AI Document Extraction for Rent Rolls: QC Guide

Rent roll extraction usually breaks at the field level: unit IDs change format, lease dates get misread, concessions end up counted as base rent, and vacant units are labeled inconsistently. This article lays out how AI rent roll extraction needs to handle mapping, anomaly detection, and quality checks before lenders use the output to size or price a deal.

Rent rolls usually do not break because the PDF was unreadable. They break because the data looks clean after extraction while the fields that matter to underwriting are mapped wrong. AI document extraction for rent rolls only helps if it turns inconsistent borrower schedules into tenant-level data you can trace back to the source and defend in underwriting, exception review, and credit committee.

This article covers the failure points lenders run into most: bad field mapping, tenant-level anomalies, and QC checks that should happen before anyone sizes or prices a loan. It also lays out where automation works, where an analyst still needs to step in, and how this fits into broader ai agents for private commercial real estate lending programs.

Key Takeaways

- Rent roll extraction usually fails when one source field can mean several different things. "Rent" might mean base rent, gross rent, net effective rent, or current charges.

- Tenant-level issues like duplicate unit IDs, expired leases marked occupied, and month-to-month tenants with hard term dates still cause underwriting mistakes even when OCR looks accurate.

- Quality control should test field logic, not just text recognition. An occupied unit should line up with lease dates, rent, and square footage.

- Reliable extraction needs a standard output schema, clear exception thresholds, and an audit trail that ties every mapped field back to the source line item.

- Lenders should treat rent roll extraction as an input-control problem tied to origination and underwriting handoffs, not as a standalone OCR task.

AI document extraction for rent rolls: what lenders actually need

For lending, rent roll extraction is not just text capture. It is the conversion of borrower-supplied schedules into a normalized tenant ledger. Every row needs to trace back to the source, and every field needs to land in a defined underwriting schema.

In practice, lenders usually need the same core fields regardless of property type: unit or suite ID, tenant name, unit type, leased square footage, lease start date, lease expiration date, current monthly rent, market rent if provided, security deposit, concessions, delinquency indicators, and occupancy status. According to the Federal Deposit Insurance Corporation real estate lending examination guidance, lenders are expected to maintain sound collateral analysis and documentation controls. For income-producing property, that only works if the income data is complete, internally consistent, and supportable.

The problem is simple: borrower rent rolls are not standardized. Multifamily schedules may group by floorplan instead of unit. Office schedules may list rentable square feet and usable square feet in separate columns. Retail schedules may fold reimbursement charges into the same cell as base rent. According to Mortgage Bankers Association commercial real estate finance research, underwriting decisions in CRE lending depend heavily on property cash flow documentation. If the input table is wrong, DSCR, occupancy, rollover, and concentration analysis will be wrong too.

That is why rent roll extraction usually sits upstream of ai agents for cre loan origination and ai agents for cre underwriting workflows instead of replacing them.

Common rent roll field mapping issues

The most common extraction errors are semantic, not optical. The model reads the cell correctly, then sends it to the wrong underwriting field.

Rent fields: base rent vs. gross rent vs. charges

Many rent rolls have several rent-like columns that look interchangeable but are not. A lender sizing to in-place income needs to know whether a number is contractual base rent, billed rent with reimbursements, or net effective rent after concessions.

A common office example looks like this:

| Source label | Possible meaning | Underwriting risk if mapped incorrectly |

|---|---|---|

| Current Rent | Monthly base rent | Low if confirmed by lease terms |

| Total Charges | Base rent plus CAM, taxes, insurance, utilities | Income overstated if treated as contractual rent |

| Effective Rent | Net of abatements or free rent | Income understated or timing distorted |

| Scheduled Rent | Budgeted or market rent | In-place income confused with pro forma |

According to the Federal Reserve supervisory guidance on commercial real estate concentrations, lenders need to distinguish stabilized assumptions from current cash flow support. A mapping system that collapses all rent-like columns into one field adds noise that underwriting does not need.

