AI Agents for Loan Servicing in CRE: Uses and Controls

For many private CRE lenders, post-close servicing eats up more staff time than the payoff itself. AI tools for loan servicing can handle payment reminders, borrower requests, covenant tracking, escrow notices, and delinquency workflows without losing audit trails, approval controls, or servicing records.

Post-close servicing is where private CRE lenders burn the most time on repetitive borrower contact, deadline tracking, and document exceptions. AI agents for loan servicing can take a real dent out of that work after closing by handling payment reminders, borrower request triage, covenant follow-up, escrow notices, and delinquency routing, while keeping a clean audit trail for every step.

That matters in 2026 because private lenders are expected to service larger books with smaller teams, and the work itself keeps getting heavier. Borrower reporting, reserve administration, and exception handling now involve more documents, more follow-up, and more room for error. This article lays out where servicing agents help, where they break, which controls you cannot skip, and how to use them without turning servicing into a black box no one can explain later.

Key Takeaways

- AI agents for loan servicing work best on repeatable post-close tasks like payment reminders, borrower request triage, covenant follow-up, escrow notices, and delinquency routing.

- The best setups pair automation with hard controls: system-of-record data access, approval thresholds, immutable logs, and exception queues.

- According to the Consumer Financial Protection Bureau mortgage servicing requirements under Regulation Z and the Real Estate Settlement Procedures Act servicing rules in Regulation X, servicing communications and borrower responses can trigger compliance obligations in some contexts. Even private lenders outside agency-style platforms need strong auditability.

- According to the Federal Deposit Insurance Corporation consumer compliance examination guidance, institutions are expected to keep evidence of policies, controls, and exception handling. Private CRE servicing should follow that same discipline, even when the exact consumer rulebook does not apply.

- The lenders getting the best results use AI agents to prepare work, draft communications, and gather evidence, not to make unsupervised servicing decisions that change loan terms.

