AI for Loan Servicing Payment Management Guide

Servicing teams spend too much post-close time chasing routine payment follow-up, answering borrower emails, and checking status updates. This article looks at where AI actually fits in CRE loan servicing workflows, with specific examples for reminders, failed-payment triage, payoff requests, and borrower service tickets.

Servicing teams burn a lot of time on payment operations because the work is repetitive, deadline-driven, and buried in emails, notes, and PDFs. In CRE lending, AI for loan servicing payment management works best in a few specific workflows: payment reminders, failed-payment triage, payoff requests, and borrower service tickets where speed matters but the record still has to hold up later.

Here’s what that looks like for private lenders and servicers in 2026, where AI actually cuts manual work, and where it should stop and hand the case to a person. It also connects these workflows to adjacent systems such as ai agents for loan servicing and the broader ai agents for private commercial real estate lending stack.

Key Takeaways

- AI fits high-volume, rules-based servicing work best: reminder scheduling, failed-payment categorization, payoff intake, and ticket routing.

- The best pattern is not full autonomy. It is draft generation, document collection, status tracking, and exception escalation with a complete audit trail.

- Payment workflows need system-of-record controls because the Consumer Financial Protection Bureau mortgage servicing rules under Regulation Z section 1026.36 and the Real Estate Settlement Procedures Act servicing rules under Regulation X can attach legal consequences to servicing communications and payoff timing in consumer contexts. Private CRE lenders often use the same control discipline even when the loan is business purpose.

- AI helps with payoff handling only if fee logic, approval thresholds, and source-document references are visible to staff. Hidden calculations create reconciliation risk fast.

- Borrower service tickets work better when AI keeps a channel-by-channel history, including prior emails, uploaded documents, payment events, and prior commitments made by staff.

What AI for loan servicing payment management actually does

AI for loan servicing payment management means software agents that monitor payment events, borrower messages, and servicing requests, then take limited actions such as drafting outreach, classifying exceptions, gathering documents, and updating queues. It does not replace the servicing system of record, cash application controls, or payoff approval authority.

The Federal Reserve guidance on supervisory considerations for financial institutions using AI pushes institutions toward governance, explainability, and risk management, not blind trust in model output. The National Institute of Standards and Technology AI Risk Management Framework makes the same basic point: higher-risk use cases need traceability, human oversight, and monitoring for drift. In servicing, that usually narrows the useful work to operational support with clear inputs and clear escalation rules.

A direct 40-to-60-word answer: AI for loan servicing payment management uses rules and language models to automate payment reminders, organize failed-payment follow-up, assemble payoff request data, and triage borrower service tickets while keeping a searchable audit trail of communications, documents, statuses, and human approvals.

Payment reminders: where AI reduces routine outbound work

Payment reminders are one of the cleanest servicing use cases because the trigger, audience, and timing are usually explicit. The real gain is not just sending messages faster. It is running a consistent cadence, documenting delivery, and cutting down on missed follow-up.

In a typical CRE servicing shop, reminder work includes pre-due notices, grace-period notices, failed-ACH follow-up, and internal alerts to asset management or servicing staff. AI can watch the servicing ledger or payment processor feed, then draft the right borrower message based on payment status, loan type, contact preference, and prior communication history.

| Scenario | Manual process | AI-assisted process | Human review needed |

|---|---|---|---|

| Upcoming due date | Staff exports due loans and emails borrowers individually | Agent generates queued reminder messages by rule and logs each draft | Usually no, if template and borrower list are preapproved |

| Grace period ending | Staff checks ledger and sends second-round reminders | Agent identifies unpaid accounts, applies approved language, and routes exceptions | Yes for disputed balances or prior promise-to-pay notes |

| Returned ACH | Servicer reviews processor notice and starts outreach | Agent classifies likely cause, requests updated payment method, and opens a ticket | Yes if fees, waivers, or legal notices are implicated |

A practical example: a borrower misses a monthly autopay because the operating account changed after a property-level refinancing. Instead of having a servicer read the processor notification, dig through prior emails, and draft a response from scratch, the agent can attach the failed-payment event, summarize the earlier borrower explanation, propose the next email, and create a follow-up task for two business days later if no response arrives.