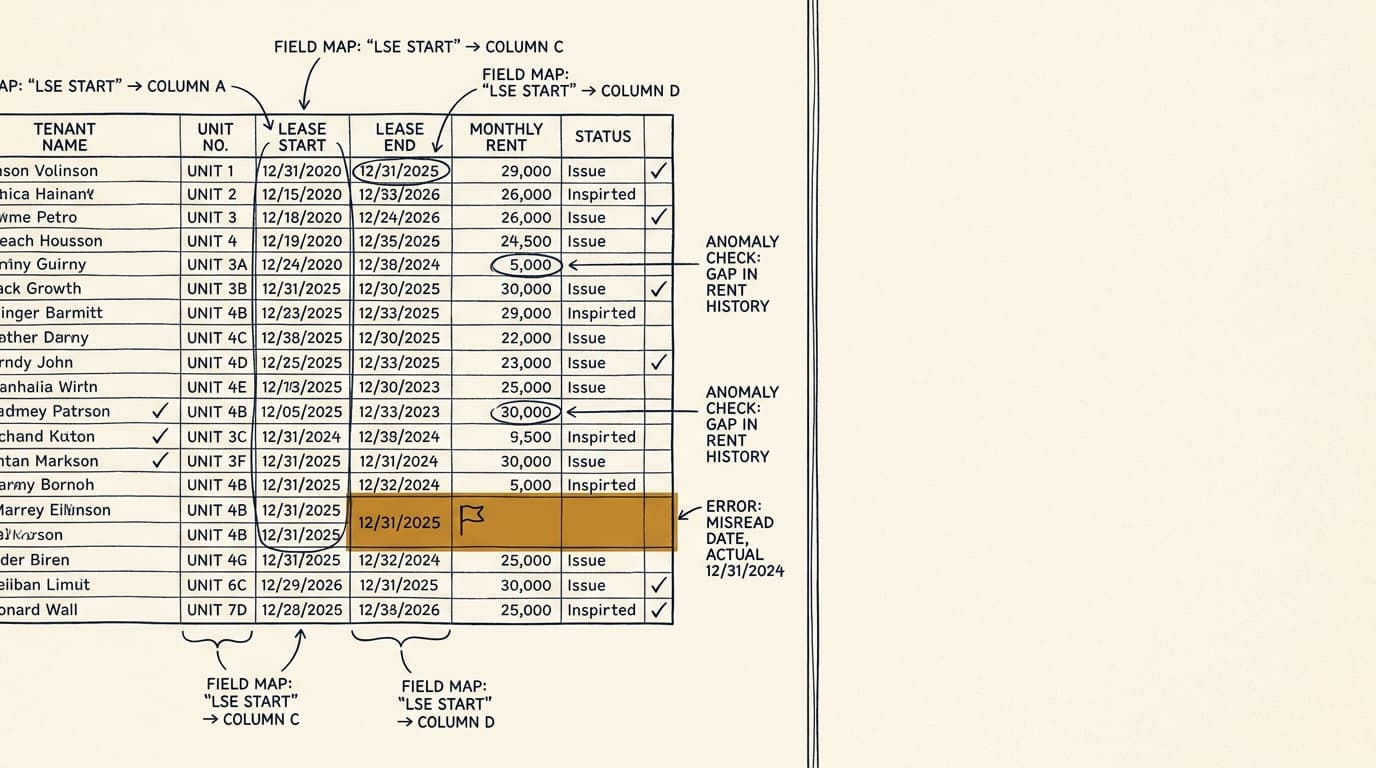

Lease dates and term fields

Lease start and expiration dates are often split across term columns, note fields, or renewal options. Extraction systems also tend to stumble on date formats like 3/1/26, 03-01-2026, or "MTM" used instead of an end date.

Typical mapping failures include:

- Renewal option dates captured as actual expiration dates

- Month-to-month tenancies converted to blank dates with no occupancy flag

- Two-digit years interpreted in the wrong century

- Move-in dates mapped as lease commencement dates

These are not small errors. Rollover analysis depends on date precision. If a tenant expiring in 2026 is read as expiring in 2028, refinance proceeds and reserve assumptions can move in a material way.

Unit identifiers and square footage

Unit identifiers look straightforward until you see how they actually show up in source files. "101," "Unit 101," "Suite 101," and "101A" may be different spaces, or they may be the same space written four different ways across tabs.

Square footage creates a second problem. According to Building Owners and Managers Association International measurement standards resources, commercial space measurements can vary depending on the standard used and whether the figure is rentable or usable. If the rent roll does not say which one it shows, extracted PSF calculations can point in the wrong direction even when the cell value itself is correct.

Tenant-level anomalies that distort underwriting

Tenant-level anomalies are often the difference between a clean import and a dataset you can trust. Most only show up after extraction, when you run row-level logic checks.

Occupied vs. vacant status conflicts

A unit marked vacant should not also have an active tenant name, current rent, and a future expiration date without some explanation. A unit marked occupied with zero rent may be legitimate, but it should trigger review for free-rent periods, model units, employee units, or bad debt masking.

Examples worth flagging:

- Vacant units with security deposits

- Occupied units with no lease start date

- Former tenants retained on the report with zero balance but active status

- Notice units coded as occupied without separate near-term rollover tags

Duplicate tenants and duplicate units

Duplicate rows often show up when borrowers export both summary and detail tabs into the same PDF. The extraction engine may capture both, and suddenly income is double-counted.

A practical rule is to flag any repeated combination of unit ID, tenant name, and rent amount, then review exceptions where one row reflects a current tenant and the other reflects a renewal or amendment. In multifamily, duplicate unit counts can move occupancy by several percentage points on smaller assets.

Concessions, delinquency, and non-standard notes

Concessions and delinquency indicators often live in comments instead of clean columns. Phrases like "2 months free," "legal," "skip paid by agency," "payment plan," or "employee discount" may not hurt OCR quality, but they absolutely change the income story.

This is where narrow extraction logic often beats generic OCR. A lender does not just need the note text captured. It needs the note classified so analysts can separate contractual rent from collectible cash flow. That distinction matters even more when the extracted rent roll feeds ai underwriting for private lenders models or exception queues.

