to the open-prepay date or maturity.

- Contract note rate and contractual spread to the Treasury benchmark.

- Any formula floor, minimum penalty, or special servicing condition in the note.

If the note uses a Treasury-based spread formula, even a small move in the benchmark can materially change the payoff. For a more technical breakdown, see the supporting pages on yield maintenance formula, yield maintenance treasury rate, and an applied yield maintenance calculation example.

How CMBS defeasance works and why transaction costs matter

CMBS defeasance replaces the real estate collateral with a portfolio of government securities sufficient to make the remaining scheduled loan payments. From the borrower's perspective, the goal is release of the property lien. From the trust's perspective, the goal is keeping bond cash flow exactly on schedule.

According to sample CMBS defeasance provisions filed with the U.S. Securities and Exchange Commission, the process usually requires substitute collateral, legal opinions, rating-agency-related deliverables in some structures, and servicer approval steps. According to Bloomberg Professional's explanation of defeasance mechanics, the borrower or its advisor generally buys securities that replicate the loan payment stream.

So the all-in cost of defeasance is not just the bond portfolio. It usually includes:

- Purchase price of substitute securities.

- Servicer and special servicer review fees, if applicable.

- Trust counsel, borrower counsel, and defeasance consultant fees.

- Successor borrower formation and administration costs.

- Accountant verification or cash-flow matching fees.

This is the first big difference from yield maintenance. Yield maintenance is usually driven by the formula result. Defeasance can look cheaper on pure spread economics and still end up costing more once the professional fees and securities execution costs are added in.

CMBS yield maintenance vs defeasance cost comparison by rate scenario

Rate direction usually drives the comparison, but it does not settle it by itself. The cheaper structure is the one with the lower total cost under the actual note terms and the actual closing date, whether that means a formula premium or securities cost plus transaction expenses.

| Scenario | Yield maintenance tendency | Defeasance tendency | Why |

|---|---|---|---|

| Treasury rates well below note rate | Often expensive | Often more competitive | Lower reinvestment rates raise the maintenance premium; defeasance collateral may still price better than the formula. |

| Treasury rates near note rate | Often moderate | Mixed | The formula tightens, but defeasance still carries fixed transaction costs. |

| Treasury rates above note rate | Often lower or near minimum | Often less attractive | The maintenance formula may shrink sharply, while defeasance fees do not. |

| Short time remaining to open prepay or maturity | Often lower | Often less efficient | There are fewer remaining payments to protect, but defeasance still requires a full transaction process. |

| Long remaining term | Can become large | Can improve relative to YM | More protected cash flow means larger formula exposure; defeasance economics depend on securities pricing. |