AI agents for loan servicing: what they do after closing

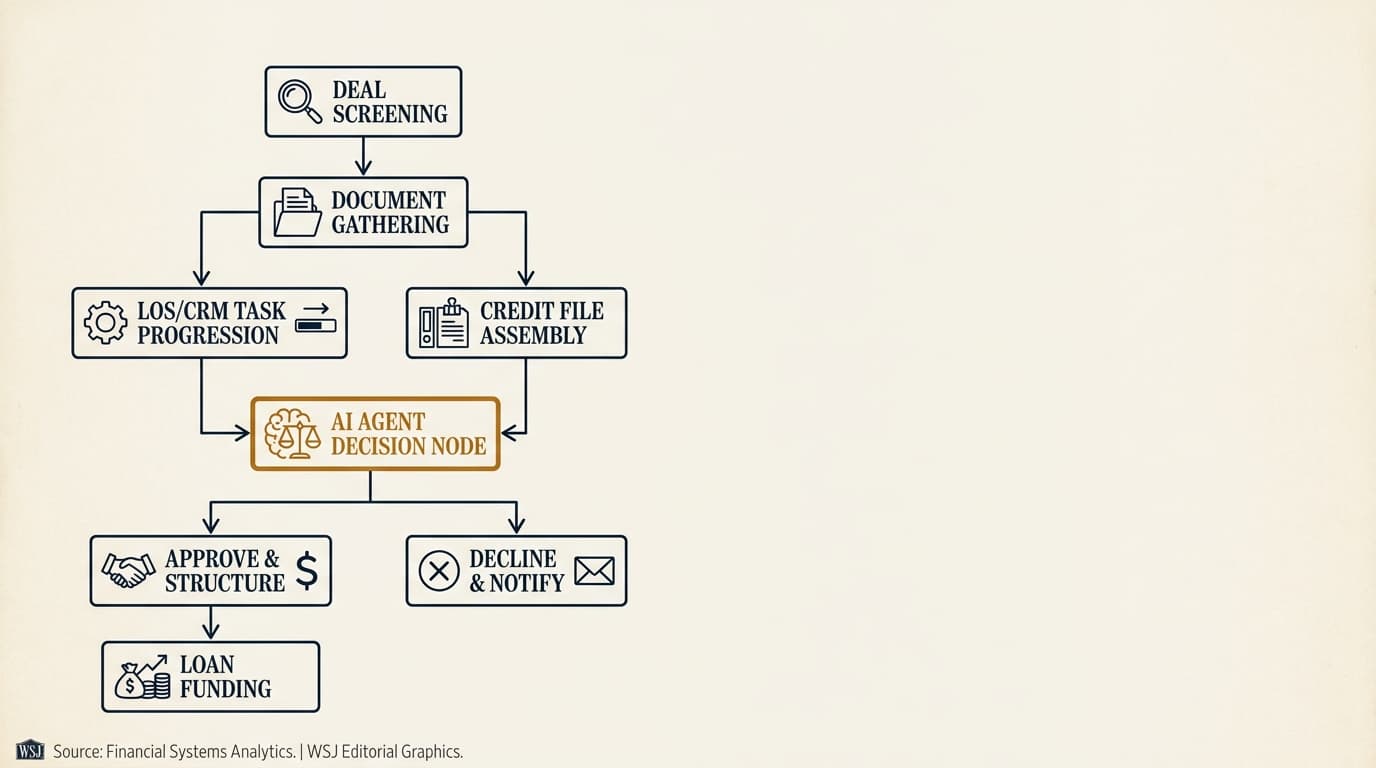

AI agents for loan servicing are software tools that monitor servicing events, pull the right data and documents, and start or draft next-step actions based on lender-defined rules. In private commercial real estate lending, the best use cases start after closing, when the work shifts from underwriting to day-to-day administration, borrower communication, and exception handling.

A servicing agent usually sits between the lender's system of record, document repository, inboxes, and tasking tools. It does not replace the servicing platform. It watches for triggers like upcoming due dates, missing financials, insurance expirations, reserve thresholds, borrower email requests, and late-payment conditions. Then it creates tasks, drafts notices, pulls supporting files, and routes exceptions to the right servicing employee.

This is different from ai agents for private commercial real estate lending, which covers the broader lending workflow from intake through portfolio operations. It is also separate from ai agents for cre loan origination and ai agents for cre underwriting, where the focus is on pre-close decisions rather than post-close servicing administration.

Where AI agents fit in the post-close servicing stack

The most useful place for AI agents in loan servicing is the orchestration layer around repetitive service events. They do best where the rule is stable, the source data is clear, and a human reviewer can step in on exceptions.

In a typical private CRE shop, that stack includes five layers:

- System-of-record data — loan terms, payment schedules, balances, reserve accounts, contact records, and collateral identifiers.

- Document layer — notes, modifications, guaranties, insurance certificates, tax bills, financial reporting packages, servicing correspondence, and payoff support.

- Trigger layer — due dates, delinquency thresholds, covenant deadlines, maturity windows, insurance expirations, reserve deficits, and inbound borrower requests.

- Action layer — reminders, notices, task creation, draft responses, escalation routing, and handoff packets.

- Control layer — approvals, permissions, locked templates, evidence capture, and audit logs.

According to the National Institute of Standards and Technology AI Risk Management Framework, organizations using AI in operational workflows should govern data quality, human oversight, and traceability. In servicing, that comes down to a simple rule: an agent can prepare and route work, but the lender still needs a clear record of what source data it used, which rule fired, what communication went out, and who approved any non-routine action.

Payment reminders and payment exception workflows

Payment reminders are usually the cleanest starting point for AI agents for loan servicing: lower risk, high volume, easy to measure. The agent can read the payment calendar, identify upcoming due dates, generate borrower-specific reminders, and flag exceptions like unapplied funds, partial payments, or wires received without identifiers.

For private CRE lenders, the real operational gain is not the reminder itself. It is the drop in cleanup work after the reminder goes out. A servicing agent can:

- Pull the scheduled payment amount and due date from the servicing system.

- Insert approved remittance instructions and borrower contacts.

- Suppress reminders where a payment is already posted, in process, or under dispute.

- Create same-day exception tasks for partial receipts, short pays, and unidentified wires.

- Log the communication, template version, source records used, and delivery timestamp.

According to the Consumer Financial Protection Bureau mortgage servicing compliance resources, institutions are expected to maintain accurate servicing information and respond appropriately to payment issues and borrower inquiries. Even when a private CRE loan falls outside standard consumer servicing patterns, the lesson still holds: reminder automation should be tied to posted ledger data, not a spreadsheet someone copied two days ago.

A common failure point shows up when the agent relies on stale balances or ignores lockbox timing. The borrower gets a late reminder after already sending funds, disputes the notice, and servicing staff has to unwind the mess by hand. The fix is simple: require the agent to check ledger status, unapplied cash, and same-day payment queues before sending any past-due or late-stage communication.