Quality-control checks before sizing or pricing a loan

Good quality control asks whether the extracted dataset behaves like a real rent roll. A high field-level confidence score does not answer that question.

The following checks are the minimum lenders should run before relying on extracted data:

- Define a standard schema for required and optional fields by property type.

- Map each extracted field to a source citation showing the original page, row, and cell context.

- Reconcile unit counts, occupied counts, and vacancy counts against the source summary if one is provided.

- Test date logic so lease start dates come before expiration dates and month-to-month records are coded explicitly.

- Separate base rent from reimbursements, fees, concessions, and one-time charges.

- Flag duplicate unit IDs, duplicate tenant names, and duplicate rent rows for review.

- Run range checks on rent per unit and rent per square foot to catch outliers.

- Escalate records with conflicting occupancy, missing lease terms, or note-based concessions to analyst review.

According to the National Institute of Standards and Technology AI Risk Management Framework, trustworthy AI use requires documented validation, monitoring, and human governance over high-impact decisions. In lending, that means the extracted rent roll should show the final field values, but also what was uncertain, what was normalized, and what was escalated.

A practical threshold is to auto-accept only rows that pass every structural check and send the rest to targeted review. That is usually far more efficient than asking analysts to reread an entire 200-line schedule.

A practical review workflow for rent roll extraction

Rent roll extraction works best as a staged review process with exception handling, not a one-shot import. The goal is to cut manual review without losing the audit trail.

A workable lender workflow looks like this:

- Ingest the borrower rent roll in its original form, including scanned PDFs and spreadsheet exports.

- Classify the property type and detect the document layout before mapping fields.

- Extract tenant-level rows into a normalized schema with source-linked citations.

- Apply rule-based checks for dates, occupancy, duplicates, and rent-field conflicts.

- Route exceptions to an analyst queue with the exact source snippet that triggered the flag.

- Approve, correct, or reject flagged records before exporting the final dataset to underwriting.

- Store the final structured output and exception log for audit and later servicing use.

This matters because the same rent roll data usually moves across several teams. A disciplined extraction layer cuts re-keying at intake, supports the cre loan origination workflow ai agent handoff, and leaves a cleaner record for post-close monitoring by ai agents for loan servicing and ai agents for portfolio monitoring.

Where AI rent roll extraction adds value — and where analysts still need to review

AI is good at repetitive normalization across inconsistent layouts. It is much less reliable when the source itself is ambiguous, internally inconsistent, or economically material enough to require judgment.

| Task | AI extraction fit | Why |

|---|---|---|

| Capturing unit, tenant, and date fields from varied layouts | High | Pattern recognition and row reconstruction are repeatable |

| Separating base rent from reimbursements when labels are clear | High | Column semantics can be learned and validated |

| Interpreting handwritten notes or vague comments | Moderate | Text may be readable but economically ambiguous |

| Determining whether collectible income should exclude concessions or delinquent tenants | Moderate to low | Requires policy judgment and underwriting context |

| Approving exceptions that change loan proceeds or pricing | Low | Needs analyst accountability and documented review |

The practical point is that lenders should not ask extraction tools to make credit decisions. They should ask them to produce a structured, reviewable dataset that gets analysts out of clerical work. In a broader workflow, this usually sits inside an ai agents for cre document analysis stack with separate controls for policy, privacy, and audit under ai agents for cre lending compliance.

Frequently Asked Questions

What is AI document extraction for rent rolls?

AI document extraction for rent rolls converts borrower-provided rent roll files into structured tenant-level data such as unit IDs, lease dates, rent amounts, occupancy status, and square footage. For lending, the output should include field-level traceability back to the source document and exception flags for ambiguous or conflicting records.

How accurate is AI rent roll extraction in commercial real estate lending?

Accuracy depends less on OCR alone and more on document variety, source quality, and post-extraction validation. Clean spreadsheet exports are usually easier than scanned PDFs with summary tables, handwritten notes, or mixed rent definitions. In practice, lenders should measure row-level and field-level validation pass rates, not just character recognition scores.

Which rent roll fields cause the most extraction errors?

The fields that cause the most trouble are current rent, effective rent, reimbursements, lease expiration dates, occupancy status, unit identifiers, and comments related to concessions or delinquency. These fields often carry ambiguous labels or note-based exceptions that need rule checks and analyst review.

Does rent roll extraction vary by market or property type?

Yes. Multifamily rent rolls usually emphasize unit status, deposits, and monthly charges, while office and retail rent rolls are more likely to include suite numbers, rentable square footage, reimbursement structures, and option periods. Market practice also varies by property management system and region, so lenders in dense urban office markets often see more reimbursement complexity than lenders focused on suburban multifamily assets.

What quality checks should a lender require before using extracted rent roll data?

At minimum, the lender should require source-linked auditability, duplicate detection, occupancy reconciliation, lease date logic checks, separation of base rent from non-rent charges, and exception review for concessions, delinquency notes, and missing fields. If the data will affect proceeds or pricing, flagged records should be reviewed before the dataset enters underwriting.