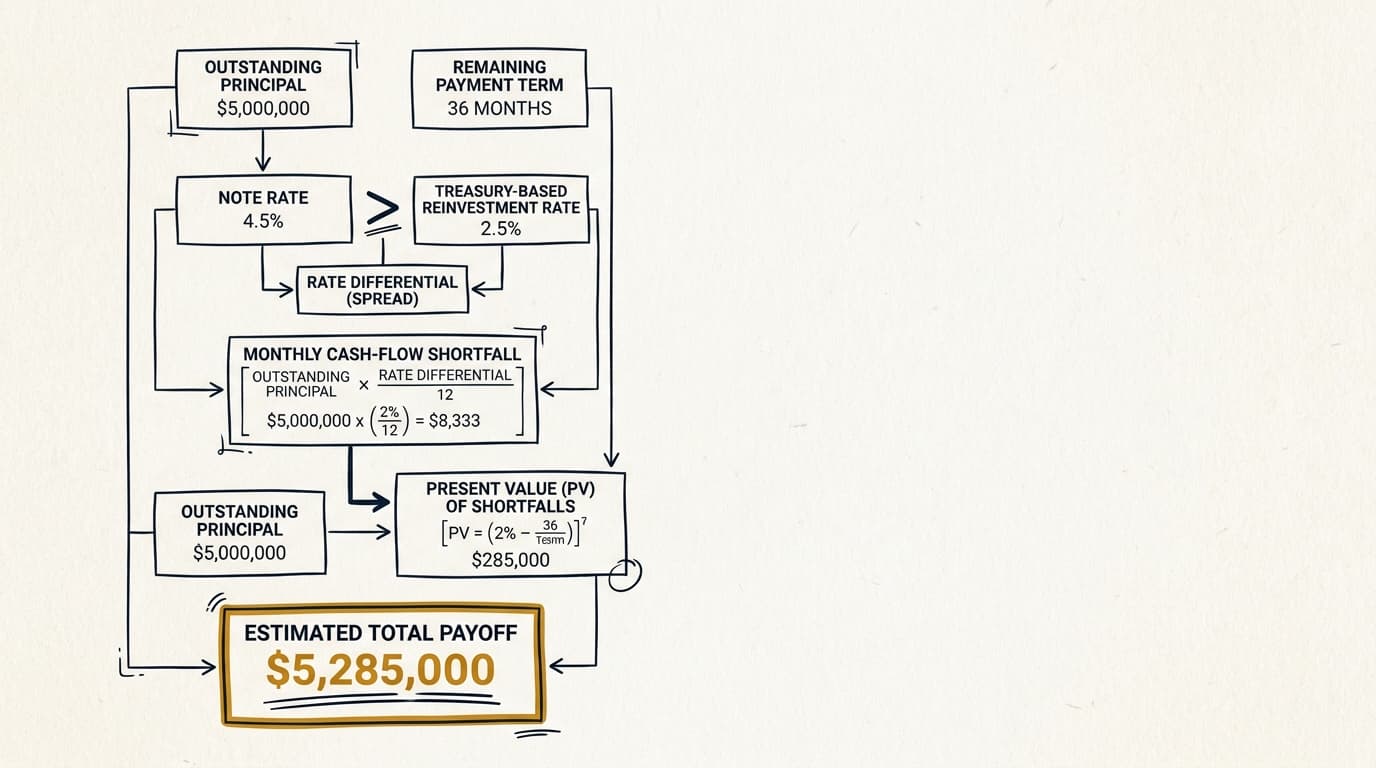

A simplified example shows the pattern. Assume a $12 million CMBS loan at 5.85% with 48 months remaining and a Treasury-based maintenance formula. If the relevant Treasury is 3.40%, the spread to reinvestment is meaningful and the yield-maintenance charge may be substantial. If that Treasury moves to 5.10%, the formula tightens fast, and a defeasance package with six-figure aggregate fees may stop being the cheaper path.

The edge case is a loan with a short remaining term but mandatory defeasance language. In that situation, a borrower may not have a practical yield-maintenance option at all. The first step is always to confirm the prepayment structure in the yield maintenance loan documents and, for securitized context, the dedicated page on cmbs yield maintenance.

When yield maintenance is likely cheaper than defeasance

Yield maintenance is usually cheaper in CMBS when the premium has already narrowed and defeasance would still require the full securities substitution process. That tends to happen in higher-rate environments, later in the loan term, or where the note gives the borrower a relatively favorable minimum premium structure.

Higher benchmark rates reduce the formula burden

Higher Treasury yields usually reduce the present value of the lender's reinvestment loss. In plain English, a large prepayment charge can shrink into a much smaller number, sometimes leaving defeasance transaction costs as the main expense.

This is why broad statements about prepayment economics are not very useful once you are dealing with a live CMBS quote. A borrower who assumed defeasance was always cheaper in 2021 could easily find the reverse under 2025 or 2026 rate conditions, depending on the note spread and remaining term.

Shorter remaining term favors cash-payoff structures

A shorter remaining term means fewer protected payments are left in the formula. If only a limited number of scheduled payments remain before an open period, the value of building a substitute securities portfolio may be pretty thin.

This timing issue also affects sale planning. A borrower considering a disposition should compare the economic impact of delaying closing by 60 to 120 days. In many cases, that matters more than arguing over relatively small consultant-fee differences. Related timing considerations are covered in yield maintenance before maturity and yield maintenance refinance or sale.

When defeasance is likely cheaper than CMBS yield maintenance

Defeasance is more likely to come out ahead when the maintenance formula is severe under current rates or when the loan documents make defeasance the cleaner path to lien release. In long-dated CMBS loans, the gap between the note rate and the Treasury benchmark can make a cash payoff expensive enough that transaction fees become secondary.