For a deeper breakdown of reminder logic and payment handling, lenders should see ai for loan servicing payment management.

Payment exception queues are more valuable than generic reminders

Most lenders overrate outbound reminders and underrate exception routing. The biggest time savings usually come from sorting the 10 to 20 percent of payment events that do not reconcile cleanly.

In practice, the agent should classify exceptions into operational buckets like these:

| Exception type | Typical cause | Best next action |

|---|---|---|

| Partial payment | Short wire, reserve confusion, borrower dispute | Create servicing review task and hold borrower notice until reviewed |

| Unidentified funds | Wire lacks loan number or property reference | Match remitter and route to cash application queue |

| Payment posted after reminder cycle | Batch delay or lockbox timing | Suppress follow-up and log timing exception |

| Repeated late payment | Cash flow pressure or borrower process weakness | Escalate to delinquency monitoring after threshold is met |

That classification layer creates real operational value because it cuts down inbox review and the ad hoc detective work servicing staff usually gets stuck with.

Borrower requests: statements, balances, consents, and payoff intake

Borrower requests eat up more servicing time than they should because they arrive in messy formats and often require pulling data from more than one place. AI agents can triage these requests, identify the request type, gather supporting records, and prepare a draft response or task package for review.

The most common requests in private CRE servicing include balance confirmations, payment histories, reserve balances, insurance questions, consent requests, assumption or transfer inquiries, and payoff-related intake. For routine informational requests, the agent can classify the email, confirm the borrower entity and loan, check whether the request needs approval, and draft a response using locked language.

This is especially useful for payoff intake. A borrower might email asking for an estimated payoff, an assumed closing date, or wiring instructions. An agent can collect the requested date, verify the loan number, flag whether default interest or fees may apply, pull the current note terms, and route the package into the authorized payoff workflow. For lenders focused on payoff execution, that front-end triage cuts cycle time before statement preparation even starts.

According to the Board of Governors of the Federal Reserve System guidance on managing outsourced risk and the Office of the Comptroller of the Currency model risk management handbook, institutions should understand how automated tools produce outputs and how those outputs are reviewed. For borrower requests, that means the agent should never send a consent approval, release, or payoff figure without rule checks and human signoff.

Where borrower request automation breaks

Borrower request automation usually breaks at the line between administrative information and legal or credit decisions. A balance confirmation is routine. A request to defer a payment, waive a covenant, approve a transfer, or interpret prepayment language is not.

Private lenders should split requests into three categories:

- Informational — balance histories, due dates, reporting deadlines, contact updates. These can often be drafted automatically.

- Operational — reserve draw status, insurance certificate follow-up, document re-delivery, payoff intake. These can be prepared automatically and reviewed by staff.

- Decision-based — waiver requests, transfers, assumptions, modifications, default remedies. These should be escalated immediately with no autonomous response.

That distinction is more useful than a generic "automation allowed" rule because it matches how servicing risk actually shows up in a private loan book.

Covenant tracking and reporting follow-up

Covenant tracking in servicing is mostly a deadline, document, and exception-management problem. AI agents can monitor reporting schedules, identify missing submissions, compare incoming documents against expected requirements, and escalate possible breaches to asset management or servicing reviewers.

Examples include quarterly rent rolls, trailing 12-month operating statements, borrower-prepared financial statements, debt service coverage reporting, occupancy tests, leasing status updates, and construction or stabilization milestones. The agent's job is not to decide whether a borrower is in breach. Its job is to make sure the reporting package is requested, received, checked for completeness, and routed with evidence attached.

According to the Federal Reserve supervisory guidance on model risk management, automated systems should be validated and monitored when outputs affect material decisions. In covenant monitoring, validation means testing whether the agent correctly identifies due dates, required document sets, and missing fields before anyone relies on its escalations.

For deeper coverage on this adjacent topic, lenders should refer to ai agents for loan covenant monitoring and ai agents for portfolio monitoring.

Why covenant servicing needs document-level evidence

The servicing team should be able to show exactly why a covenant follow-up was sent and what was missing at that moment. An audit trail that says only "financials overdue" is thin. One that shows the expected reporting period, source covenant language, due date, receipt log, and exceptions found is much easier to defend.