For teams cleaning up post-close operations, this sits downstream from origination and underwriting workflows such as ai agents for cre loan origination and ai agents for cre underwriting, where borrower contact data, notice preferences, and loan terms should already be structured correctly.

Failed-payment triage: routing, classification, and next actions

Failed payments create a lot of operational noise because not every failure means the same thing. The value here comes from separating administrative issues from credit-relevant events before staff waste time in the wrong queue.

Most failed payments fall into a short list of categories: insufficient funds, closed account, expired authorization, processor error, timing mismatch, borrower dispute, or unapplied cash. An AI agent can classify the event from processor codes, ledger context, and borrower communications, then route it to the right workstream.

What good triage looks like

Good triage assigns each failed payment to a reason code, a deadline, a message template, and an escalation owner. That structure matters more than the model.

- Capture the payment failure event from the processor or servicing platform.

- Match the event to the loan record, borrower contacts, and open tickets.

- Classify the likely cause using return codes, prior notes, and recent borrower messages.

- Draft the next borrower communication with the relevant payment amount, due date, and response options.

- Escalate exceptions involving disputed balances, legal notices, or repeated failures to a human reviewer.

- Log every draft, edit, send event, and status change in the servicing record.

This is also where communication continuity matters. If the borrower previously submitted insurance documents through a servicing inbox, or discussed account changes during intake, that context should be available. Related systems such as ai agents for borrower intake and ai agents for cre document analysis help upstream data arrive in usable form instead of as disconnected PDFs and inbox threads.

Payoff requests: document gathering, fee checks, and audit trails

Payoff requests look simple until you have to produce one accurately. The hard part is not generating a number. It is pulling the right inputs, applying fee logic correctly, and keeping a record of how the statement was built.

The Consumer Financial Protection Bureau payoff statement requirements under Regulation Z section 1026.36(c)(3) generally require creditors or servicers in covered contexts to provide an accurate payoff statement within a reasonable time, no more than seven business days after a written request, subject to limited exceptions. Many private CRE shops use that timing benchmark operationally even when a loan falls outside consumer mortgage scope because borrowers and title counterparties still expect a prompt response.

An AI agent can cut manual work in payoff processing by pulling the note rate, default interest rules, extension fees, exit fees, protective advances, late charges, suspense balances, and approved good-through date assumptions into one review workspace. It can also flag missing source inputs, such as an unreconciled protective advance or an unposted wire.

Where payoff automation fails

Payoff automation breaks down when fee rules are implicit, modifications are not digitized, or side-letter economics live in email instead of the servicing file. In those cases, the agent can produce a clean-looking draft from incomplete inputs, which is exactly the kind of error that slips through if nobody slows down.

That is why payoff workflows need explicit source references and approval gates. A reviewer should be able to see which agreement section supports each fee line, whether default interest was switched on manually, and whether the good-through date assumptions match the request. For lenders building this into a larger servicing stack, the control logic should line up with ai agents for cre lending compliance.

Graphline focuses on auditable payoff statements for this reason: speed matters, but auditability matters more when a borrower, title company, or investor questions the number later.