Falling-rate environments often favor defeasance

Falling rates tend to push the yield-maintenance premium higher because the trust is assumed to reinvest at lower yields. Defeasance collateral pricing moves with rates too, but not in a simple one-for-one way. In some structures, the securities package plus fees still comes in below the maintenance formula.

This is the scenario borrowers misread all the time when they focus on the label instead of the dollars. The real question is not whether defeasance sounds more complicated. The real question is which structure produces the lower verified wire amount at closing.

Document mandates can override economic preference

Many CMBS loans do not give the borrower a free choice between the two structures. Some require defeasance during most of the closed period and allow open prepayment only within a stated window before maturity.

According to Fannie Mae Multifamily guidance on defeasance, defeasance structures preserve scheduled cash flows for investors. CMBS documents often pursue the same result. So the economic comparison matters only after you confirm that the note actually allows the cheaper option.

Document terms that usually decide the answer

The answer is usually in the note, deed of trust, and servicing provisions, not in a market article. Borrowers should identify the operative prepayment clause before ordering a quote or setting a sale schedule.

Review these items first:

- Confirm whether the loan allows cash prepayment, defeasance, or both during the current period.

- Check lockout dates, open windows, and any prohibition on partial releases.

- Identify the exact Treasury benchmark and spread used in any maintenance formula.

- Check for minimum premiums, make-whole floors, or alternative prepayment language.

- Verify notice periods, servicer fee schedules, and required third-party reports.

These details are the difference between a rough estimate and a number you can actually defend. For clause-level review, the supporting pages on yield maintenance loan documents and yield maintenance borrower negotiation cover where these provisions usually appear and what borrowers tend to flag before closing a loan.

A practical decision framework for borrowers

The most reliable way to compare CMBS yield maintenance and defeasance is to build a side-by-side exit model using the expected closing date, not a rule of thumb. In real deals, the cheaper option can flip with a 25- to 50-basis-point rate move or a modest shift in timing.

A workable borrower framework looks like this:

- Obtain the note language and confirm the currently permitted prepayment method.

- Request an indicative yield-maintenance quote tied to a specific as-of date.

- Request an indicative defeasance quote that includes securities, professional fees, and servicer charges.

- Model at least three closing dates, such as immediate close, 30 days out, and 90 days out.

- Stress-test the comparison under modest Treasury moves instead of relying on one static rate snapshot.

- Compare the total wire amount, transaction complexity, and execution risk before locking the sale or refinance timeline.

This produces a better answer than comparing headline penalties. It also separates pure economic cost from execution friction. If a borrower is selling under a tight purchase agreement, paying a little more for the more certain payoff path may be worth it. If a borrower is refinancing and has flexibility, waiting for the formula to improve or for the open-prepay window to arrive may be the smarter move.

For borrowers comparing other prepayment structures, the related pages on yield maintenance vs step-down, yield maintenance prepayment penalty, and yield maintenance assumption sale cover adjacent decision points.

Frequently Asked Questions

Is defeasance always required for a CMBS loan?

No. Some CMBS loans require defeasance during the closed prepayment period, while others use yield maintenance or a lockout followed by open prepayment. The controlling source is the loan note and related servicing provisions, not a general market convention.

What costs should be included in a CMBS defeasance quote?

A complete CMBS defeasance quote should include substitute securities, servicer fees, legal fees, accountant or verification costs, consultant fees, and any successor borrower expenses. Borrowers who compare only the securities package to a yield-maintenance figure usually understate total defeasance cost.

Does a falling Treasury rate usually make yield maintenance more expensive?

Yes. In most Treasury-based maintenance formulas, lower benchmark rates increase the lender's or trust's assumed reinvestment loss, which increases the premium. The exact effect depends on the note language, spread, remaining term, and any minimum penalty provision.

Can CMBS borrowers choose between yield maintenance and defeasance?

Sometimes, but not always. Many loans prescribe the available prepayment method by date range. A borrower may have defeasance as the only option before an open window, then gain the ability to prepay in cash closer to maturity.

Do CMBS defeasance costs vary by region?

The core economics are driven more by loan terms, Treasury pricing, and transaction parties than by property location. Regional differences usually show up indirectly through local counsel costs, recording practices, and closing logistics, while the securities and servicing mechanics are generally national in scope.