A well-configured agent should capture:

- The covenant clause or servicing rule that triggered the reminder.

- The due date and grace period, if any.

- The list of required files or fields.

- The timestamp and channel of each borrower follow-up.

- The reviewer who marked the package complete or escalated it.

That record becomes especially useful when a borrower disputes whether a reporting item was actually missing, or when servicing missed an attachment buried in an earlier email thread.

Escrow notices, reserve draws, and annual reviews

Escrow and reserve administration is one of the messiest parts of private CRE servicing, which is exactly why it eats so much manual effort. AI agents can help, but only when reserve categories, notice templates, approval steps, and documentation rules are tightly defined.

Typical use cases include tax and insurance reserve notices, replacement reserve balance alerts, upcoming disbursement reminders, reserve draw intake, incomplete draw package notices, and annual escrow review support. According to the Consumer Financial Protection Bureau escrow account operation requirements under Regulation X, Section 1024.17, escrow administration in regulated contexts requires specific calculations and disclosures. Many private CRE loans are handled under negotiated commercial terms instead of standardized consumer escrow frameworks, but the operational lesson still applies: reserve notices need to be tied to documented calculations and timing rules, not free-form email judgment.

A practical servicing agent can review incoming draw requests for required components like invoices, lien waivers, inspection reports, borrower certifications, and reserve availability. Then it can produce a checklist-based intake summary instead of making staff rebuild the file from scratch every time.

| Escrow or reserve task | What the agent can do | What should remain human-reviewed |

|---|---|---|

| Tax and insurance notice | Calculate due-date reminder schedule and draft notice | Final review where amounts or shortages are disputed |

| Reserve draw intake | Check package completeness against checklist | Approval of disbursement and exception handling |

| Annual reserve review | Assemble balances, disbursements, shortages, and expiring policies | Interpretive decisions on funding changes |

| Policy expiration follow-up | Track renewal dates and send evidence requests | Force-placement or default-related actions |

Delinquency workflows and workout handoffs

Delinquency is where AI agents for loan servicing can create real leverage, and it is also where governance matters most. The agent can monitor aging thresholds, compile contact history, summarize payment patterns, pull relevant loan documents, and prepare next-step notices or workout handoff packets. It should not independently choose remedies or communicate legal positions outside approved templates.

For a private CRE lender, the early delinquency workflow often has more operational friction than legal complexity. Staff need to know whether the payment is late because of cash timing, a lockbox mismatch, reserve confusion, missing billing information, or an actual distress signal. A servicing agent can pull those facts together in minutes by gathering prior payment behavior, recent borrower correspondence, unpaid charges, reserve status, and upcoming property deadlines into one case view.

According to the FDIC consumer compliance examination manual for servicing operations, examiners look for accurate records, timely responses, and evidence that staff followed policy. In commercial delinquency management, the same operating standard matters because disputes often turn on chronology: when the payment was due, what notices were sent, what cure rights existed, and how the lender documented communications.

A servicing agent should build the case file before legal review

The strongest use of an agent in delinquency is building a complete case file before a human decision-maker acts. That is more valuable than auto-sending generic late notices.

A delinquency handoff packet should include:

- The payment history with aging and unapplied funds status.

- The governing note, guaranty, modification, and any side-letter provisions affecting remedies.

- The communication log, including reminders, borrower responses, and disputed items.

- The current collateral and covenant status, including missing insurance or reporting items.

- The recommended internal routing path: servicing, asset management, workout, or counsel.

This is where servicing automation earns its keep. It turns fragmented records into an auditable timeline that a portfolio manager, workout officer, or lawyer can use right away.

A practical decision framework for private CRE lenders

Private CRE lenders should choose loan servicing AI use cases based on repeatability, financial impact, and review burden. The real question is not whether a task is automatable in theory. It is whether the task has clear inputs, stable rules, and enough volume to justify controlled automation.

The framework below is more useful than a broad automation roadmap because servicing teams usually deal with mixed portfolios, uneven document quality, and limited engineering resources.

| Use case | Volume | Rule clarity | Risk if wrong | Best starting approach |

|---|---|---|---|---|

| Payment reminders | High | High | Low to moderate | Automate with ledger checks and suppression rules |

| Borrower request triage | High | Moderate | Moderate | Automate classification and draft responses only |

| Covenant follow-up | Moderate to high | Moderate | Moderate to high | Automate deadline tracking and completeness review |

| Reserve draw intake | Moderate | Moderate | High | Automate checklisting, keep approvals manual |

| Delinquency routing | Lower volume | Moderate | High | Automate case assembly and escalation triggers |

| Loan modification response | Low | Low | Very high | Do not automate beyond intake and routing |

The pattern is consistent: start where the workflow is repetitive and evidence-based, not where judgment changes loan economics or legal rights.