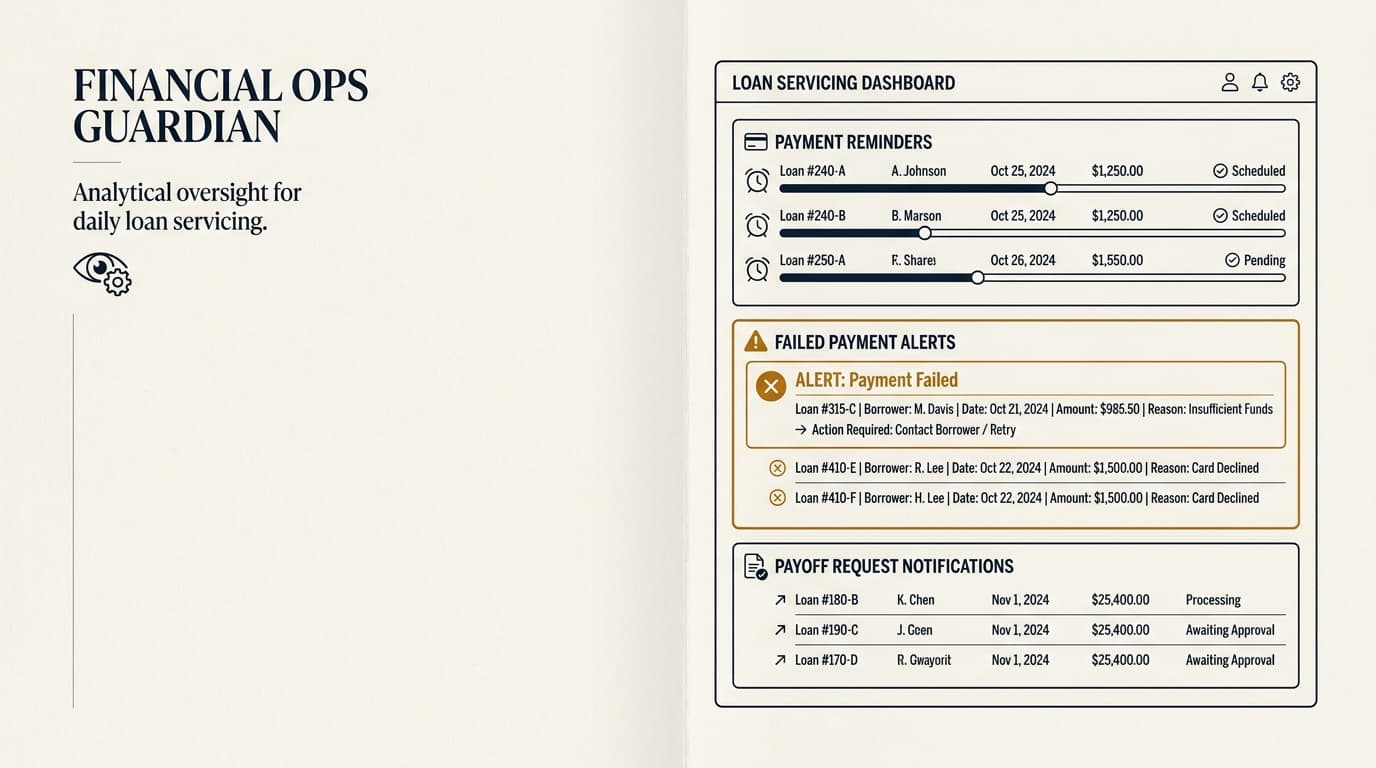

Borrower service tickets: preserving history across channels

Borrower service tickets usually end up scattered across shared inboxes, servicing notes, phone logs, and document portals. AI is useful here because it can build a unified case record without forcing staff to retype the same history into multiple systems.

A servicing ticket might start as an email about a late fee waiver, continue with an uploaded bank letter, and end with a payoff request from a title agent. An agent can stitch those events into one case timeline, summarize the status, and identify the next required action. That cuts duplicate outreach and reduces the chance that one staff member contradicts another.

The National Institute of Standards and Technology Privacy Framework recommends mapping data flows and applying role-based access controls when sensitive data is involved. In practice, that means the servicing agent should show communication history and relevant documents, but it should not expose unrelated borrower files to every queue user.

Ticket history also helps portfolio oversight. Repeated payment issues, fee disputes, or extension inquiries can feed into ai agents for portfolio monitoring so asset management sees patterns before the next reporting cycle.

A practical workflow for deploying AI in servicing payment management

The strongest implementation pattern is narrow deployment around one payment workflow at a time. Teams that start with one queue, one approval policy, and one measurement set usually get cleaner results than teams that try to roll out AI across servicing all at once.

- Select one servicing workflow with high volume and stable rules, such as failed ACH follow-up.

- Map the authoritative data sources, including the servicing system, payment processor, inboxes, and document repository.

- Define the actions the agent may take automatically and the conditions that require human approval.

- Standardize templates for reminders, exceptions, and payoff acknowledgments before model deployment.

- Test the workflow on historical servicing cases and compare draft accuracy, routing accuracy, and handling time.