How to implement AI agents for loan servicing without losing control

Implementation goes well when lenders start with one narrow servicing workflow, map exact data sources, and define approval points before any automation goes live. Most failures come from dropping an agent on top of inconsistent servicing data and trying to patch controls later.

- Map one servicing workflow end to end, such as payment reminders or borrower request triage.

- Identify the authoritative system of record for balances, due dates, contacts, and loan status.

- Define trigger events, suppression rules, and exception categories in writing.

- Lock communication templates and require approval for any language that changes loan interpretation.

- Capture a full audit log showing source data, triggered rule, generated output, reviewer, and timestamp.

- Test historical files to measure false reminders, missed exceptions, and routing errors before launch.

- Launch with a limited loan cohort and compare cycle times, error rates, and manual touches against baseline.

- Expand only after servicing staff can explain how the agent behaved in both routine and exception cases.

According to the NIST AI Risk Management Framework Playbook, organizations should document intended use, human oversight, and performance monitoring for AI systems. In servicing, those controls are concrete: who can approve notices, when the agent has to stop and escalate, and how the lender checks that communications reflect current loan data.

Lenders also need a build-versus-buy view before scaling. For that question, see build vs buy ai agents for lending.

Common failure points in CRE servicing automation

Most servicing automation problems are not model failures. They are data-governance failures, workflow-design failures, or permission failures. Private lenders should assume these issues will show up unless they deal with them directly.

Stale or conflicting loan data

An agent that reads from spreadsheets, email attachments, and a servicing platform at the same time will eventually produce conflicting outputs. Balance-sensitive communications should pull from the ledger or another designated system of record, with overrides logged and time-stamped.

Too much automation at the edge cases

Loans in default, modifications in process, disputed escrows, and negotiated waivers should move to human review quickly. These cases create the highest legal and reputational risk, and they rarely benefit from autonomous communication.

Weak audit logs

If the lender cannot show which data field, document, or rule led to a notice, the workflow is not defensible. This matters even outside formal exam settings because borrower disputes usually come down to dates, amounts, and prior communications.

Poor template governance

Servicing agents should use approved language libraries with version control. Free-form generated text raises the odds that a routine reminder turns into an unintended statement about rights, fees, or loan status.

Frequently Asked Questions

What are AI agents for loan servicing in private CRE lending?

AI agents for loan servicing are workflow tools that monitor post-close servicing events and complete structured actions like drafting payment reminders, triaging borrower emails, tracking covenant deadlines, checking reserve draw packages, and preparing delinquency case files. In private CRE lending, they are most useful when connected to a servicing system of record and governed by approval rules and audit logs.

Which loan servicing tasks are safest to automate first?

The safest starting points are high-volume, rules-based tasks with low interpretive risk: payment reminders, borrower request classification, reporting deadline follow-up, insurance expiration notices, and reserve draw completeness checks. Tasks that change borrower rights or loan economics — such as waivers, modifications, and remedy decisions — should stay under human control.

How do AI agents for loan servicing differ from workflow automation?

Traditional workflow automation usually follows fixed if-then rules on structured fields. AI agents add document reading, inbox triage, request classification, draft generation, and multi-step routing across systems. That difference matters in servicing because many post-close tasks start with unstructured borrower emails, PDFs, and exception scenarios rather than a clean form submission.

Do location and loan type change how servicing AI should be deployed?

Yes. Servicing controls should reflect whether the loan is consumer or commercial, whether the state is judicial or non-judicial foreclosure, and whether notices or cure rights are governed by state-specific documents or statutes. A private CRE lender operating in Texas, California, and New York may use the same servicing agent framework, but late-stage default communications, reserve administration practices, and counsel handoff procedures usually need state-specific rules and templates.

What should a private lender require before using AI agents for delinquency workflows?

At minimum, the lender should require a designated system of record, approved notice templates, escalation thresholds, complete communication logging, and human review of any action related to default, remedies, or loan modification. The agent should assemble facts and route the file. It should not make unsupervised legal or credit decisions.