- Launch with full logging of prompts, source records, edits, approvals, and outbound communications.

- Review exception rates monthly and retrain rules when payment codes, fee policies, or borrower behavior changes.

Teams that need upstream data hygiene often find that the real bottleneck is not messaging at all, but document quality. In those cases, supporting workflows like ai document extraction for rent rolls or cre loan origination workflow ai agent may need attention first so servicing inherits cleaner records.

Decision framework: what to automate, what to review manually

The right automation boundary depends on financial risk, legal sensitivity, and data quality. A simple rule works well here: automate repeatable communications and information gathering; keep balance-affecting decisions and nonstandard borrower commitments in human hands.

| Workflow task | Automate | Human review | Why |

|---|---|---|---|

| Pre-due reminder drafts | Yes | Rarely | Rule-based, low discretion, easy to template |

| Returned payment outreach | Yes, with exception routing | Yes for repeated failures or disputes | Classification is useful, but concessions affect account treatment |

| Late fee waiver response | Draft only | Always | Waivers change economics and may set precedent |

| Payoff statement assembly | Yes, as draft workspace | Always before release | Small input errors can create settlement issues |

| Ticket summarization | Yes | Spot check | High time savings, lower economic risk |

This is where lenders often overreach. They try to automate judgment-heavy servicing actions before cleaning up the low-risk queues. The better sequence is reminders, payment triage, ticket summarization, and then payoff assembly with strict approval controls. For firms comparing broader architecture choices, the pillar page on ai agents for private commercial real estate lending covers workflow and ROI across the full lending lifecycle.

Controls, auditability, and borrower communication standards

Payment management automation is only as reliable as its controls. The minimum standard is a complete record of what source data the agent used, what draft it created, what a human changed, and what was ultimately sent or issued.

The Federal Deposit Insurance Corporation guidance on managing risks associated with third-party relationships makes the point plainly: institutions still own the risk even when vendors provide the technology. The Office of the Comptroller of the Currency model risk management handbook materials say governance should cover validation, performance monitoring, and change management. For private CRE lenders, the practical version is straightforward:

- Keep the servicing platform or loan system as the system of record for balances and statuses.

- Require approval for any borrower-facing message that changes fees, payoff amounts, or legal position.

- Store model outputs with timestamps, user edits, and source citations.

- Segment permissions so payoff preparation, borrower messaging, and policy changes are not all controlled by the same user role.

- Review a sample of closed tickets and released payoff statements for completeness and accuracy.

Those controls also make downstream review easier for finance, compliance, and investors. If the same institution is using ai underwriting for private lenders or other AI-assisted workflows, a shared audit framework cuts operational friction.

Frequently Asked Questions

What is the best first use case for ai for loan servicing payment management?

The best first use case is usually payment reminders or failed-ACH follow-up because the triggers are clear, message templates are easier to standardize, and financial risk is lower than in payoff or fee-waiver decisions. Teams can measure cycle time, response rate, and exception rate before expanding scope.

Can AI send payoff statements automatically?

It can assemble a payoff draft automatically, but automatic release is usually a bad control choice. Payoff statements depend on accrued interest, fees, advances, and modification terms that may not be fully structured. A human reviewer should confirm the good-through date, fee basis, and source documents before issuance.

How does AI preserve borrower communication history in servicing?

It links emails, portal submissions, payment processor events, internal notes, and generated drafts into one case record. The practical advantage is simple: staff can see prior promises, disputes, uploaded documents, and earlier outreach without searching multiple systems or rebuilding the timeline by hand.

Does this workflow differ by lender type or state?

Yes. Business-purpose CRE servicing is generally less prescriptive than consumer mortgage servicing, but policies still vary by lender, servicing platform, and state-level notice practices. Multi-state lenders often adopt one higher-control workflow for reminders, payoff handling, and record retention so staff are not juggling separate operating standards by jurisdiction.

What should a private CRE lender measure after deployment?

Measure handling time per ticket, reminder send coverage, failed-payment routing accuracy, payoff turnaround time, exception rate, and the share of borrower-facing drafts that require material edits. Those numbers tell you whether the agent is actually reducing manual work or just moving it into a review queue.